My views are that it has been a long and frustrating journey but we are close to the bottom of the credit cycle for bandhan. I sipped the stock for a year post the promoter disinvestment, the share price is realy beaten down do i dont see a point in selling now.

My initial thesis of investing for the long term has changed after i saw how aggressive the large private banks are getting rural finance, how i feel the best customers of bandhan will eventually move to hdfc and axis. This coupled with the fact that the management has gided for lower growth of 20% in the last Q2 con call has dampened my bullishness.

The rising interest rates also are compressing NIMs since the lending is mainly fixed rate and the RBI reversal of the PSL income is a big damper, they lose fee income and have to create RDIF deposits by raising expensive bulk deposits

But with the actions that the managent has taken over the last week with the arc sale and the CGFMU happening before the next quater makes me thing we are closer to the end of the credit cycle for bandhan. The NIMs should normalize by next year once the hikes taken by the bank flow through.

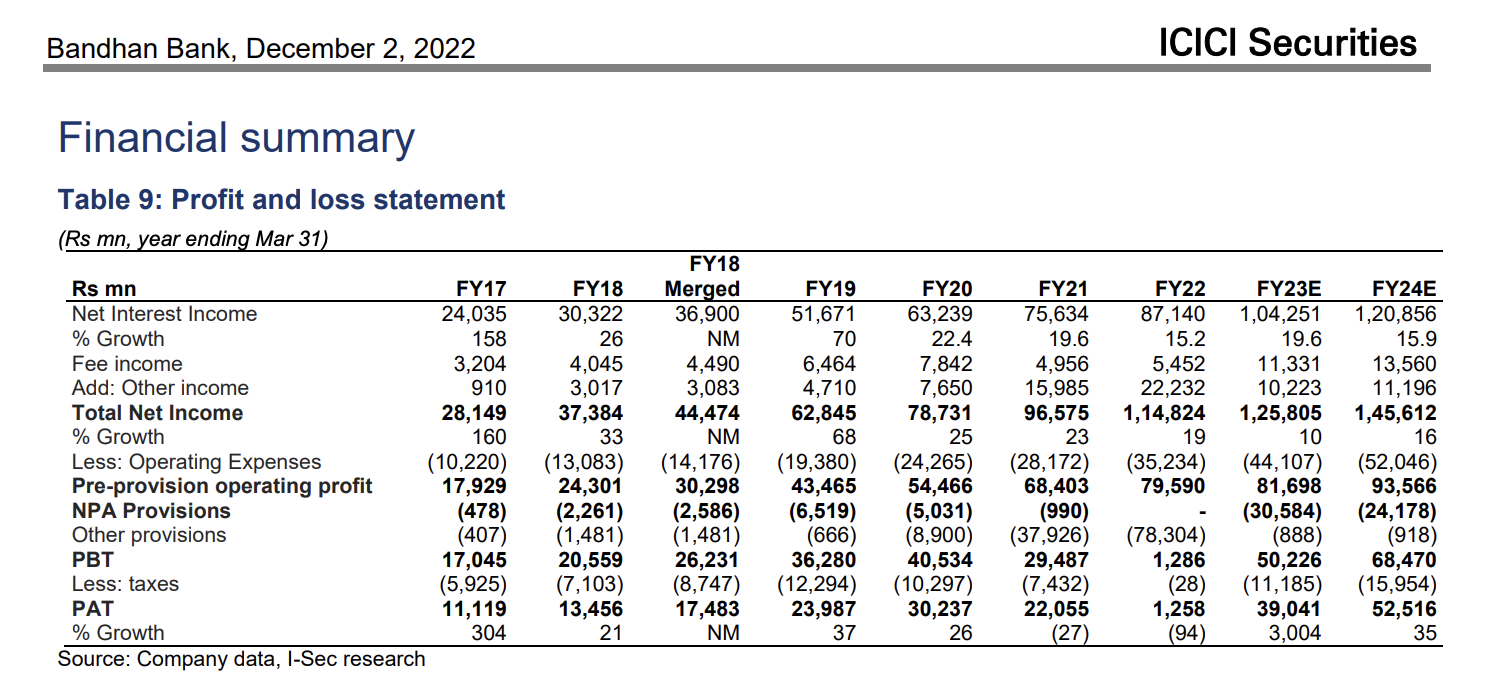

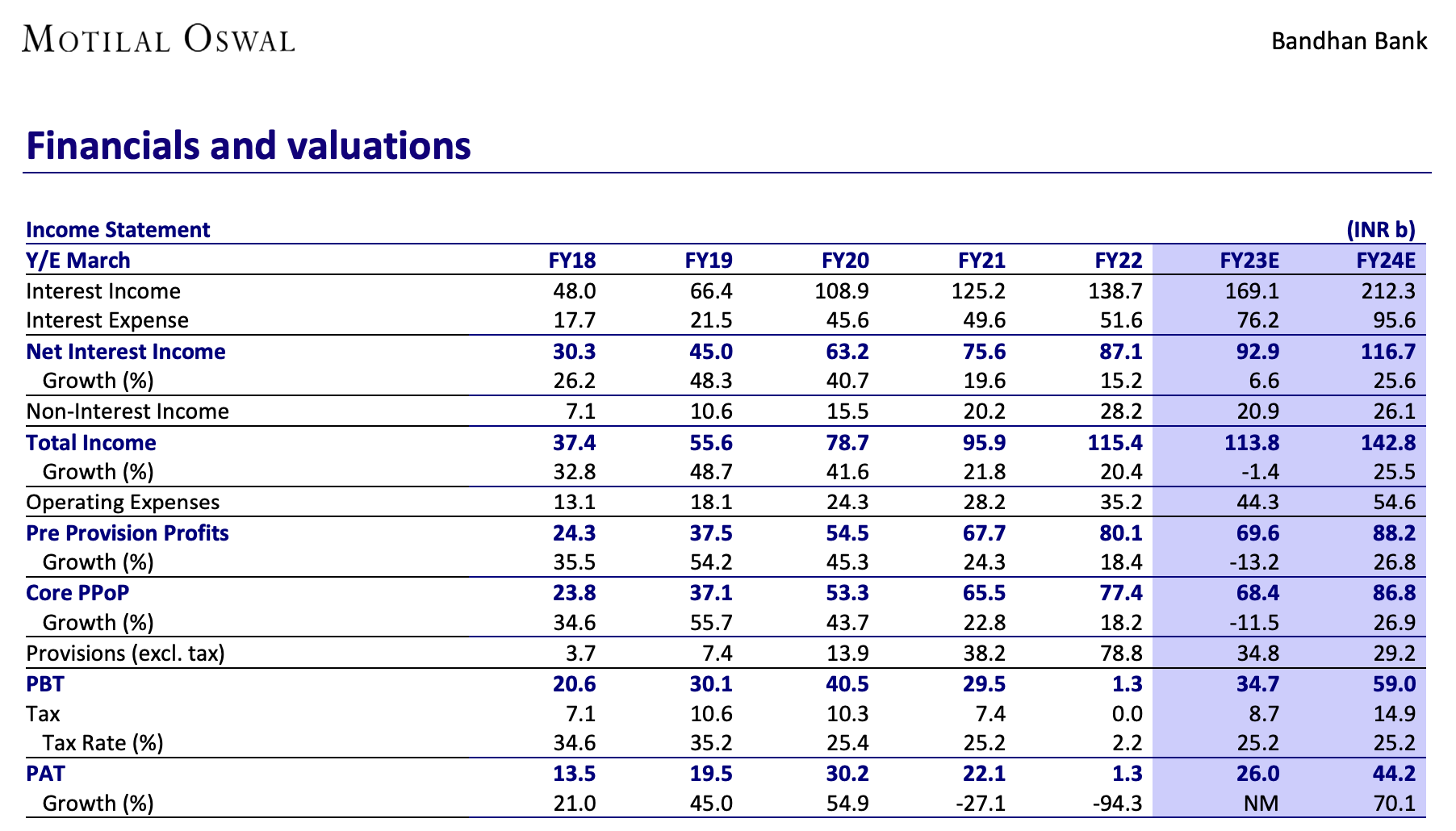

If there is no forth wave of covid or anything that can cause a major macro shock we should see a very strong earnings next year, my estimate is ~40k cr (Motilal and icici sec have estimates 44-52k cr) so still holding on atleast for a year and then evaluate things from there

| Subscribe To Our Free Newsletter |