I am also personally very interested in low volatility portfolios. So ran a backtest based on following method.

- Measure the volatility of prev year.

- Measure DD from high within last three years.

- Calculate z scores of both the criteria.

- Calculate total z-score, by 75% weightage to Low volatility and 25% to minimum drawdown from three year high.

- Rank the stocks with least scores. Filter the stocks which trades at least 99% of total trading days.

- Shortlist top 20 stocks. Form equal weight portfolio.

- Rebalance monthly.

Other parameters

- Direct Taxes:- 10% of yearly profit

- Brokerage/transaction costs:- 0.275%

- Cash Component:- 5% of total portfolio.

- Initial Capital:- 11 lacs

- Dividends:- not considered

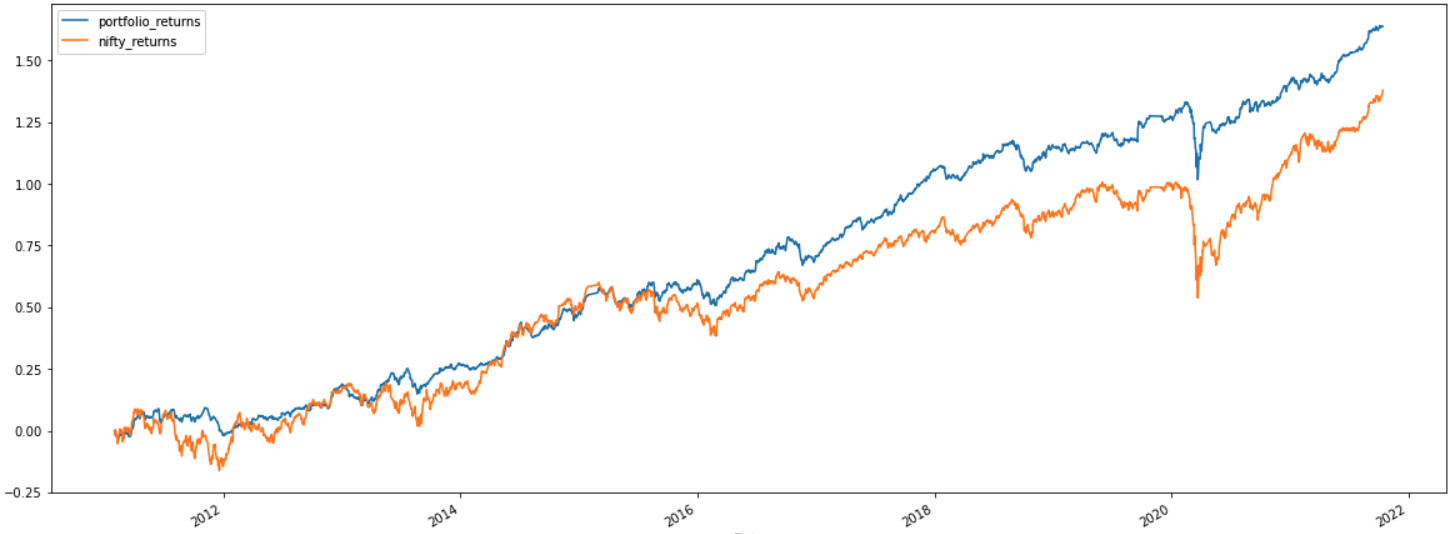

Equity Curve

Backtest Period:- Jan 2011 to Oct 2021

Benchmark:- Nifty 50

CAGR:- 12.75%

Annual Volatility:- 11.01%

Beta:- 0.47

Sharpe Ratio:- 1.37

Omega Ratio:- 1.29

Sortino Ratio:- 1.92

Max Drawdown:- 27.98%

Disclaimer:-

This is not an investment advice. The above data has represented for study purpose only. I am not SEBI approved investment advisor.

The above data is prone to calculation mistakes, inaccurate data etc.

| Subscribe To Our Free Newsletter |