@Ashusharma On TTM basis PE looks high low growth in FY22. If we look at H1FY22 it has already reported net profit of 28Cr and likely that it will report 60Cr for full year, PE for FY23 will be 30-35 at current range of market cap.

If we look at the Oct and Nov month data of passenger movement across airports in India (Dec month data is yet to come) Q3 must be stronger quarter for DFS.

Seasonally also H2 revenue is higher than H1( source: Q2 concall)

Even if we consider minor impact on revenue which may happen due to temporary closure of two louges run by premium plaza( at Delhi and Hyderabad) ,H2 numbers must be better.

Total revenue for the H1 is 332Cr , crossing revenue of 367Cr for FY20 is not a challenge.

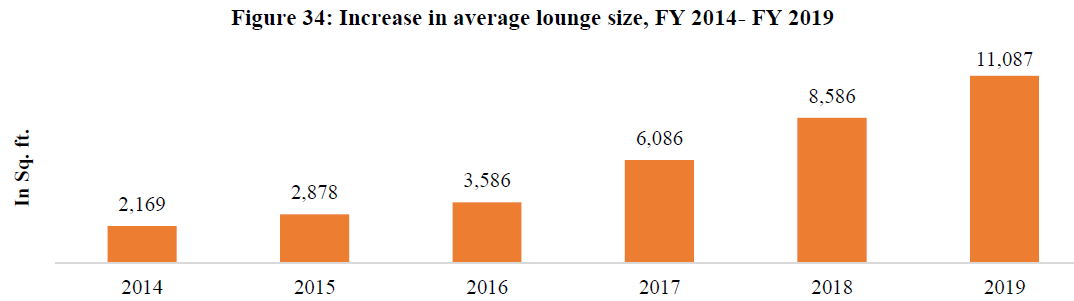

Key question to what extent it will grow in FY24 on high base of FY23 depending new airports/terminals. You must have noticed the existing lounges are running full and generally there is waiting period of around 10min to enter inside in airport like Bengaluru. Not much growth may be possible in existing lounges. Even though existing lounge size can be expanded to accommodate more people it will take time. Below image shows how average lounge size has increased from 2015 to 2019.

Agree that it does not have much pricing pressure and operating margins will remain around 12% as indicated by management.

| Subscribe To Our Free Newsletter |