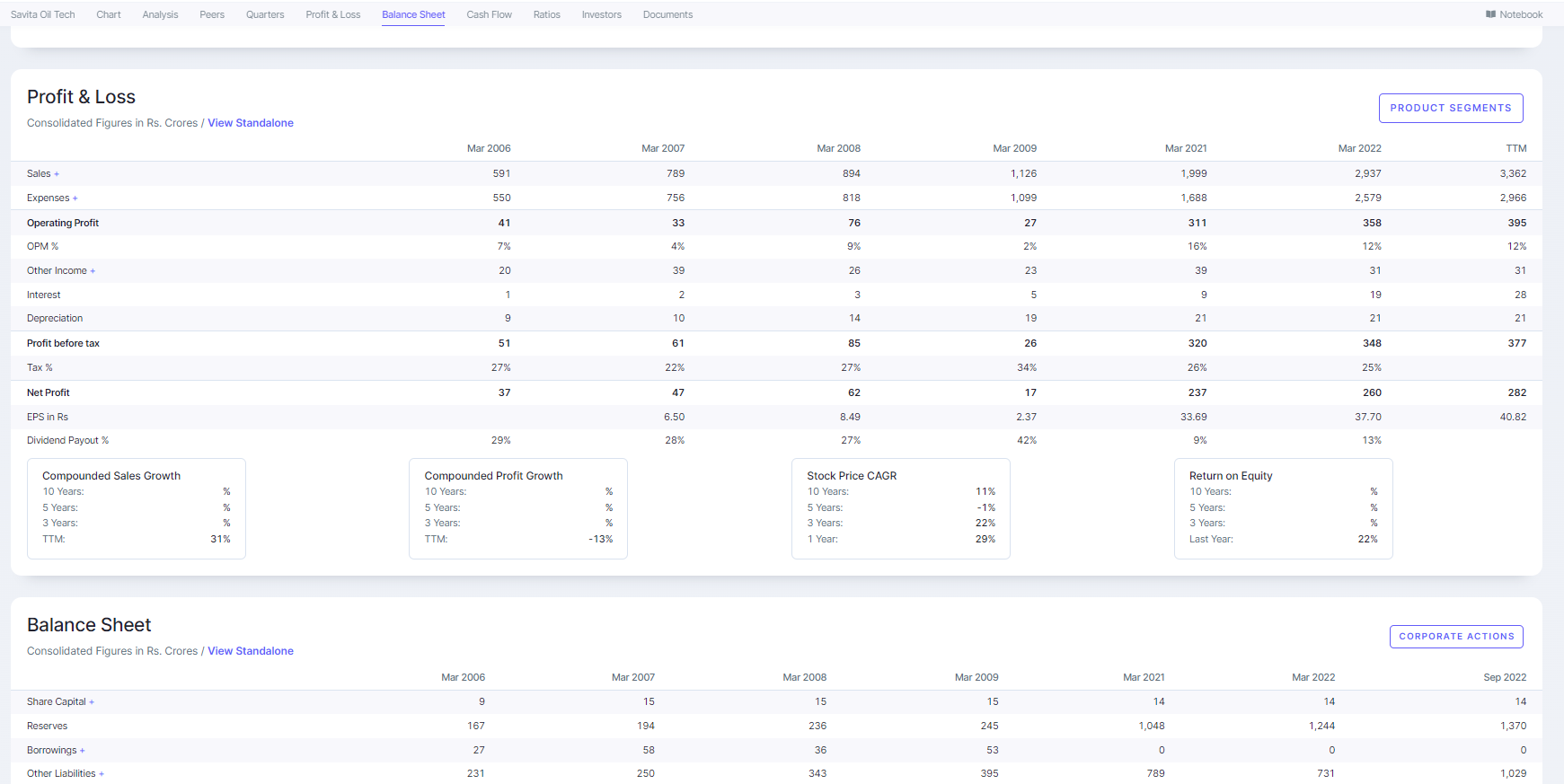

Hi All, I came across Savita Oil while scanning through power sector stocks. Contrary to my initial expectations, Savita seems to be a consumable business with revenues almost equally split between Power (transformer oils & cable filling compounds), FMCG & Pharma (paraffins, specialty waxes), Automobiles & Industrials (lubricants).

While scanning through its financials and presentations, a few doubts arose. The company doesn’t do concalls and brokerage coverage is limited, so would appreciate if any member is able to clarify these doubts:

- Company has zero debt on its balance sheet, yet paid 19Cr in interest costs in FY22 (Interest on customer advances could be an explanation, but that was only 14Cr in FY22 and interest on it would hardly be more than 1-2Cr). Interest expense continues to increase, its 18Cr already in H1 FY23. Borrowings continue to remain 0 on balance sheet. No explanation in FY22 AR notes. Can anybody help explain this?

-

Why does the company have 450Cr+ cash parked in equities (stocks, MFs) and debt funds instead of FDs? Isn’t this a very risky way of treating cash on the balance sheet, especially when both bond and equity markets are so volatile?

-

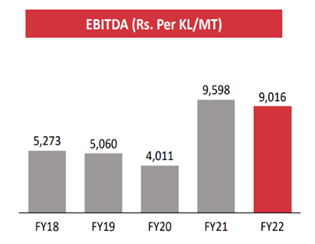

The EBITDA per KL for Savita seems to have more than doubled in FY21 and FY22 from the levels of the previous 3 years in tandem with crude oil price rise. Does anybody understand how pricing works for Savita? Are they able to retain gross margin in % terms when prices increase? That would explain the > 2x rise in EBITDA per KL.

- Related party transactions – I did not understand two huge transactions worth 115Cr involving KMP and their relatives. The transactions are tagged as purchase of shares (screenshot from AR below). What are these share purchases for which company seems to have paid out a huge sum of money to KMP?

- Any corporate governance red flags apart from points 2 & 4 highlighted above? I did a quick check on the following:

- Promoter ownership & pledge – OK

- EBITDA to CFO conversion – OK. Over 5Y, 75% EBITDA converted to CFO

- Contingent liabilities – OK (Negligible – 5% of net worth)

- KMP remuneration as % of PAT – OK (4.2% in FY22 and 3.6% in FY21)

| Subscribe To Our Free Newsletter |