I’ve spent most of the week reading old concalls of VBL and updating my thesis. This post is my understanding of the business as a whole, the nuts and bolts of it (especially the “Unstructured notes” section). What follows is a copy/paste from my Notion page so may have certain unfinished bits/errors etc. Wasn’t sure if I should share or not since its perhaps a bit too long.

Varun Beverages (VBL) is a bottler for PepsiCo in India and abroad. The relationship with PepsiCo is now 30+ years old and as a company, VBL has been in the bottling business with PepsiCo for 30+ years and in the beverage industry for 55+ years. The company went public in late 2016.

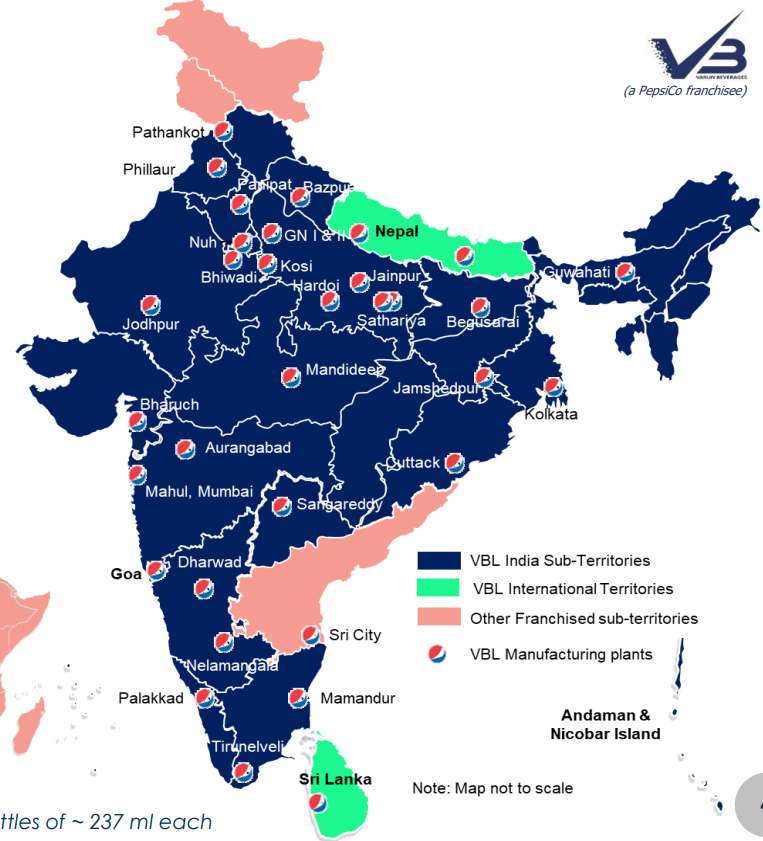

Geography

During the last 6 years post listing, the company has continued to maintain its stellar growth pre-listing, unlike most businesses that listed in ‘16/’17 period (Parag Milk, Thyrocare etc.). VBL had distribution rights in 17 states and 2 Union Territories and 5 countries in 2016 when it got listed, whereas today, it has presence in 27 states and 7 UTs and 6 countries.

Most of East, West and South India rights were taken from PepsiCo in the last few years. PepsiCo and Coke have a combined market share of ~90% in India in CSD+Juices. PepsiCo has ~38% in that.

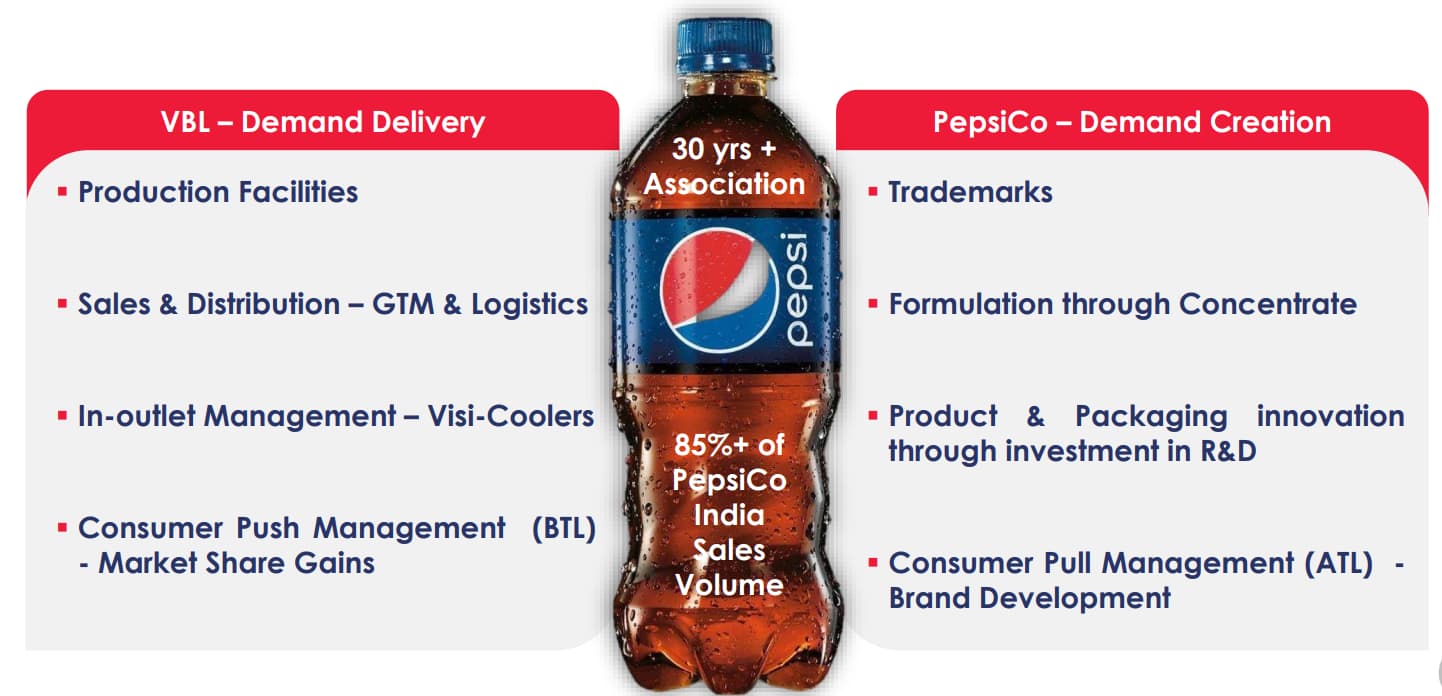

PepsiCo Partnership

As partners, VBL and PepsiCo handle different responsibilities in the symbiotic relationship. PepsiCo owns the Branding, Trademarks, Formulation and supply of concentrate, Product & Packaging innovation and Customer Pull Management (ATL) via Brand development. VBL handles the production, distribution, logistics, outlet management and Customer Push Management (BTL)

Products

The company sells products under broad categories of carbonated soft drinks (CSD), Juices and Packaged Water. They sell energy drinks under Sting brand. sports drinks under Gatorade and dairy products under Creambell which is owned by the promoter and not PepsiCo.

Volume Growth

20% CAGR over last 10 years. (Company has grown at 20% CAGR over 25 years) Interesting how international volumes have kept up with the domestic volume driven by territory acquisitions.

In million cases

| Year | Domestic Volume | International | Total | International % |

|---|---|---|---|---|

| 2012 | 114 | 22 | 136 | 19% |

| 2013 | 132 | 21 | 153 | 16% |

| 2014 | 144 | 26 | 170 | 18% |

| 2015 | 209 | 31 | 240 | 15% |

| 2016 | 224 | 52 | 276 | 23% |

| 2017 | 224 | 55 | 279 | 25% |

| 2018 | 274 | 66 | 340 | 24% |

| 2019 | 404 | 89 | 493 | 22% |

| 2020 | 337 | 88 | 425 | 26% |

| 2021 | 454 | 115 | 569 | 25% |

| 2022 |

Key Milestones

-

2016

- Got listed

- Launched Pepsi Black

- 45% of PepsiCo’s volumes. Presence in 17 states and 2 UTs

-

2017

- Acquired Odisha, MP, Chattisgarh, Jharkhand territories (21 states, 2 UTs)

- 51% of PepsiCo’s volumes

-

2018

- 51% of PepsiCo’s volumes. Acquired Bihar (22 states, 2 UTs).

- Launched Sting

- Acquired dist. rights to Tropicana, Gatorade and Quaker dairy

-

2019

- Acquired Gujarat, parts of Maharashtra and Karnataka

- Acquired parts of AP & Telangana, Kerala and TN

- Acquired 5 more UTs (Total cost 1850 Cr for 7 states and 5 UTs)

- 83% of PepsiCo’s volumes (27 states, 7 UTs)

- Exports to Botswana and Malawi from Zimbabwe

- Acquired water distribution rights in Morocco (led to great vol. growth)

- 50% stake in Lunarmech for recycling PET

- Tropicana plant commissioned in Pathankot end of 2019

- QIP to raise money for acquiring territories

-

2020

- Adapted to large packs for in-home consumption (introduced the 1.25L pack instead of 2L since 1.25L fits in a fridge easily)

- Cost-cutting, rationalisation across the supply chain and innovation with light-weight PET pre-forms

-

2021

- Re-introduced Cream Bell branded dairy products

- Launched Mountain Dew Ice

- Tropicana in PET form and in small packs

- Enhanced GTM strategy for territories acquired in 2019 (more vehicles, visi-coolers, people)

-

2022

- Commissioned Bihar & Jammu plants

- Entered Congo (supplied from Zambia and Morocco as off-season of Morocco is peak in DRC)

- Lays, Doritos, Cheetos distribution rights in Morocco

- Kurkure Puffcorn co-packing rights in India to test the waters

Unstructured Notes

-

Concentrate, sugar, logistics (6%), pre-form, crown, corks, labels, cartons, pulp used for juices form the cost structure

-

Fully integrated company that produces everything from shrink films, crates, corks, pre-forms, blows their own bottles and owns the trucks and visi-coolers used for distribution

-

This is a seasonal business where bulk of the sales used to be in H1. However, there are early signs that seasonality might be changing a bit

-

For Coke, different territories are run by different people. PepsiCo appears to be taking a different turn going with a single bottler contributing to 81% of India volumes. Its an incredible amount of trust between VBL and PepsiCo

-

The trust can also seen by the keenness PepsiCo has had to hand over territories in Africa as well whenever VBL is ready. And also with handing over distribution of snacks (Lays, Doritos, Cheetos) business in Morocco and Tropicana in India, which they have not done anywhere else in the world. VBL is the only franchisee in the world that manufactures Tropicana and Lays

-

65% of volume used to be in H1 and 35% in H2 (2/3rd in Q3 and 1/3rd in Q4) in 2017 when they had mostly North territories

-

Capacity utilisation is calculated only based on peak month utilisation. Peak month, the plant is run on 3 shift basis. So 9 month production happens in 90 days (concept of 24/90)

-

PepsiCo’s territories acquired by VBL have been very underpenetrated (10-15% market share vs 40% in VBL’s northern strongholds). PepsiCo due to its reputation as a IP and brands player and other franchisees being small and fragmented, haven’t been able to execute as well as VBL (VBL has 4+% higher margins than other bottlers in the world)

-

Acquisitions that VBL does are always at around 1x current revenues in the territory and most territories VBL has acquired so far have been underpenetrated, so these have been fantastic capital allocations so far

-

MP, Odisha, Bihar, Chattisgarh, Jharkhand – 5 states had revenues of 420 Cr when acquired (30 million cases) – How much now?

-

Tropicana was acquired at 7.5 million case volume from PepsiCo. PepsiCo was using a co-packer so VBL traded Tropicana in the first year until they put up the plant. They spent a lot of time and effort in optimizing the process for margins as juices were the future. Volumes grew to 10 million cases (Rs.300 realisation, so 300 Cr) by 2019

-

Tropicana plant is Pathankot is the only plant that manufactures it. Its at 100% util. New plant will come up towards end of ‘23.

-

VBL’s distribution for Tropicana is lot stronger than “Real”, its main competitor and market leader. VBL has 750k visi-coolers and great reach for its products

-

Dairy and Tropicana are fungible in the same line. Water and CSD are fungible as well. Large packs and some packs are fungible as well (Covid time VBL shifted to large packs for in-home consumption)

-

Lemon and Lime category is estimated to have 600 million cases volume in India (another ultra-large category)

-

Nimbooz and Mountain Dew Ice, though both lemon based are not same. Nimbooz is perceived as summer drink

-

Sting is consumed by truck drivers, youngsters alike and has universal appeal. Price rationalisation in ‘20 led to 1000% growth in the year

-

Sting competes with Red Bull but is really in a category of its own since the price differential is huge

-

Sting is now present in more outlets than any other VBL product including water. Sting has 400k dedicated outlets (outlets that offer promise for pushing other VBL products in the future). VBL has 3 million total outlets, 250k international incl. (India has total 11 million outlets in all)

-

Sting has grown from 0 to 12% of volume in just 4 years

-

It takes 1-2 years for acquired territories to reach the 20-21% EBIDTA margin

-

After acquiring water rights in Morocco, the company had phenomenal volume growth. 80% growth in 6-7 yrs vs 80% growth in a single year in 2019. Water penetration helped increase CSD volumes as well. (One product helping other product’s reach seems to be a theme in VBL with Sting penetration helping CSD volumes)

-

Single-serve packs are more profitable than larger packs (out-of-home vs in-home consumption)

-

Capex required for the business will be 50% of depreciation on steady-state

-

Asset turns at 2x for greenfield and 2.5x for brownfield. Mature plants do 2.5x

-

Where seasonality is low (South/West), capex is lower (capacity is for peak season)

-

Margins will be stable around 20-21% most years and there’s hardly any scope for improving it. However ROCE growth will come primarily from improvement in asset turns (Has played out very well in ‘22)

-

Price per case varies a lot between water, CSD, Sting and Tropicana but margins are more or less in line. Realisation improved from Rs.145/case to Rs.167/case in ‘22 (Sting alone contributed Rs.8 to this as it has 65% higher realisation. Reduction in water mix, inc. in juices and dairy)

-

Depreciation – 20 years useful life for P&M, bottles etc. 5 yrs, visi-coolers is 8 years. Weighted avg. dep is 8%

-

VBL wants to do 100% PET recycling and produce their own resin and as a first step have a partnership (55% stake) with Lunarmech for 30,000 ton starting capacity

-

Company will mostly do brownfield as much as possible unless acquiring new territory. GST makes it easier to do business. Also larger plants have a distinct scale advantage over several small ones

-

83% of PepsiCo’s volumes in India. 17% left are parts of AP, J&K, PepsiCo’s JV with Tata called NourishCo and some bulk water sales. So not much headroom left in India to grow via acquisitions in beverages from PepsiCo

-

Two peak months now with Q2 and Q3 after acquisition of South and West. Morocco has peak in Aug and Zimbabwe/Zambia in December

-

Seasonality will reduce going forward with South and West regions (1/3rd of volume) and also with Tropicana portfolio, as well as Zambia/Zimbabwe which have peak season in Q4

-

Even in ‘19 when FMCG companies were struggling with growth, VBL had great growth due to under-penetration in Bihar, Chattisgarh etc.

-

Most of VBL’s rural growth has come from rural electrification. There is now a cooling infrastructure possible in a lot of places which wasn’t so few years back or didn’t have power for 16-18 hours making it difficult to justify chilling infra (mainly in UP)

-

VBL’s GTM (Go to market) – More people, routes, visi-coolers, outlets

-

Glass bottles have reduced to < 10% of volumes now (Company has depreciated/written-off glass production lines accordingly). PET bottles have higher realisation

-

Distributors generally carry 5-7 days inventory. VBL doesn’t carry more than 30 days inventory – this is the worst case and its at the beginning of season. Otherwise its 15 days inventory

-

Rural is 30%, semi-urban is 40% and urban is 30%

-

Covid behavior change of in-home consumption has continued post Covid as well since Customers now consume out-of-home small packs alongside in-home large packs which have remained stable in volume in ‘22

-

Bihar has low per capita consumption of beverages at 8-9 bottles compared to 24 for the country. VBL put up a large plant (285 Cr) which it felt could serve it for 2-3 years but was maxed out in the first year itself

-

Bihar, Orissa, Chattisgarh, Jharkhand and MP are so underpenetrated they can grow at 35% volumes

-

Summer ‘22 saw 97% volume growth and 90% capacity utilisation. VBL has set out to expand capacities by 30% in time for Summer ‘23 (they missed out on a lot of business in ‘’22 due to capacity constraints and stock-outs)

-

GST has really helped VBL. They shutdown extra warehouses and supply to distributors from their plants. Reduced time at borders and not having to have plants in every state have also helped (and during Covid to shift supplies based on state-level lockdowns)

-

Beverage consumption in India is about 2 bottles a month, whereas in US/Mexico it is about 2-3 bottles a day (30x higher). China is about 12x higher than India. Even Nepal, Sri Lanka and Pakistan are 2x ours. So as per capita income increases our beverage consumption will keep growing

-

PepsiCo is behind Coke in North America, South America and China but ahead in Middle-east, Pakistan, Vietnam. PepsiCo leads in juices with Tropicana (could be a crucial differentiator in the tussle with the future shift in preference towards juices)

Growth

Where will further growth come from is the question I set out to answer with this big exercise. It could come from

-

New territories abroad. Looks like Africa and maybe South-east Asia is ripe for the picking once VBL has stabilised their India acquisitions. This has been mentioned 2-3 times in the concalls across the years. Lot of countries in which Pepsi doesn’t even exist in Africa

-

New product lines – After Pepsi Black, Mountain Dew Ice, Sting and Tropicana, it looks likely that the company may venture into acquiring Frito-Lay portfolio and enter PepsiCo’s snacks business

-

Dairy as a category is very promising. Currently there’s capacity constraint for both Tropicana and Dairy and this should get resolved when they add an additional plant by end of ‘23

-

Volume growth as per-capita consumption increases with per-capita GDP improvements. We may see surprising growth here as the bottom of the pyramid is mis-represented in per-capita GDP numbers. Once they are pulled up, a Rs.20-Rs.30 beverage becomes affordable luxury

Risks

-

Contract renewal is done once every 10 years. Unless VBL messes up big in terms of infractions to contract, this shouldn’t be a concern. They have a 30+ years relationship now. Also VBL has proven across time and regions that it has higher efficiency of ops and with 83% volume in India and 6 countries in Africa, VBL is an equal partner with PepsiCo

-

Sugary carbonated beverages might go out of fashion with health-conscious population. VBL however appears set to capture the juice and dairy market which might replace the CSD slowly over time. Ours is a hot country and some form of packaged hydration is perhaps inevitable

-

Coke has introduced “Charged” to compete with Sting. A lot of the growth has come from Sting for VBL in the last 5 years. Have to see if Sting loses market share to “Charged”. Initial impressions however indicate Sting has better taste and is holding its own being a first-mover

-

Valuation is pricing in good growth for the foreseeable future. Management appears confident of the same and having read 6 years of concalls back-to-back, it is fascinating how clear the management vision has been so far. (Hindsight and survivorship bias of course)

Conclusion

I think we sometime underestimate the scale-invariance of growth. We assume a large player cannot grow for long. It always feels obvious though in retrospect. VBL has grown at 20% for 25 years without growth being too lumpy, very much like a HDFC Bank. There are decent signs that they might be able to do it for sometime to come as India’s per capita GDP rises and Africa rises in dominance over the next few decades. This might be a business which might survive disruptions as well. However, be wary of the price you pay.

Disc: Invested from lower levels in personal and family accounts. This is not advice to buy/sell. I am not SEBI registered and could have several errors in this post. Please do your own due diligence.

| Subscribe To Our Free Newsletter |