Q2 had 30cr of one-offs – 20cr of forex impact and 10cr of CSR. Were it not for these, EBITDA would have been 100cr so I think Q3 should safely be 100cr + benefit from drop in costs. And there’s the 70cr inflow – 20cr for UCL and 50cr from the arbitration matter.

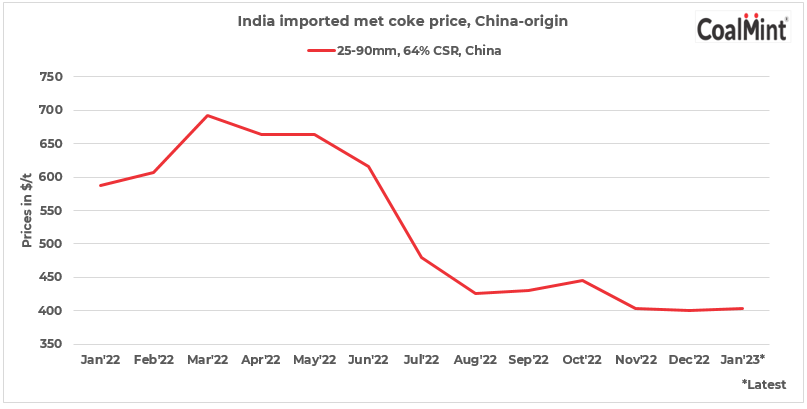

Meanwhile prices have held up fairly well and near-term outlook looks promising with China reopening.

Disc: Invested

| Subscribe To Our Free Newsletter |