Hello @njain1983 . Thanks for the great post, would be great if you could also include a few supporting links for others to read along.

I believe the key thesis, which has been repeated ad nauseum, is two aspects,

-

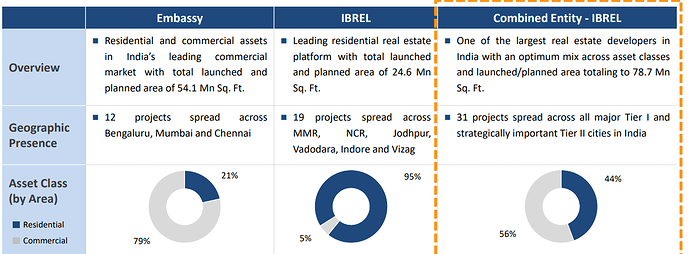

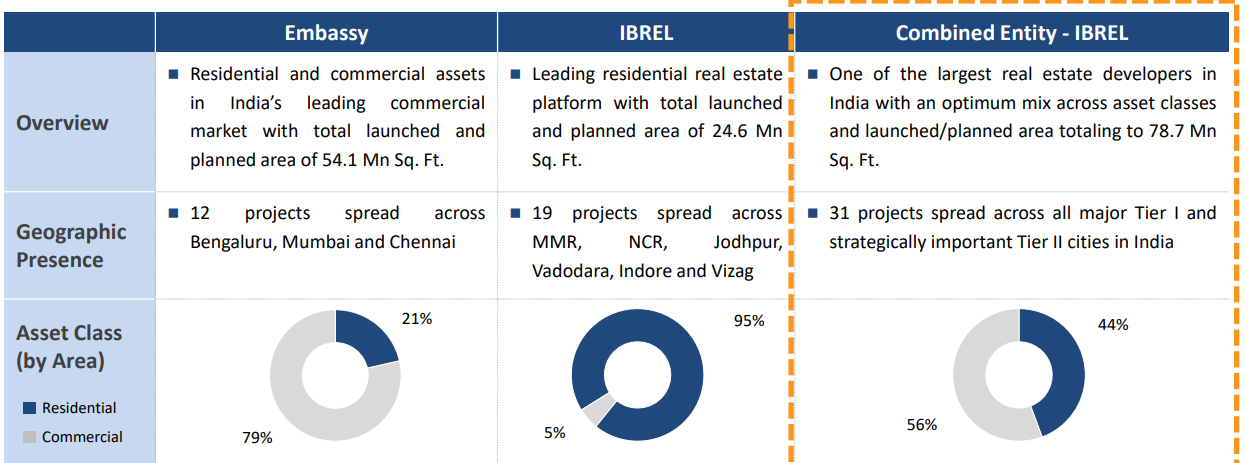

Moving to a very balanced residential + commercial mix through the merger

– 44% residential & 56% commercial link

-

The ability of the Embassy group to

a) manage liquidity for completion of IBReal residential projects & realize the surplus from projects

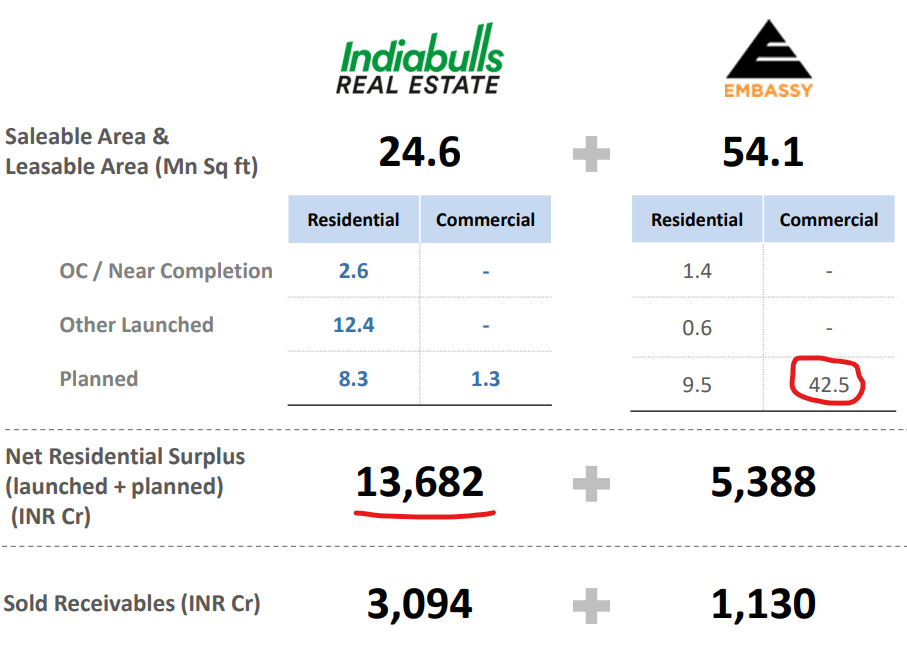

b) monetize their planned commercial portfolio through their listed REIT arm. 43mn sq ft

It seems from the latest court proceedings of 05.01.2023, there are multiple aspects which were discussed and hoping the next hearing on 03.02.2023 will assume significance towards concluding majority of these.

(1) Income Tax department trying to wrap around their findings from Embassy raids from June 2022 and trying to link them to IBReal – which they are apparently not.

(2) Violations of disclosure norms and other aspects filed by minority shareholders. Again if Mr. Dharanish is acting a front end for some other interested party remains to be seen, but disclosures obtained because of this activist movement has been beneficial for minority shareholders – to say the least.

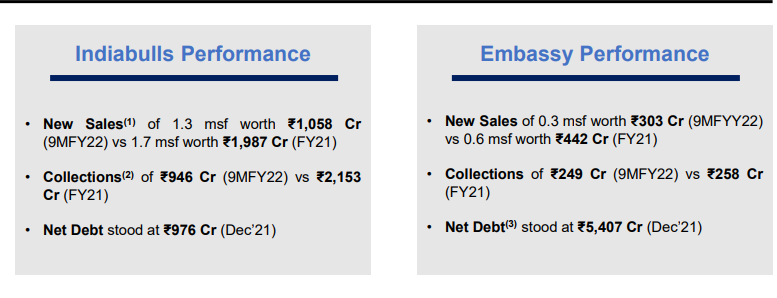

Yes, can’t agree more. We have seen a very high debt number from Embassy being floated towards December 2021, of 5,407 Cr along with all cash flow issues you highlighted.

Subsequently from the Jan 4, 2023 disclosures, we have seen this coming down to 4300 Cr.

Again the end use of debt is debatable because the IB Housing term loan originated in April 2020 as per the filing, while the promoter buyout happened in 2019.

Not all of the IBReal landbank is promisable and they will monetize certain parcels as was highlighted in the last conf. call back in June 2022. Going back to the buy thesis, I do not see the core thesis being derailed from this non-core asset monetization.

Very fair arguments, given Sameer Gehlaut’s minority stake in Dhani and “Promoter” tag not being applicable.This could indeed be some sort of quid pro quo.

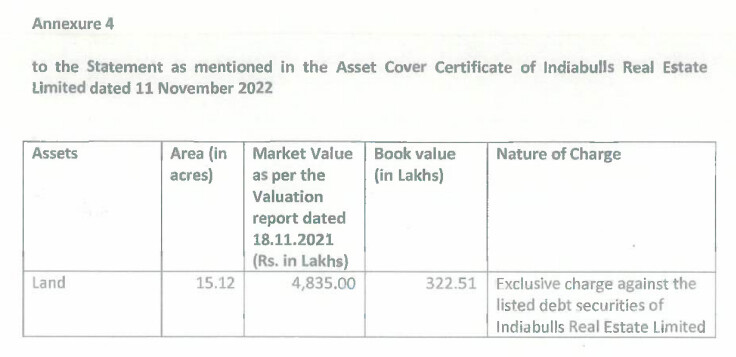

However, their realization of 240 Cr for 35 acres is double the last revaluation disclosure from Q2FY23 filings

IBReal sold the Hanover Square property in 2019 to SG for £200 (purchase price £162 Mn).

From the Jun-22 concall only £60mn is left unpaid at that time.

SG is focusing on the London RE market through this new company Clivedale London, launching the new service apartments and premium hotels near the Hanover Square area. So I am assuming the remaining dues are recoverable for IBReal.

| Subscribe To Our Free Newsletter |