Q3 FY23 Result

Source : investor presentation

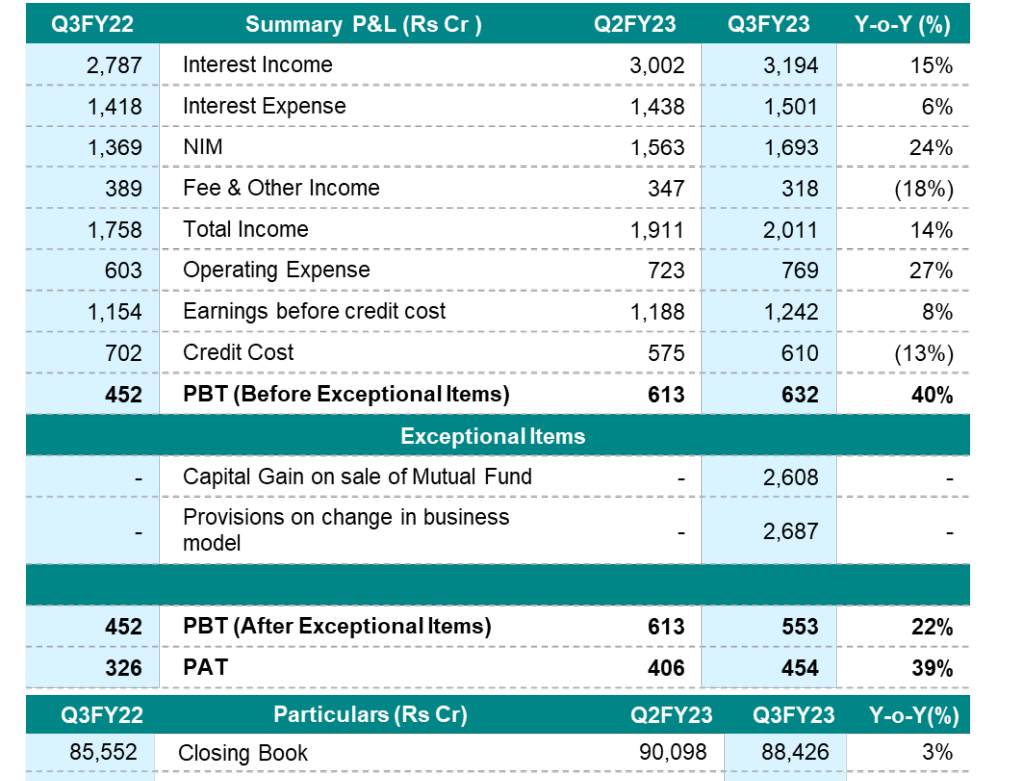

1.Management has mentioned that they have provisioned Rs. 2687 Cr. as one time provision for acclerated sale down of wholesale book and at the same time they have shown capital gain of Rs. 2608 Cr. from sale of Mutual Fund business to HSBC. Perhaps management is cleaning NPA mess in tax efficient manner. These provisions are substantial and management owes a detailed clarification to shareholders, how this mess was created and kept pending and whether any specific drive ( like Lakshya 26 etc.) is required to reflect the NPAs. Still wholesale book is Rs. 31010 Cr ( down from Rs. 37597 Cr. QoQ), so don’t know whether more provisions are left.

-

One thing is clear that management is aggressively taking steps towards retailization of loan book ( retail book from 52040 Cr to 57000Cr QoQ) and NIM+Fee +other income is 11.38% for retail, compared to 8.88% of total book. It is only 3.74% for whole sale book. It means whole sale book is a big drag on over all profitability.

-

Performance of this quarter in term of disbursement, NIM, RoE is better in comparisopn to YoY and QoQ.

-

Consolidated GS3 is 4.21% ( NS3 1.72%, PCR-60%), while retail GS3 is 3.47% ( NS3- 0.73%, PCR- 79%). Still a lot more room for asset quality to improve. since, cost of fund is 7.54%(in comparison with 3-5% of banks), and NIM is 8.8% ( 11.38% for retail), it means their interest cost is quite high, so borrower profile may be risky. Management in their Lakshya 26 target also envisages GS3 <3 %.

-

Overall forward looking results with clear direction.

Disclosure: Invested and no transaction in last 90 days

| Subscribe To Our Free Newsletter |