Some notes.

Disclaimers:

- Dont Own

- Open to Correction

- Aim to be as objective as possible; leaving subjective interpretation to reader.

Was interested in the business and the growth aspects ahead. Driven by the adage, ‘what the rich do exclusively now, will be emulated by the rest in-future’ – there is room for plenty of customers ahead. How many will be exclusive members (direct to DreamFolks) and how many via intermediaries (card benefits) is open to estimate.

Went through the RHP and presentation and Frost & Sullivan report (FSr) which is quite exclusively splashed by the company.

- FSr was paid for by the company.

-

IPO was completely offer for sale. Hence nothing went to the business per-se.

-

There are quite a few associated companies with DFS amidst them. There have been quite some monies exchanged either terms of advances-given or expenses-payble etc. Via Google one can find there are many companies hosted at (possibly) a flat in a housing site in Delhi.

Some companies share the same accounting email address too.

DFS now has a different corporate address – Gurgaon, Haryana.

Related party transactions need to be better understood.

- Is it the norm that intermediary like DFS has to indemnify the Operator for services?

- Un-stamped or inadequately stamped documents and enforcement of rights is an open-to-interpretation question.

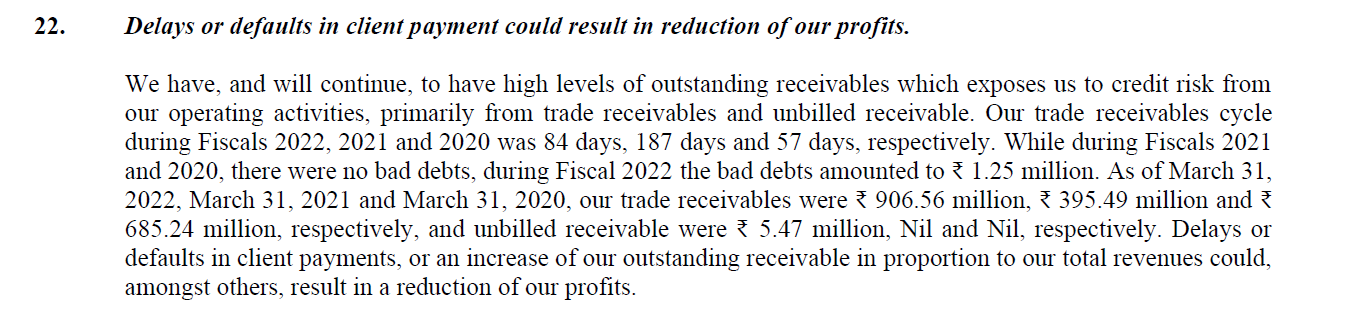

- A categorical warning-statement that receivables will be high.

- An unsettled matter – possibly legal – but not explained further, exists.

- There are 60 (sixty) full time employees

- (This point is subjective) With 60 employees, and DFS claiming to be Asset Light and almost always hiring (or facilitating) external services, the company has higher assets in terms of Motor Vehicles than Computers. As DFS provides platform oriented facilities, would have felt their investment in IT should have been the highest among assets. Are these vehicles for usage of company personal? Or are they used for ferrying clients? How many – actual number – of vehicles are owned? Elsewhere there is a mention of hiring external vendor for vehicular services – so how differentiated are these company owned vehicles? At 54mn INR, this equates to 5.4 crores.

Subjectively – my opinions –

Have not been able to find the comfort in understanding Management positioning or MoS in terms valuation to take a position.

Am enthused by the ‘runway for growth’, ironically – it is literal in this case as business deals with Airports (runways) – that lies ahead for India in terms of population (volume), aspiration and airports. A cube-of-growth factors, that very few business can claim to boast of.

With IPO mania being the season, perhaps as other new age companies have weaned themselves away from highs after a year or so of running, DFS may feel the heat too. Especially after the Anchor Investor lock (of 1 year?) ends.

| Subscribe To Our Free Newsletter |