Hi @smallcapstalker ,

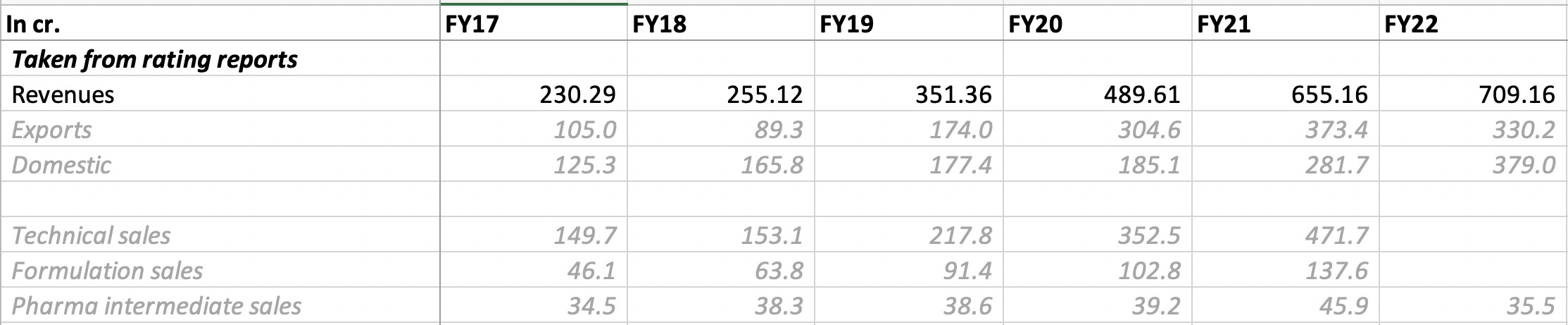

Thanks for adding your notes. I am sharing the breakup of their sales (taken from Care rating reports).

As we can see in the above figure, the large improvement in financials happened from FY18, with rapid scaleup in technical division. This coincided with scaleup in molecules such as Prosulfocarb, Folpet, Cymoxanil and Thiocarbamate. Captan has been a very old product for IPL.

Captan, Folpet and Thiocarbamate account for 40-45% of revenues, followed by Prosulfocab which accounts for 25-30% of their sales (Q3FY22 concall transcript).

Its very interesting to note that in most of these molecules (Prosulfocarb, captan, folpet), they are market leaders with 20-25% of global market share and the sole Indian manufacturer at scale. This is one of the reasons for their superior margins.

In past couple of years, they have launched newer products such as Aclonifen, Triclopyr, and Carboxin which are scaling up. These 8 technical molecules (Prosulfocarb, Captan, Folpet, Carboxin, Aclonifen, Triclopyr, Cymoxanil and Thiocarbamate) account for majority of their turnover and most revenue growth has come from these products.

I have been following IPL for a while and am sharing notes from the past few calls.

Major raw material: Chlorine, tetrahydro phthalic anhydride, carbon disulphide, technical grade urea, di-n propylamine, benzyl chloride

Imports RMs: Tetra Hydro Phthalic Anhydride (THPA), Ammonium Thiocyanate, Di N Propylamine and Cyano Acetyl Ethyl Urea from Taiwan and China

21.09.2022

- Use rice husk for fuel (price has increased from 300 to 900/quintal). This contributes around 2% of cost of production

- Have been unable to full price hike for energy cost increase, raw material increase has been passed on

- MNC contract prices are reset quarterly

- Sandila has seen lot of brownfield expansion. It was 19’500 MTPA in FY21, then increased by 2000 MTPA in FY22, has again increased by 2000 MTPA and will increase further in next 6 months to reach 27’500 MTPA

- Hamirpur: EC clearance in progress, 2 stages finished 1 remaining (environmental impact assessment) which is being submitted. Expect to get EC clearance by November. Will make conazole based fungicides, 2 herbicides and 2 intermediates. Expect to start operations by FY24Q3

06.10.2022 Care ratings report

- Out of 8 planned new products, 5 were introduced in FY22. 1 was launched in Q1FY23 (Pretilachlor technical as a part of backward integration)

- Domestic distribution network consists of 3500 distributors and sales force in Gujarat, Rajasthan, Maharashtra, Andhra Pradesh, Madhya Pradesh, Punjab, Haryana, Uttar Pradesh, etc.

- Major raw materials used in making captan technical are imported from China and Taiwan

- Imports Tetra Hydro Phthalic Anhydride (THPA), Ammonium Thiocyanate, Di N Propylamine and Cyano Acetyl Ethyl Urea from Taiwan and China

- Specializes in manufacturing of fungicide based technical

29.11.2022 CNBC

- Sales growth will be 30% in FY23 with export growing by 40%. Expect 25%+ growth in FY24

- H2FY23 margins will be at same levels as H1

- Technical and API margins higher vs formulations

- Capacity will increase to 27’500 MTPA by FY23

- Major export markets are Australia and Europe. Haven’t seen any order cancellation from Europe

29.12.2022 BQ

- EC clearance for 100 tons/day and 2 tons/day of API at Shalvis Specialities Limited, first block will come onstream in Q4FY24

- When Shalvis Specialities comes on stream, total capacity will increase to 57’500 MTPA

- Will do annual Capex of 100-125 cr. over next 3-4 years

- Incremental fixed asset turns will be 2.5-2.7x

- Expect FY23 sales growth to be around 30%, and expect growth to be maintained in FY24

- 20% of raw materials are imported from China, and 10% from other geographies

- Hoping to end FY23 at 24-25% EBITDA margins

- Export incentive has been reduced from 2% of sales to around 0.8% of sales

17.01.2023 CNBC

- Newly launched herbicide (from Sandila) can contribute 100 cr. annual revenues. At peak capacity utilization, this can go up to 150-160 cr. Margin will be 22-25%

- Will be marketing this herbicide in India and Europe. Have started talks with 5 customers

- Out of 8 products promised during IPO, 7 have been launched with 1 to be launched in March 2023

- Margins will go back to 24-25% when current high priced inventory gets used up

Disclosure: Not invested (no transactions in last-30 days)

| Subscribe To Our Free Newsletter |