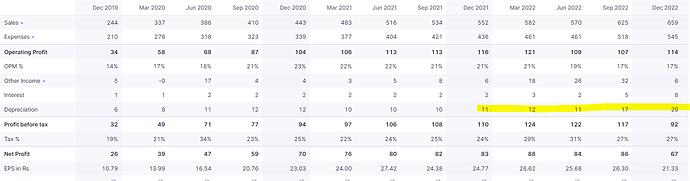

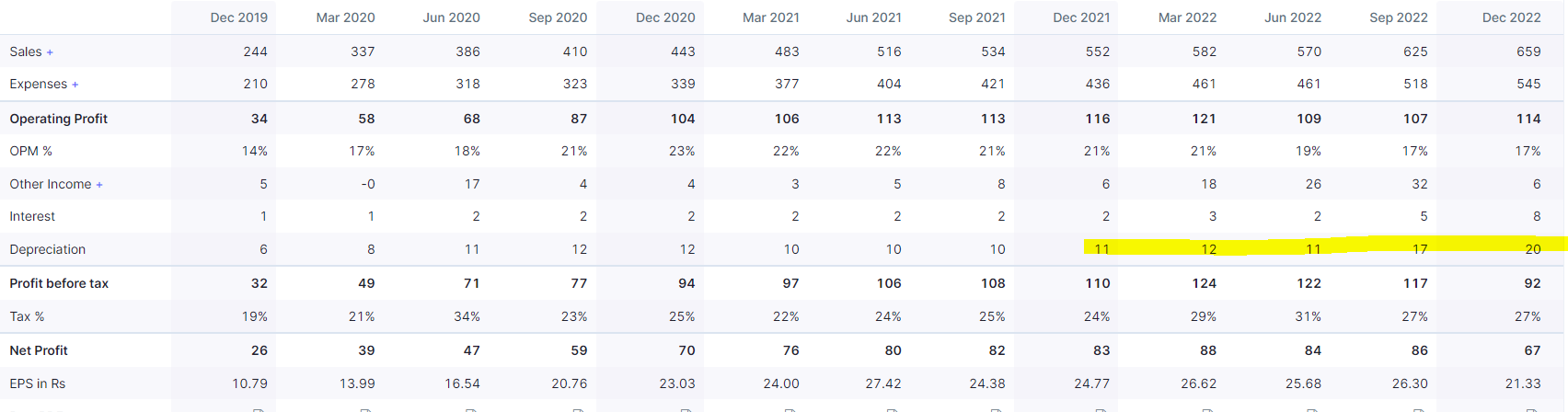

Impact of MST acquisition on Mastek Q3-FY22 P&L

-

Mastek took a debt of 240 cr at 3.5% per annum. Interest in this shall be around 2.1 cr per quarter.

-

Depreciation has increased from 11 cr to 20 per quarter. In short other things being equal- MST acquisition has added 11 cr of expenses to Q3 P&L.

In the current quarter, MST revenue was $10 million USD, so assuming 10% net profit margin, what profit MST has contributed is negated by acquisition cost.

The acquisition cost (interest + amortisation) has continued for many years now. The interest component shall come down, but amortization (done over 1 – 6 years as per accounting norms) will remain at an elevated level.

Few pointers on PAT reduction in Q3 and future levers.

-

Q3 has a reduction in Fixed Price contracts. Fixed Price contracts are mostly offshore-based and more profitable. There is 3% reduction in Q3 as compared to Q2 or Q3 of FY22.

-

Utilization could be higher. At 69%, which is considerably lower. Due to the high demand for resources last year, companies had to keep resources on a bench in case of need. However, the scenario has now changed. Looks like they have hired a decent number of graduates so utilisation shall inch updates from here on. They are looking at the 75-80% range (as per management). This is the most likely lever which will contribute PAT.

3- 12 LTM attrition is 23.3%, which can go to high teens (15-17%) in the next couple of quarters. This shall reduce their cost.

4- There was a provision of bad debt in the result. They have not mentioned the exact amount, but it would be a few crores.

These four factors shall inch the PAT upwards in the next few quarters.

Q2 PBIT was the same as Q3, but it had an exceptional gain of 25cr, which resulted in higher PAT. Otherwise, it was a bad result considering that they had two months of MST revenue in Q2.

Last year MST revenue was 240 cr (approx 30 million). Assuming it grows to $40 million with 10% PAT margin, that will be around 30-35 cr PAT. However, interest and depreciation

costs will be around 40-44 cr. This means MST will continue to drag overall Mastek profit for some time now. Even if Mastek rebound in the next 2/3 quarters, they are likely to be near the 75-85 cr profit range.

| Subscribe To Our Free Newsletter |