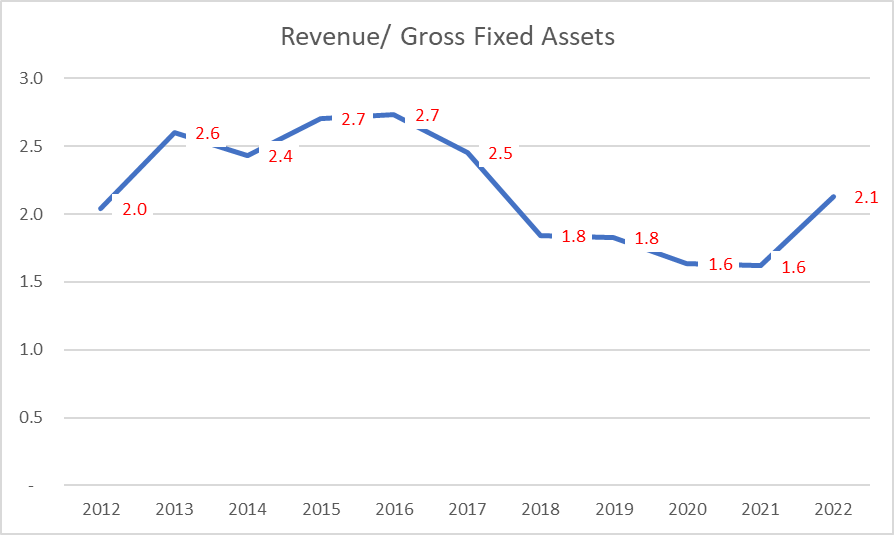

One thing I am unable to understand is that if you look at historical Revenue/ Gross Fixed Assets, they have ranged in the range of 1.8 on the low (ignore COVID years) and 2.7 on the high. The current Gross Block is INR 310 crs. Planned capex over next couple of years is INR 40 crs. That takes the Gross Block to INR 350 crs. If I apply the peak Rev/ GFA of 2.7 to this, the revenue potential from this asset base is INR 945 crs only. However, the management says that they can reach a revenue of INR 2000 crs with this Gross Block of INR 350 crs. That implies an Rev/GFA of 5.7. This looks way high relative to it’s own history as well as relative to the peer-set. What am I missing?

| Subscribe To Our Free Newsletter |