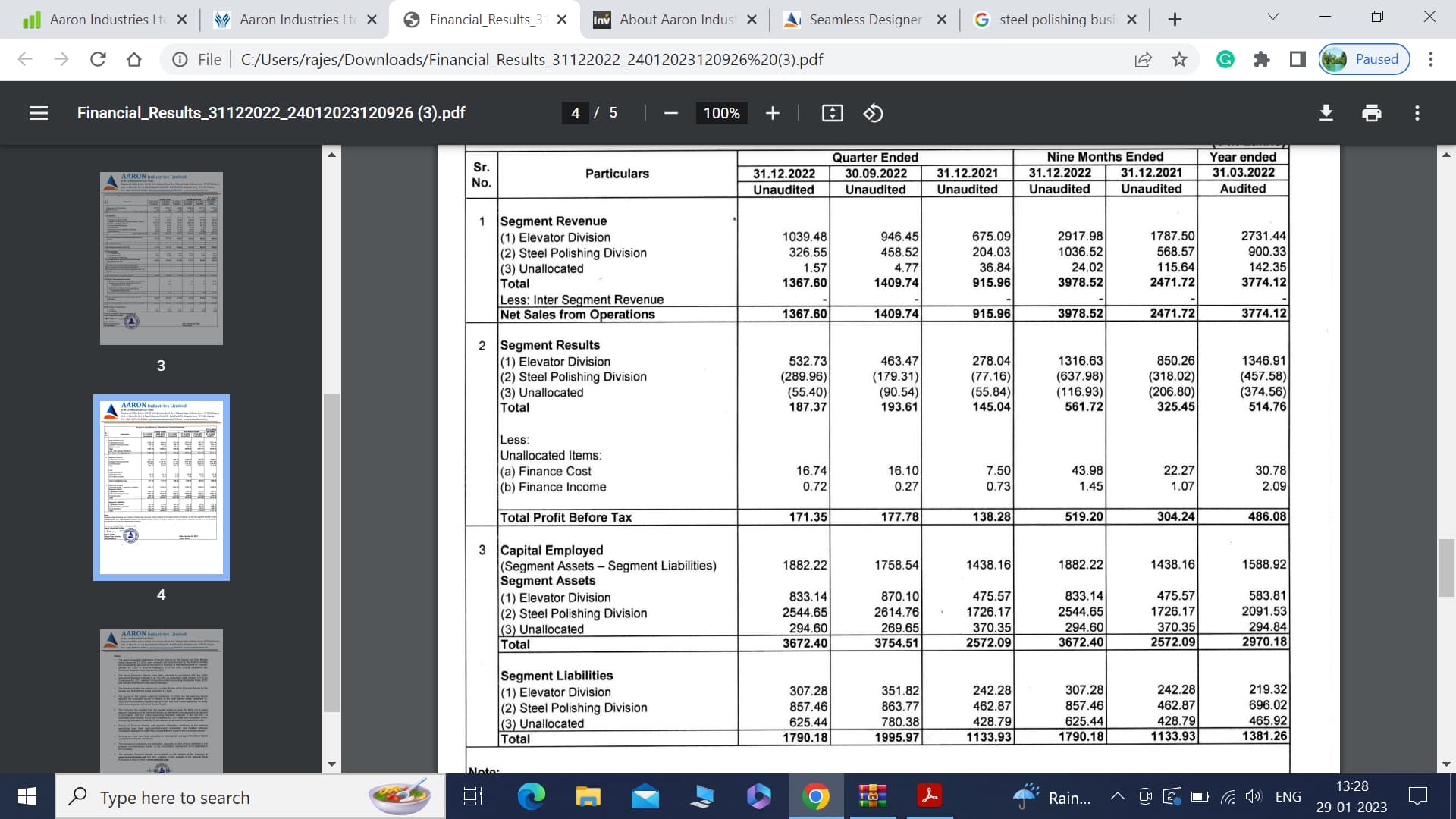

Not much information has been provided by the Management on steel polishing business, however can be seen that highest amount of capital has been employed in this segment, and the segment is continuously in loss.

Steel polishing is the backward integration of the primary business of elevator doors and cabins. Chairman says in AR 2021-22,

“Further, by New Product Development in our Kosamba Unit, operations will

play a major role towards our growth in the Steel polishing segment. During the Year, we have witnessed a healthy growth in this segment and reported revenue of Rs. 900.33 lakhs as against Rs. 769.59 lakhs of the previous year, an increase of 16.99%. This unit also helped us in the supply of SS sheet which is used as raw material of primary products i.e. Elevator doors and cabins. That largely reduced our dependency on external providers.”

Polished steel is a commodity, and lately there has been steep decline in steel prices. It may be a reason of loss in the segment. I am not sure how internal segment-wise accounting is being done by the company, primarily, at what prices polished steel is transferred from this segment to elevator segment. If it is done cost basis, the segment will show losses due to higher depreciation/interest in the segment. But certainly, we need to ask this question from the management.

| Subscribe To Our Free Newsletter |