From my reading until now, the highest incremental value creation in next 2-3 years will come from PVDF. So i want to analyze PVDF in this post as exhaustively as possible.

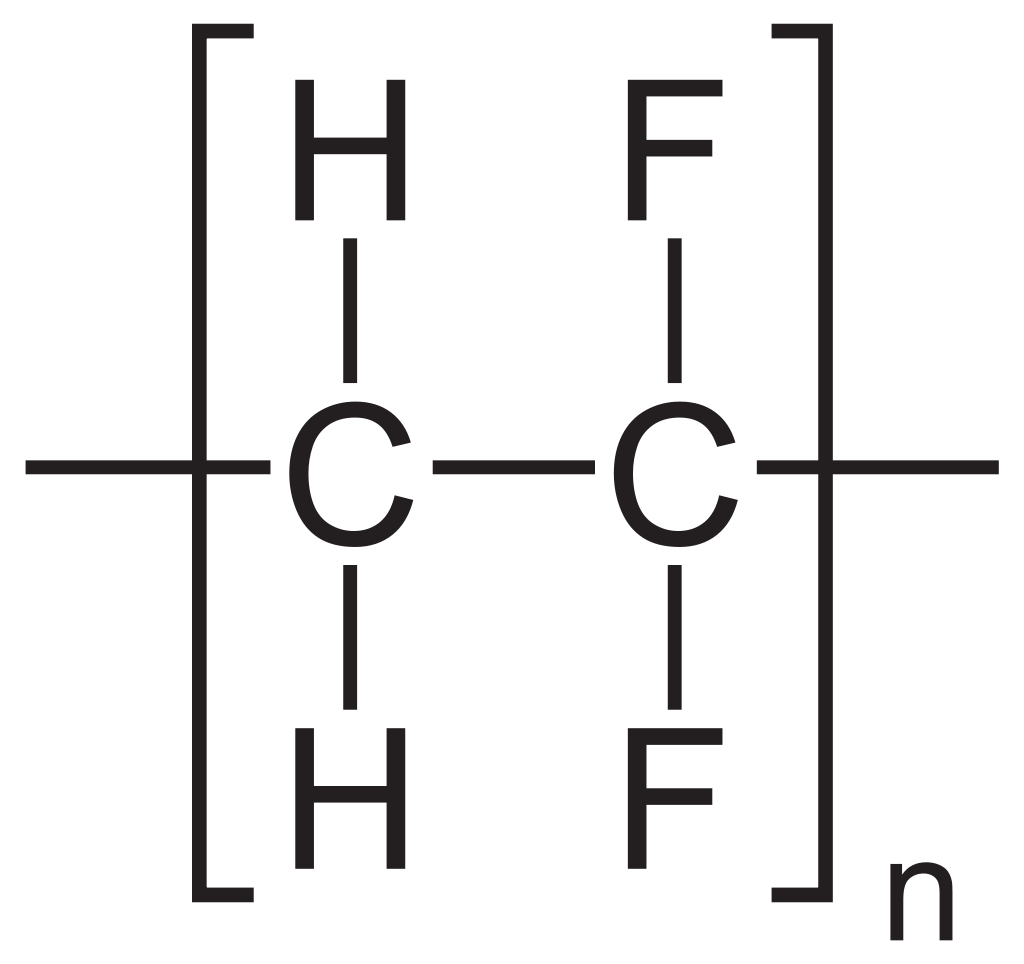

The molecule

This is the molecule. Polyvinylidene fluoride or polyvinylidene (PV) difluoride (DF) is a highly non-reactive thermoplastic fluoropolymer produced by the polymerization of vinylidene difluoride (VDF).

PVDF is sold under many brand names including KF (Kureha), Hylar (Solvay), Kynar (Arkema) and Solef (Solvay).

The word piezoelectricity means electricity resulting from pressure and latent heat. Piezoelectricity is one of the critical properties of PVDF which make it applicable in batteries.

PVDF has also been subjected to high-heat experiments to test its thermal stability. PVDF was held for 10 years at 302 °F (150 °C), measurements indicated no thermal or oxidative breakdown occurred. This also makes it ideal for EV battery applications. PVDF is a standard binder material used in the production of composite electrodes for lithium-ion batteries, PVDF is used because it is chemically inert over the potential range used and does not react with the electrolyte or lithium.

https://hal.science/hal-02557122/file/Ordonez2016.pdf is an interesting read to understand lithium batteries. PVDF is used as binder for both cathode & anode:

The longevity of Li batteries is guaranteed by the PVDF’s chemical resistance in the extremely harsh surroundings of the lithium-ion batteries, which contains a large amount of lithium salts. PVDF is also used as a dispersion agent in Lithium ion batteries to evenly distribute the active electrode material on the battery’s current collector, leading to improved battery performance. A dispersion agent in the context of Lithium ion batteries refers to a material that is added to the electrode mixture to distribute the active material evenly and prevent clumping or aggregation. The dispersion agent improves the uniformity of the electrode mixture and enhances the overall performance of the battery by ensuring a more efficient use of the active material and better electrical conductivity. In the context of Lithium ion batteries, the active material refers to the substance that participates in the electrochemical reaction taking place in the battery. The active material is typically a metal oxide or a polymeric material and can be either the cathode or the anode material. The active material determines the energy and power density of the battery and its overall performance.

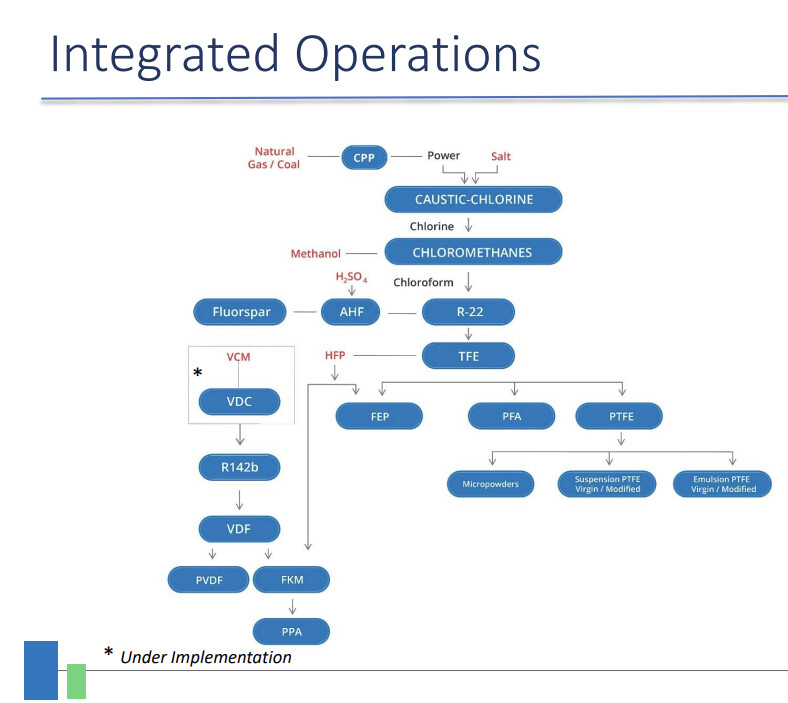

Value chain for GFL

Let us also understand how GFL produces PVDF.

GFL goes from VCM => VDC => R142b => VDF => PVDF. This level of backward integration is one of the strong competitive positioning GFL has.

According to this market research: Polyvinylidene Fluoride (PVDF) Market – Growth, Trends,

The global PVDF market is highly consolidated. The top 4 players account have a marketshare of around 90% in 2021. The top players are: Arkema, Solvay, Kureha, & Dyneon LLC (3M Company).

According to this: Polyvinylidene Fluoride (PVDF) Market – Growth, Trends, COVID-19 Impact, and Forecasts (2022 – 2027) the PVDF market is growing at 20% CAGR in next 5 years. According to https://www.globenewswire.com/en/news-release/2022/04/20/2425284/28124/en/Global-Polyvinylidene-Fluoride-PVDF-Market-Overview-2022-New-Energy-Markets-Driving-Demand-for-PVDF-in-a-Big-Way.html the asian PVDF maket will grow at 16%. Overall, we understand that this is a fast growing global market, primarily due to application of PVDF as binder for electrodes in batteries.

Competitor Analysis

While @rupeshtatiya sir’s post talks about technical requirements required from PVDF binders here:

I wanted to focus on the capacities, capex plans & extent of backward integration to gauge the extent of competitive advantage if any which Gujarat Fluoro might hope to enjoy.

Arkema

Sources:

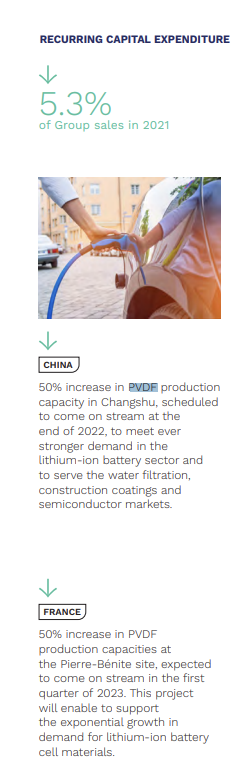

Arkema has announced several capacity expansion projects in China & France

Arkema reports PVDF under brand Kynar under the ADVANCED MATERIALS segment. This segment has 22% EBITDA margins & 3B Euro sales. This segment will be 35-40% of arkema sales in 2024 so is important to them.

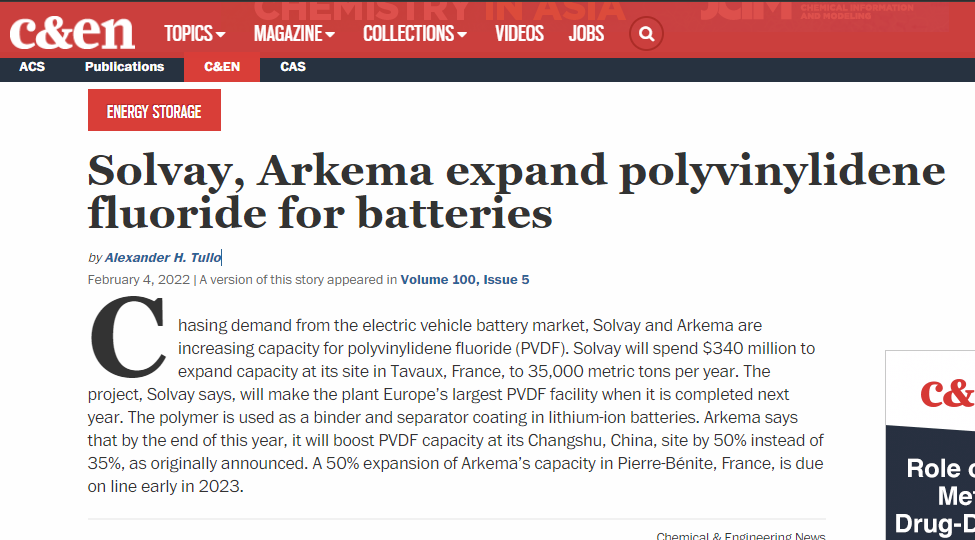

They expanded PVDF capacities by 50% in 2021 in both China & France

Arkema is also working on PVDF binders which consume 20% less carbon in the manufacturing process & are those more environmentally friendly.

In this segment, Arkema considers itself to be market leader & expects 10% annual growth. This means that their 50% capacity expansion should probably be good for next 4-5 years or so. Given that they have a plant in France, we have to very closely understand why any european customer would prefer Gujarat fluoro’s PVDF over Arkema’s which has been produced in France & is also environmentally sustainable.

We know from Foranext®: fluorinated monomers gas for fluoropolymer synthesis- Arkema Group | Arkema Global

that arkema manufactures HCFC-142b so it is at least partially backward integrated for sure.

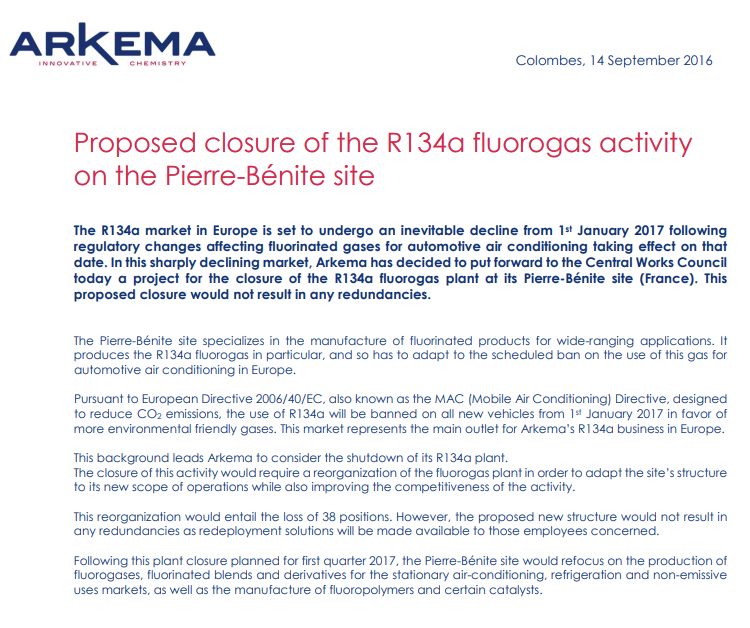

One thing to note here is that arkema did close its R134a plant in 2016.

This means that it is possible that they might find it difficult to expand R142b capacities too (need to work more to validate or invalidate this).

A 50% expansion of Arkema’s capacity in Pierre-Bénite, France, is due on line early in 2023. I havent been able to find Arkema’s total PVDF capacities.

Solvay

Solvay is also doing capacity expansion for PVDF.

Solvay will in fact have largest PVDF capacities in Europe at 35,000 ton (doing capacity expansion for 300 M euro). Solvay is also doubling capacity in china: Solvay doubles PVDF capacity in China ahead of schedule to meet growing demand for EV batteries

Solvay concall:

Solvay is Also targeting NA market. Solvay also has access to Fluorspar mines similar to GFL. Solvay’s complex in France is fully integrated.

Solvay is also going to produce PVDF in North America

I also learned why these cos do not disclose capacities. They consider it to be a competitive advantage/secret (which makes sense)

Their investments in USA will make them the undisputed leader for USA.

On pricing they basically point out that they are able to sustain margins & pass cost increases to customers

3M

I guess this is the one with most recent news. As @spatel sir posted:

3M will stop manufacturing all fluoropolymers:

3M will discontinue manufacturing all fluoropolymers, fluorinated fluids, and PFAS-based additive products. We will help facilitate an orderly transition for customers. 3M intends to fulfill current contractual obligations during the transition period.

The interesting thing i learned while studying 3M’s production stop is that it was based on ” Shareholders have also called for production of the chemicals to stop. Investors managing $8 trillion in assets earlier this year wrote to 54 companies urging them to phase out their use.” Which made me curious about which 54 companies investors asked to stop producing PFAS. We already know from sandeep sir’s post that Gujarat Fluoro does not / will not use PFAS in making its FP.I could not find 3M’s pvdf capacity although we do know that 3M sells PVDF: https://www.3m.com/3M/en_US/p/d/b40070223/

This would result in some supply vaccum. However given that 3M plants are primarily in USA, given that solvay intends to become largest PVDF manufacturer in USA, 3m’s loss might be solvay’s gain & GFL might only benefit indirectly through a demand-supply mismatch, if any.

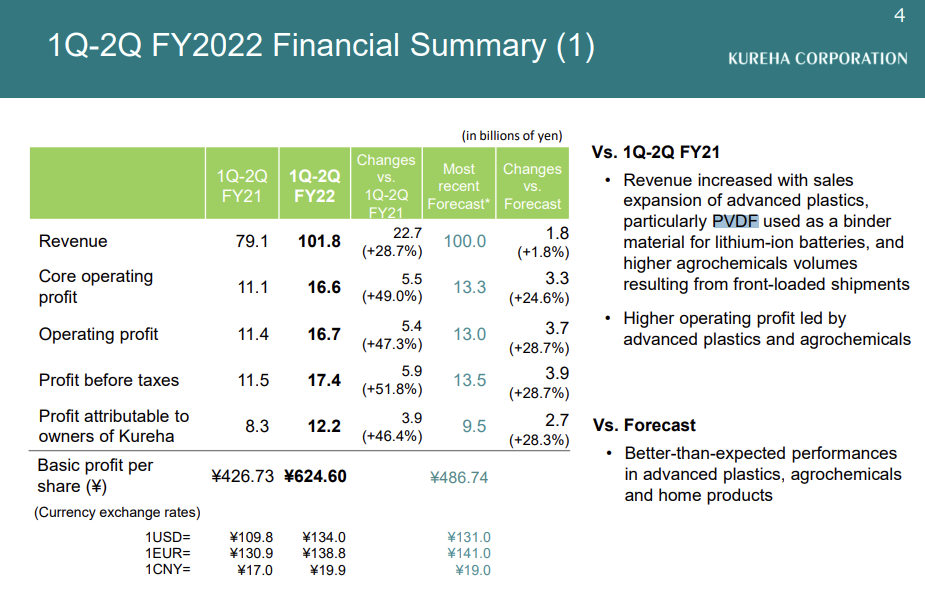

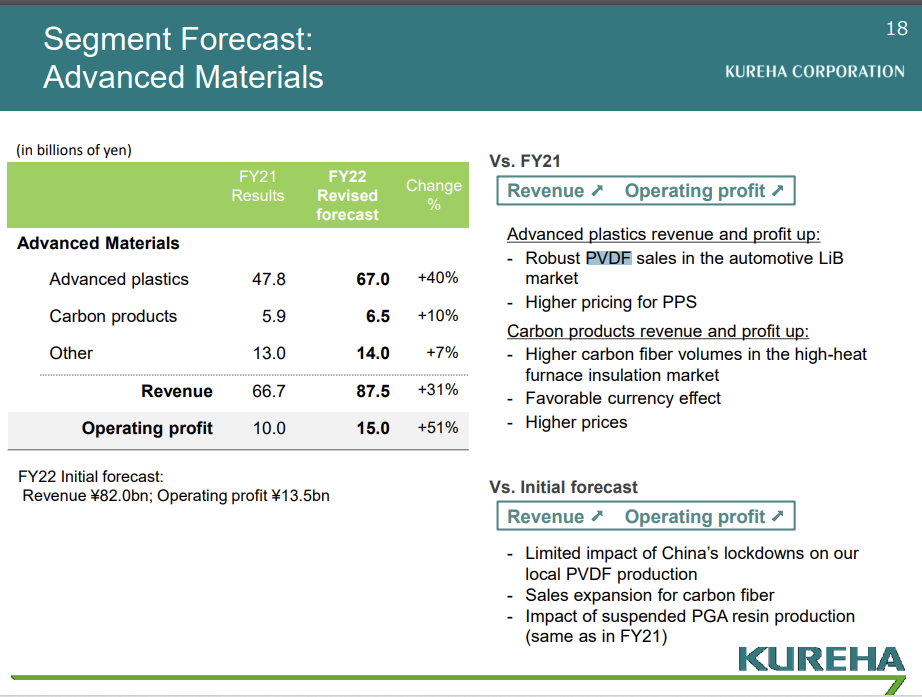

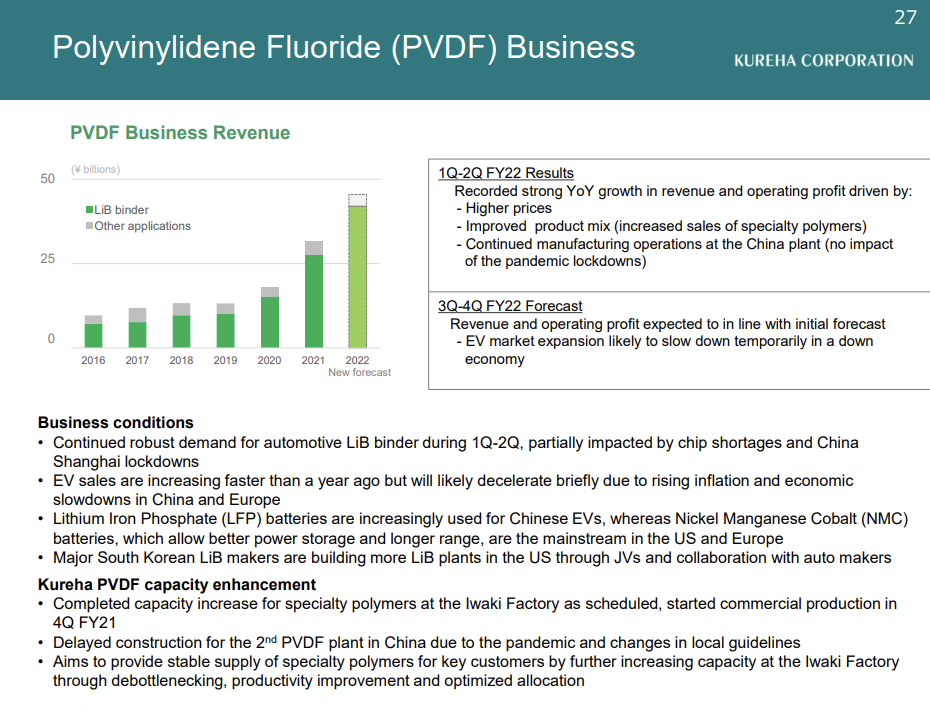

Kureha

Kureha had 11000 ton PVDF capacity. Kureha is also increasing (tripling) PVDF capacities in China.

https://www.kureha.co.jp/en/newsrelease/docs/20210720en.pdf with a focus on battery binders for LiB.

PVDF sales has been supporting kureha’s sales growth

PVDF is highly profitable for kureha

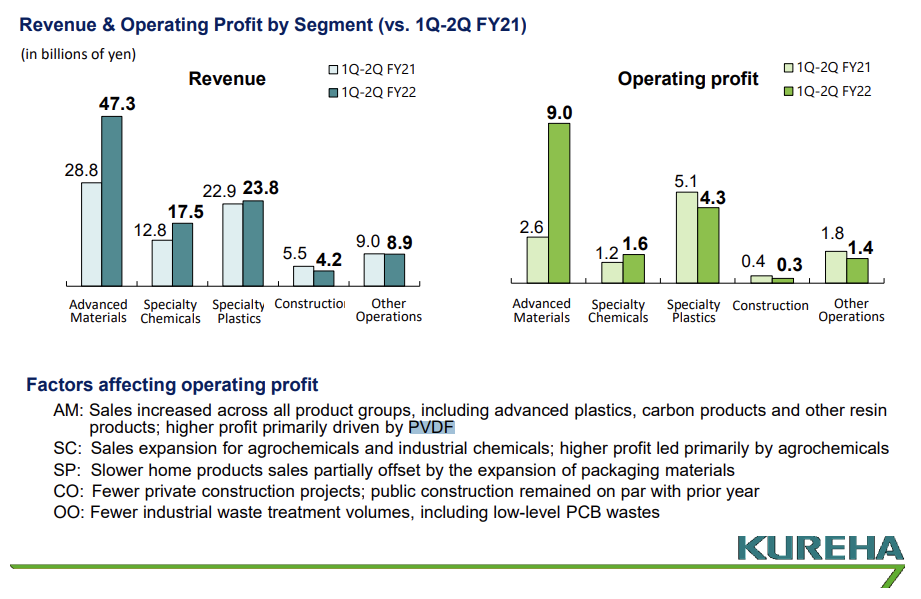

Kureha reports this under the advanced plastics segment & it is growing quite fast, also improving overall profitability for kureha

Kureha will go 3000 cr or so of PVDF sales in FY22. Economic slowdown remains a key risk specially since all PVDF makers are expanding capacities so aggresively.

Overall conclusions

- In my assessment it might be difficult for GFL to break into USA due to localization requirements which incentivize local production heavily. The Inflation Reduction Act (IRA) requires that EV manufacturers source 40% of critical battery minerals domestically or with free trade partners by 2024 . That percentage increases to 80% in 2026. And mines and battery material processing plants don’t come on at the flip of a switch. We know that PVDF binders are not a large part of the value of the battery but solvay has 1st mover advantage in USA so might be difficult for GFL to break through in NA market.

- Demand supply situation seems delicately balanced. All leading players understand the explosion of demand & most are setting up factories in China. Even if production stops in europe, it is not clear why or how GFL might be able to compete successfully against Solvay, Kureha or Arkema’s China plants given low power costs in China (power is one of largest raw material for FP).

- Perhaps In my understanding the best market GFL might be able to target is the domestic market which supported by high cost structure of European plants & some form of ADD on chinese plants, GFL might find itself in a near monopoly position for Domestic consumption. This space needs to be watched closely to see who is setting up lithium ion battery manufacturing in india & how.

Disclaimer: have a small position, but to be honest this is one of toughest companies to analyze & forecast for, each molecule is like a large industry in & of itself. I am not very confident GFL can create value without too many variables falling into the right place:

- ADD on chinese imports

- Domestic manufacturing picking up

- Realizations remaining favorable vs non-ADD imports

Ps: The reason i prioritised pvdf is that it seems the largest & fastest growing high realisation molecule. LiPF6 can be larger but also has threat of substitution by lifsi. PFA is much smaller market size. Same for fkm. Ptfe is a slow growing market.

| Subscribe To Our Free Newsletter |