Kigali Ammendment

The Kigali Amendment to the Montreal Protocol is an international agreement to reduce the consumption & production of hydrofluorocarbons (HFCs). It is a legally binding agreement & has been signed by 190+ countries, All Major countries included.

Many of the Ref Gases which serve as feedstock for FP (R22, R32, R125, R142a) are HFCs. Let us analyze how each Major geography is treating Kigali ammendment. This will have rammifications on 2 aspect of GFL business:

- Ref gas prices might go up as supply is reduced

- Integrated FP players might continue to do well due to structural reduction in supply of Ref gases.

Why production & consumption caps?

While HFCs are not damaging ozone layer, their green house warning potential is 12000-14000 times that of CO2.

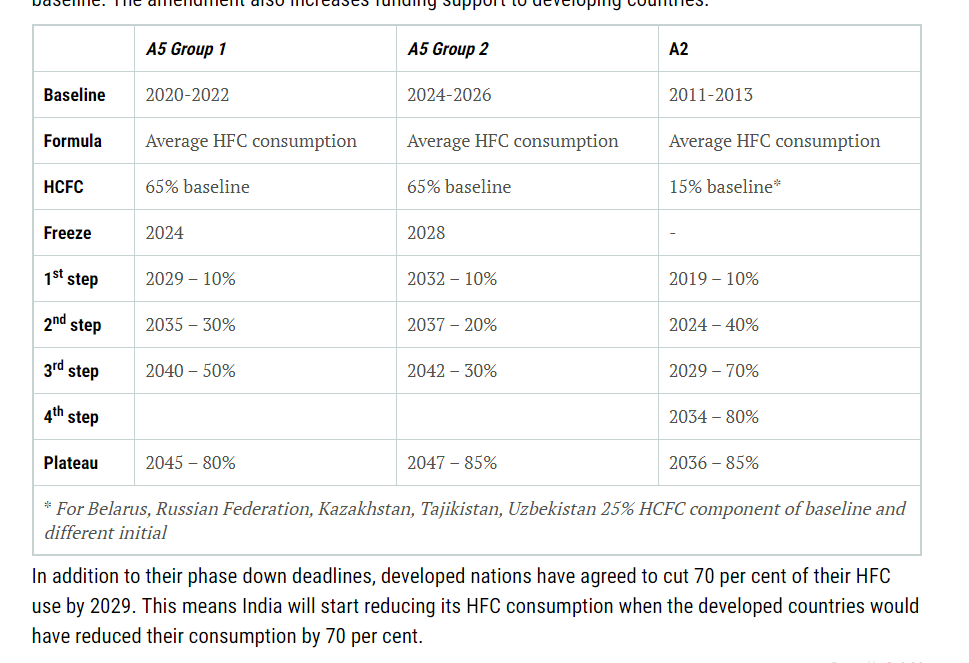

Broad Picture

Src: https://www.downtoearth.org.in/news/climate-change/countries-adopt-kigali-amendment-to-phase-down-hfcs-56008

A2 is countries like Europe, USA

A5 Group 2 is countries like India

A5 Group 1 is countries like China.

We can see that developed world is reducing capacities much more aggressively than Developing world. Even in that bucket, India would reduce much more slowly than China.

India

India ratified in 2021 the Kigali ammendment:

https://pib.gov.in/PressReleasePage.aspx?PRID=1746946

Per this document:

India will complete its phase down of HFCs in 4 steps from 2032 onwards

with cumulative reduction of 10% in 2032, 20% in 2037, 30% in 2042 and 85% in 2047.

This means, that indian producers can produce (as allowed by international law) fairly significant volume of HFC over next 15-20 years at least.

China

Compared to this China has planned more aggresive cuts in HFC production

Countries like China will have to cap their HFC use by 2024, while even poorer countries like India get until 2028

According to what I read in a report which is behind a paywall, China would cut HGC production in 2023 by 10% & then by 10% in 2024. China would reach 50% production capacity cuts by 2042, a much steeper production cut than India. This would have 2 effects. Incremental production & demand could shift to India (for both Ref Gases & FP).

Importantly Countries like China will have to cap their HFC use by 2024, while even poorer countries like India get until 2028. (From what I read in the report China is actually capping production to 2022 levels & reducing in 2023 & 2024). Meaning, Indian players like SRF, GFL can put up more capacities over next 5 years as they create & capture the market.

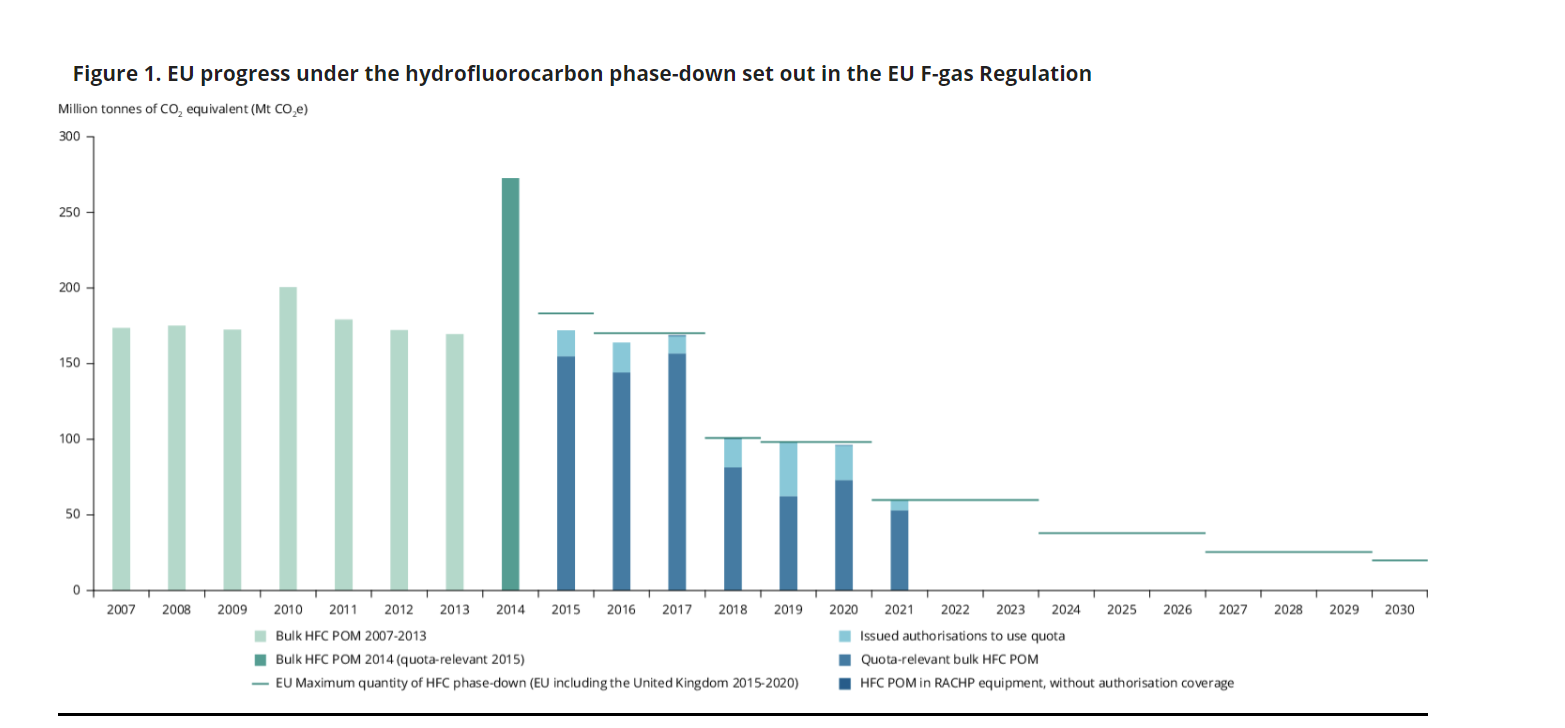

Developed world

While europe ratified & implemented Kigali amendment immediately (2016) so has already reduced capacities by > 50% for HFCs,

USA only ratified the Kigali amendment in 2022:

This means, that USA will have to ramp down production aggressively now onwards.

These revised targets have used a similar methodology to those behind plans to introduce a 10 per cent phasedown of HFCs up to 2023.

The US Government has committed via its American Innovation and Manufacturing (AIM) Act to reduce the production and consumption of HFCs by 85 per cent of baseline levels from 2036.

US EPA proposes schedule for major HFC reduction plan – Refrigeration and Air Conditioning.

Note that a similar phasedown also happened for generation 2 Ref gases (HCFC: Hydro Chloro Fluoro Carbons). The demand for HFC is not going anywhere because HFO (generation 4 ref gases) is not at the level of efficiency where it can replace HFCs.

The refrigerant-side overall heat transfer coefficient of HFO-1234yf is 18–21% lower than that of HFC-134a in the mini-channel heat exchanger in the same operating conditions

R 1234YF ah HFO has price of around 10,000 / 5 KG

Vs that, check R32

Just check the price difference. It’ll take a while before HFO can substitute for HFC due to both efficiency & cost being much lower & higher respectively.

One open question

Since Kigali amendment talks about cutting down both production & consumption , what is not clear to me is whether it ok to produce it for non-emissive captive consumption like forward integration into FP like GFL does & SRF might do, or is that also to be phased out (what happens to FP production then? Would it have to be done via some other non-Ref-gas route?)

Conclusion

- The demand supply scenario for Ref gas looks quite interesting. I can understand now why donald sir said this in his post:

- In the FP space, each molecule might follow its own demand supply scenario (like we have discussed earlier, PVDF might see excess supply like others like FKM might see excess demand) but fully integrated players will do better than ones who convert Ref Gas into FP since it would incrementally become difficult to produce Ref Gases specially stand alone.

Disclaimer: Same as before.

| Subscribe To Our Free Newsletter |