Here is my take on the results:

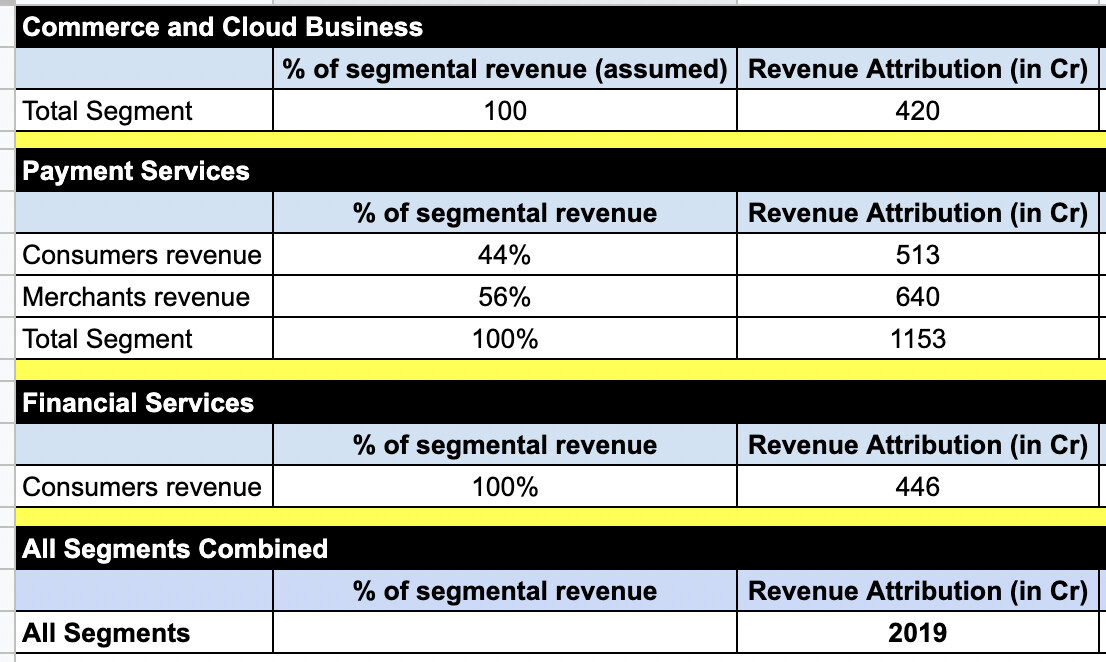

Payment Services Revenue

- Revenue Growth

This segment has been flat. About 1% growth QoQ and 21% YoY (34% adjusting for UPI incentive) - Expenses

Reduction of 1% QoQ and 6% YoY driven by festive season sales (though the report incorrectly says Q2 FY2023) - My take

Disappointed with this segment. Flattish revenue (QoQ or even compared to last few quarters). Expenses have gone down, marginally, which is a positive, but I am not sure if this is an aberration or the new normal. Further, the guidance is that the payment processing margin will reduce from 7-9 bps to 5-7 bps

Financial Services & Others

- Revenue Growth

Steep revenue increase. 250% YoY and 27% QoQ - Expenses

Check overall expenses - My take

Impressive performance in this segment. The company gets 2.5-3.5% of loan value at disbursement and 0.5-1.5% post-portfolio closure (which should come in in about a year or so).

Commerce and Cloud

- Revenue Growth

Flattish revenue. 24% YoY - Expenses

Check overall expenses - My take

Indifferent

Overall Expenses

- Indirect expenses have decreased from 58% of revenue (Dec-21) to 51% of revenue (Dec-22). Very impressive.

- ESOPs have gone up by 150%. This is very disappointing, especially when the company’s stock price is struggling. I understand that not 100% of ESOPs will vest, but the company should provide visibility on ESOP cost in the future, and the method of allocation.

Final Note

1. I think Paytm is becoming more of a lending company as opposed to a Payment Company

2. Strong performance in lending. Not so much in payments and commerce/cloud business

3. Operational profitability is good. But the management has to provide visibility on ESOP allocation, and not abuse this instrument.

Disc:

For educational purposes.

Ex-Paytm employee (left org in 2019).

Invested

| Subscribe To Our Free Newsletter |