I’ve been invested in Intellect since late 2020, and averaged up in the process. Sadly, have lost a good chunk of my gains during 2022. However, here’s why I remain invested in this scrip:

- India hasn’t produced many product companies. It is indeed commendable that Intellect is able to compete head on with Temenos, admittedly a big player in the banking software space

- It is difficult to compare revenues on a quarterly or even a yearly basis for a company undergoing changes in revenue monetisation, due to a shift away from term licenses to perpetual licenses and SaaS revenue

- However, new bookings and pipeline are the holy grail for any tech company. New wins will materialize into revenue at some point in the future, in a term license or subscription format

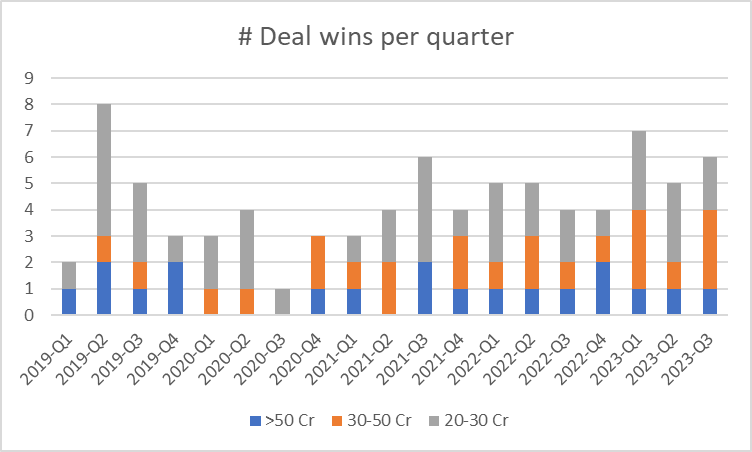

- Here’s how Intellect has been performing on its new wins on a volume basis for its destiny deals (i.e. deals with >20 Cr contract value

- As we can see, there’s been a steady increase in new wins, in 9mFY23 vs FY22, particularly in the 30 Cr+ category, which is a good leading indicator of future revenue

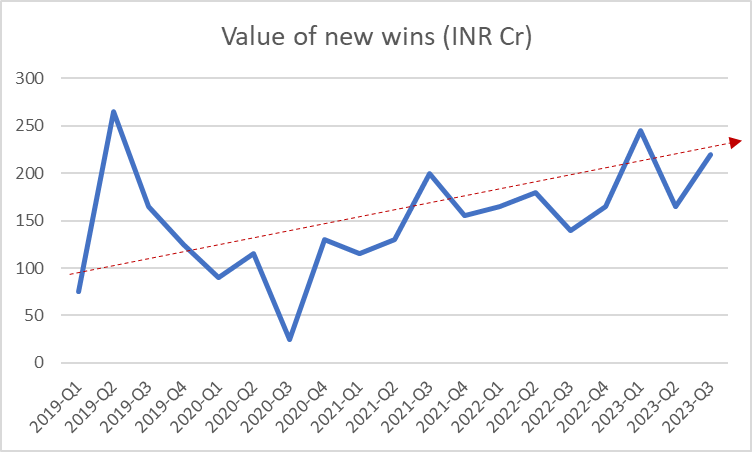

- To see this in value terms, I’ve taken a weighted average of volumetric wins by the respective deal size category (for e.g., I’ve taken 40 Cr as the avg. for 30-50 Cr bucket. This gives us an interesting trend

- Again, there’s been a good momentum in growth in 9mFY23, which continues from the historic growth trajectory and is unfortunately masked in the recognised revenue trend. They could have gotten lucky with INR depreciation, but this shouldn’t be a big factor

- If we look at their pipeline, this has remained stagnant at 500-600 Mn$ during 2019-21. It rose to 600-700 Mn$ levels in 2022, and is now at 855 Mn$. Obviously, the conversion rate may not be as high as in 2021 as Management indicated that sales cycle has elongated and customers have become more stringent in their selection process. However, Intellect seems to have expanded its pipeline considerably in 9mFY23 vs previous years, which could augur well for the future.

- Lastly, there’s the whole discussion on margins. I think the Management had been unnecessarily optimistic in guiding for 25%+ EBITDA margins, when they knew they had to invest into product development. “Quarter se Quarter tak” analyst scrutiny doesn’t help with giving the management some time to invest into product gestation, but they should have been firm and upfront about it

- So where does this leave us? I think we’re probably near the bottom of the earnings cycle, especially given the P&L shows full impact of tax. Conservatively, this is trading at a ~22x PE multiple on a runrate basis (adjusted for cash), and has the potential to grow revenue at 15%+ CAGR, and 18-20% EBITDA margins. This is not a particularly bad deal for a business with a healthy cash conversion cycle, limited pricing threat, and good RoCE

- It’s a big deal to build cloud-native microservices products. Strategically, this gives the product company an advantage to cross-sell over the term of the contract, thereby increasing the customer lifetime value. New wins in Europe and America / Canada validate their product proposition

- One risk I see is that the number of new destiny deals added to their pipeline has remained stagnant in 2023 vs 2022, which along with an increase in pipeline suggests that their deal value per deal is decreasing, which requires additional S&M investments. This would be a key monitorable to track – if they can increase the number of destiny deals in the funnel due to US / Europe expansion; else, they may see tepid growth ahead

Disc: Invested, biased

| Subscribe To Our Free Newsletter |