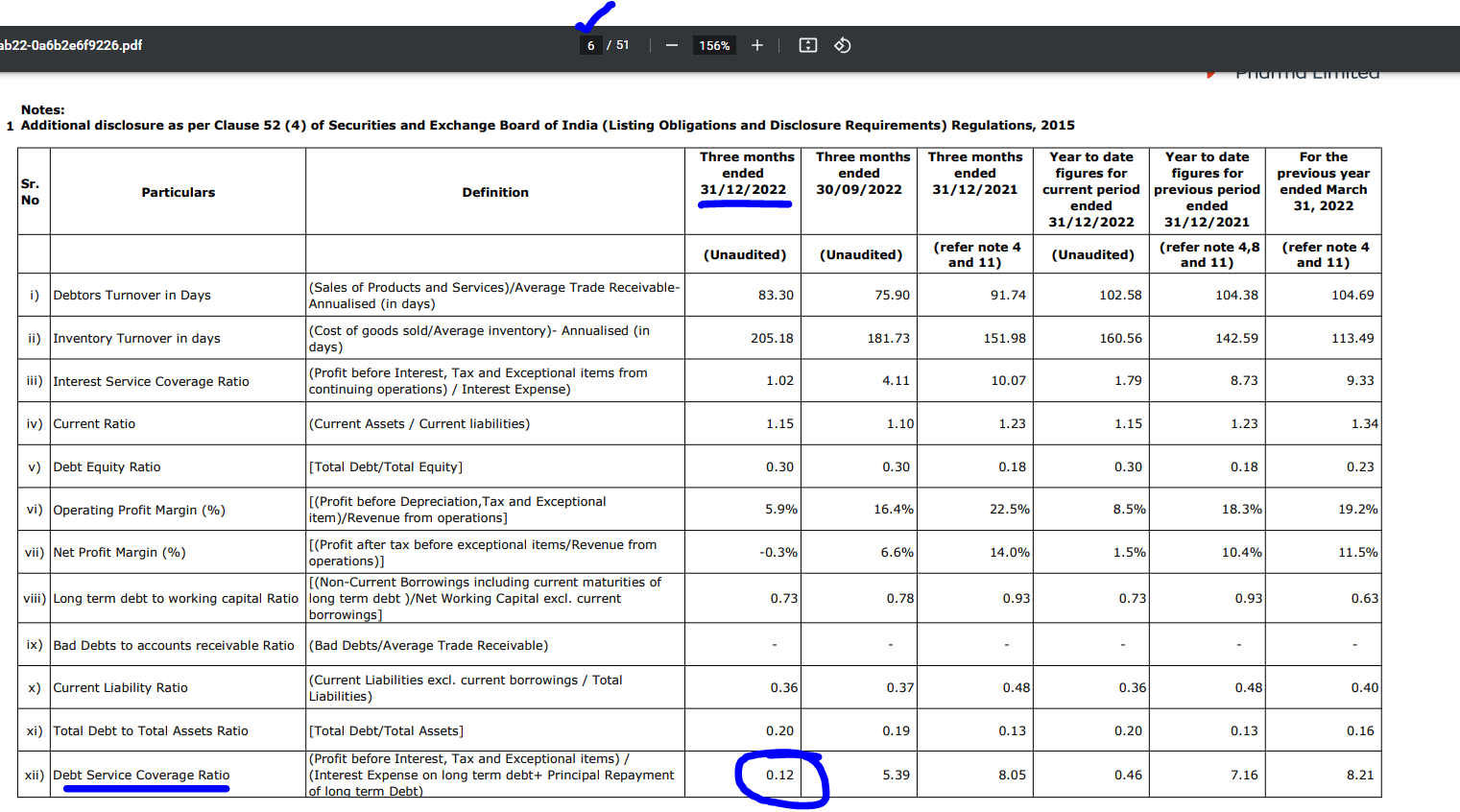

Results out for Q3 (Link).

Basis management’s view in previous conference call, H2 was expected to be better than H1. However, Q3 of FY23 is worse than Q3 of FY22. All the costs increased more than the revenue increase in % terms.

Brief synopsis:

| Dec-22 | Dec-21 | % Change | |

|---|---|---|---|

| Rev. | 1716 | 1539 | 11.5% |

| Mat. Exp. | 626 | 547 | 14.4% |

| Emp. | 492 | 396 | 24.2% |

| Other | 511 | 370 | 38.1% |

| Fin. | 95 | 50 | 90.0% |

| D & A | 164.4 | 147 | 11.8% |

| Oth. Income | 82.5 | 160.5 | -48.6% |

| PBT | -89.9 | 189.5 | -147.4% |

| EBITDA | 87 | 226 | -61.5% |

| GPM | 63.5% | 64.5% | |

| OPM | 5.1% | 14.7% |

Confirmation from the Q3 results:

However, chairperson expects investor to believe in the below highlighted reasoning:

| Subscribe To Our Free Newsletter |