Hi All,

I am a new member of the VP. For the past month or so, I have been in the read-only mode of a few fantastic posts in this community. I am truly grateful to Ishmohit that I stumbled upon this forum thanks to his SOIC course.

This is my first post/question on this forum. I was analyzing Apcotex Industries and I got really intrigued by the strong numbers it was posting.

High ROCE%, good ROE% decent NPM %, reinvestment rate of a whopping 92% over the last 10 years, ROIIC of 26%, and average ROIC of 16%. The management consists of members with strong credentials. I am considering investing in this company as it is at an attractive price point right now. I am planning to wait a bit for the base to form in terms of the stock price fall currently.

However, while going through the Annual report of FY’22, I also found a few anti-thesis pointers. I will list them here – I tried searching if anyone had asked this question and I couldn’t find it. My apologies if this is a repeat question for you all. Can anyone help me with this?

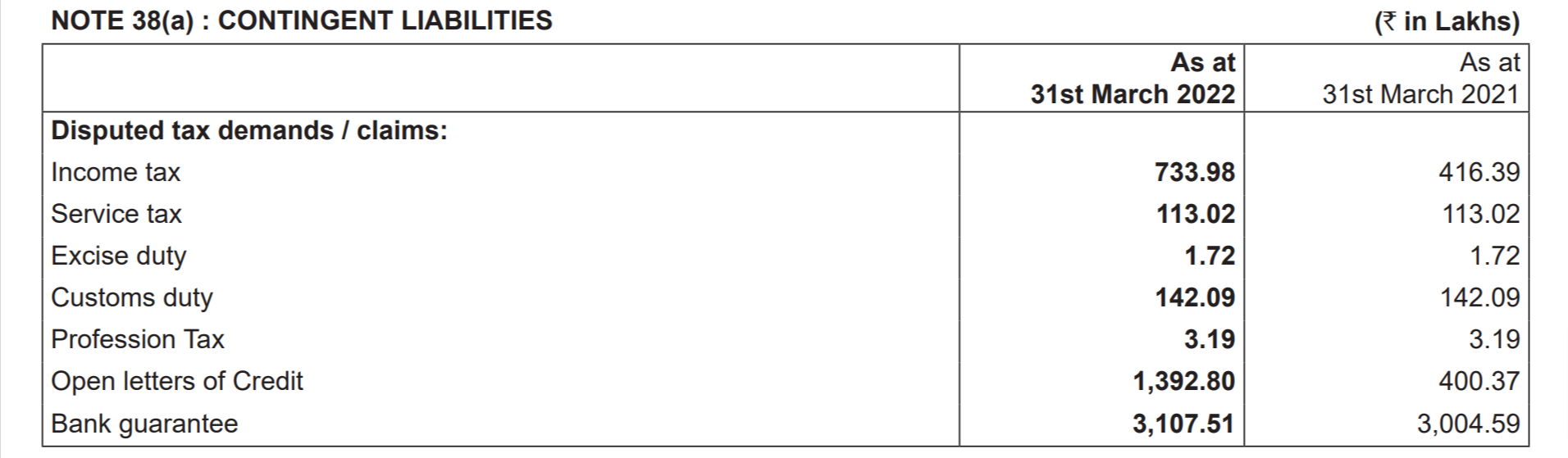

- The contingent liabilities have been consistently high for the past 6-7 years when looked at as a % of Net worth. Is anyone else concerned about this or has an opinion about this? Bank guarantees and Open letters of Credit constitute ~80% of the FY’22 contingent liability of 54 Cr. Is this normal in this line of business? Are the peers too susceptible to these costs?

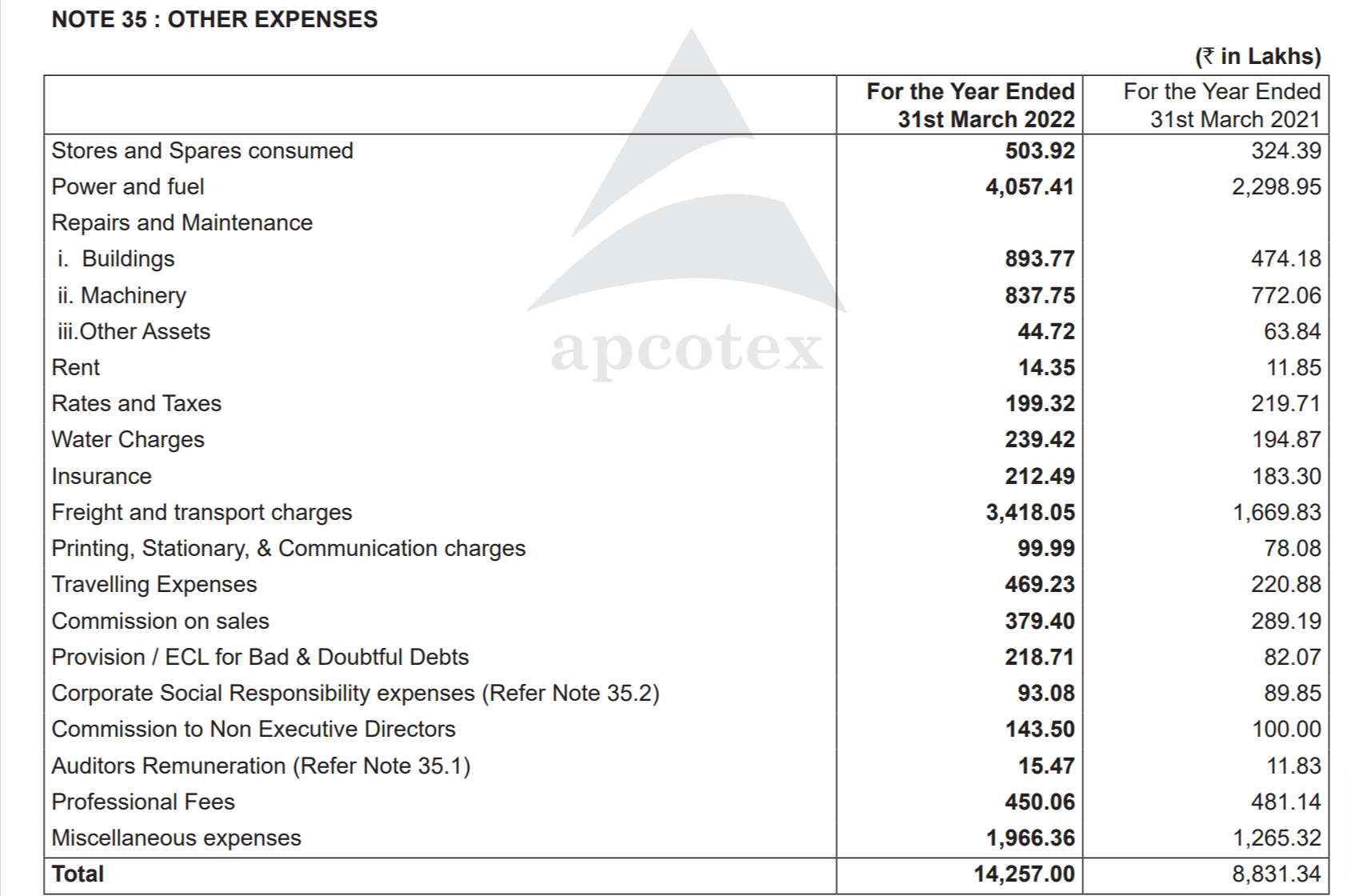

- **Increase in Other Expenses YoY **: There has been a 54Cr increase in the Other expenses from 88 Cr in FY 21 to 142 Cr in FY’22. Doing a Pareto of the same suggests that the majority of it comes from increasing in Power and fuel by 18 Cr (is it due to a predominantly increase in Crude oil?), an 18 Cr increase in Freight and transport charges (is it due to supply chain constraints) and a 7 Cr increase in Miscellaneous expenses (I am unable to find a reason for this increase). Any perspective on this?

Thanks in advance for the help!

| Subscribe To Our Free Newsletter |