Here is my take on Q3 results:

1. Food delivery

- Growth: Decent. QOQ dergowth, because December is a historically week quarter historically due to travel, vacations etc.

- Margin: I have no clue what adjusted EBITDA means, so I can’t comment

2. Hyperpure

- Growth: Strong. QOQ increase, 100%+ yoy increase.

- Margin: I have no clue what adjusted EBITDA means, so I can’t comment

3. Quick commerce

- Growth: Disappointed. 50 day revenue was 142 Cr last quarter, and this quarter they did 301 Cr. So about 20% growth after adjustment (pun intended)

- Margin: I have no clue what adjusted EBITDA means, so I can’t comment

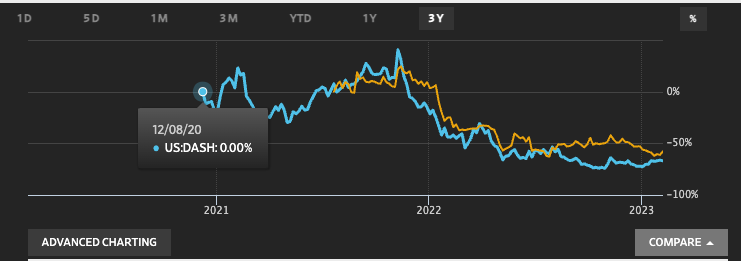

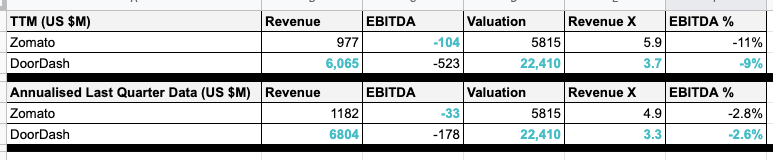

Given the limited information from Zomato’s balance sheet, I felt compelled to another company door dash, which is in a similar business (minus Hyperpure). The stock price seem directionally correlated (extent of direction varies)

In comparison to DD, Zomato is over-value in every respect

A few other things to consider:

- Zomato has a higher growth rate, but DD is not too far behind. Growth rates are difficult to decipher due to acquisitions, lock-down impact etc

- Unit economics are much better for DD

In my opinion, I think there is still froth in valuations. My view is closer to Aswath Damodaran, that 35-40 is the deep-value price (assuming 50% premium basis comparison with DD)

| Subscribe To Our Free Newsletter |