Post Q3 earnings season, want to share my current portfolio, and plan for each basket going forward:

Financials ( 40% )

| Company | Allocation |

|---|---|

| UGROCAP | 22.69% |

| SOUTHBANK | 3.14% |

| SPANDANA* | 2.36% |

| SHRIRAMFIN | 2.27% |

| FUSION | 2.22% |

| CSBBANK | 2.19% |

| EQUITASBNK | 2.13% |

| SBIN | 1.97% |

| FEDERALBNK | 1.76% |

-

My exit for CSB is around 320 per share, 2x FY23E book value of around 160.

-

Federal Bank and SBIN are proxies for cash. Federal Bank is currently at 1.3x FY23 book, my plan for an exit is around 1.7x book.

-

Fusion and Spandana are very interesting to me right now. Fusion is currently at 1.9x FY23 book and is a 4.5% RoA business. Spandana has gone through a very large reshuffle and a lot of drama over the last 6 months. Now it’s available close to FY23 book value. Exit price for both depends on how long good times continue for the MFI industry, and whether they can partially bridge the valuation gap to CreditAccess.

Metals ( 10% )

| Company | Allocation |

|---|---|

| IMFA | 4.27% |

| SANDUMA | 3.48% |

| SHYAMMETL | 1.45% |

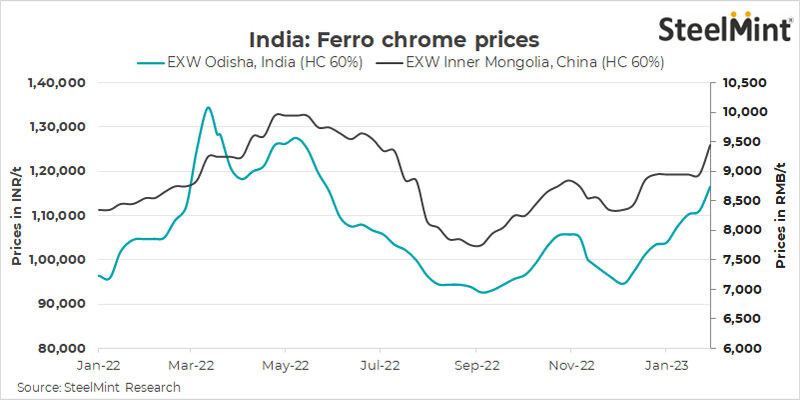

- In this pack, higher allocations to IMFA have so far paid off. I am up around 25% on my average, and the ferro-chrome index signals that the next quarter should be a good showing. Looking to exit at around 350-370.

-

Sandur’s EC has come through for a huge expansion, and results should start to look better from here on out. The stock story is a great read on VP.

-

Shyam Metallics was once the case study used in conjunction with Godawari Power, as listing valuations for Shyam were very expensive compared to GPIL. Since then, it has corrected tremendously, and is now around book value. With a few large expansion works finishing 8 months early, valuations in Shyam are now attractive. I will be increasing my allocation to around 4% over the next week.

- GPIL posted a good set of numbers, but they’re currently shutting down their sponge iron plant and completing some upgrades. My hope is that the share price will fall back to around 300-330.

Healthcare (10%)

| Company | Allocation |

|---|---|

| KRSNAA | 7.55% |

| CAPLIPOINT | 2.86% |

- Have done a lot of work on Caplin Point in the last few months – they have executed their scale up in the US very well. Volume growth in Caplin Steriles has been exceptionally strong, at a CAGR of 34% over 3 years, and revenue growth is even higher as newer molecules have far higher realisations than older molecules like Ketorolac. Steriles currently has losses of 25 Cr. on the books which will cause a free swing in PAT through Q4 and FY24. Aside from this, Caplin has multiple triggers over FY24, and is trading at a discount to historic valuations. This is the third time I’ve owned Caplin Point since 2020.

Chemicals (15%)

| Company | Allocation |

|---|---|

| FLUOROCHEM | 4.23% |

| SHARDACROP | 4.18% |

| ULTRAMAR | 2.73% |

| VALIANTORG | 1.79% |

| PUNJABCHEM | 1.76% |

-

At the behest of VP collaborators, studied GFL during the last month and I understand why the story is this exciting. New age fluoropolymers have much higher realisations than legacy products, and supply scenario in Chinese fluoropolymer producers suggests a favourable cycle for refridgerants. Overall, it is a very complex story with many moving parts. For such complicated companies, I need multiple quarters to better understand everything, and will scale my position accordingly.

-

Valiant Organics is now a turnaround story, and margins should recover as their chlorination vertical sales normalise, and the dye industry recovers.

-

I would like to scale Punjab Chemicals to 5-6% of my portfolio over time. Expecting Q4 to be flat, with multiple triggers in the future as they move to more complex chemistries, and scale higher realisation molecules. The thesis is an eventual improvement to 18% margins and beyond, coupled with 20% sales growth.

Components (5%)

| Company | Allocation |

|---|---|

| SBCL | 4.56% |

| XPROINDIA | 0.78% |

- I think there will be many opportunities to scale Xpro India to around 5% of my portfolio over the next six months. The next 3-4 quarters should be flat on PBT from the Biax division, and the Coex division is seeing a slight decline in revenue. However, they did not pay any tax in the last 3 quarters. As they will now be paying tax, the swing in the PAT will make earnings look weak until the Biax capex comes onstream. I think it is currently at a one year forward PE of 25, and should hopefully correct.

Other Cyclicals ( 10%)

| Company | Allocation |

|---|---|

| KRITI | 3.12% |

| GLOBUSSPR | 3.02% |

| AVANTIFEED | 2.42% |

| GEEKAYWIRE | 1.07% |

- Kriti Industries has seen incredible volume growth in Q3. The agri-pipes sector has seen muted numbers since covid due to the pandemic, and subsequent high price of PVC. This is now being resolved, and I expect blockbuster numbers for Kriti in Q4 and Q1 as the demand carries over into their seasonally strongest quarters.

- Planning to add Coastal Corp after Q3 results.

Current cash position is 8%. Inviting comments. ![]()

| Subscribe To Our Free Newsletter |