Unfortunately, there is no post mentioning the business dynamics so would like to share my limited knowledge on APSEZ and ports business sector fundamentals. I have power/infrastructure project finance background and had done a feasibility study to set up a green field port project.

Adani Ports Business Summary:

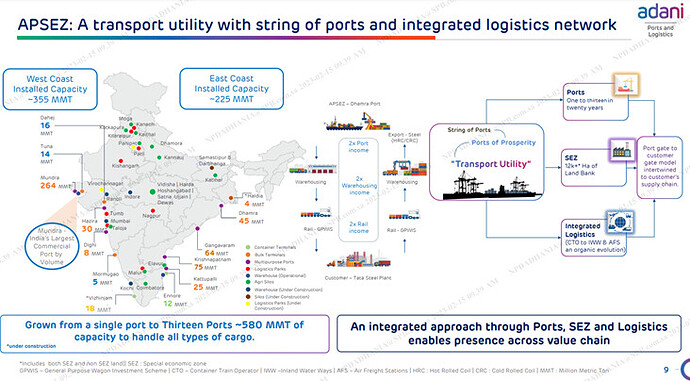

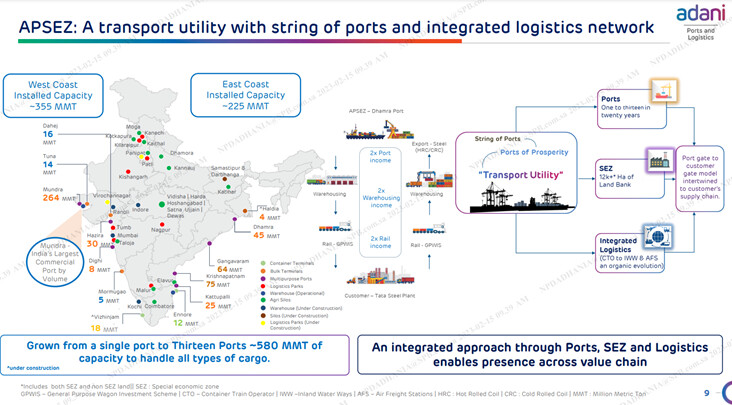

It is the largest commercial port operator in India with 25% share of port cargo movement in India. The company has evolved from a single port dealing in a single commodity to an integrated logistics platform. The company has a pan-India presence in ten locations (nine are operational) with the flagship Mundra port, India’s largest commercial port, in the Gulf of Kutch. It has a large land bank of 8,481 hectares of contiguous land at Mundra.

- Total ~70% of APSEZ’s revenues is contributed by its port operations. Rest

is led by harbour (11%), logistics (7%) and others. - In FY22, container, bulk, liquid mix were at 36%, 55%, 9%, respectively

Further financial and operating parameters can be found at screener.in so not wasting time on that.

Port & ICDs sector:

Construction of ports is quite challenging as the new age large container ships require deep channel depth just adjacent to land plateau. There would be very few sites where this is naturally formed. Gautam Adani was able to identify this opportunity at Mundra where no one had an idea and he jumped into port business with no prior experience!

Building a port where such natural occurrences are not available can lead to huge capex depending on site conditions. So yes it’s not that ports can be constructed anywhere. Also in India constructing ports itself has other challenges like environment clearances, fishermen agitations, PILs, etc.

Also, just building the port is not enough. The heart of ports is its connectivity to hinterland, inland container depots (ICDs), warehousing, etc. It is of prime importance to shipping liners that there is quick turn around of movement of cargoes as they have many ports to call. They will pay a premium for such facilities. Many ports in India are govt operated and there may be inefficiencies in them, leading to better business opportunities for pvt players. Building roads, train tracks, etc. itself is a humongous task with getting related approvals, etc. with extra capex costs.

Adani has and in future may keep acquiring key ports at strategic locations. This can create a monopoly business with pricing power. There are many future key trigger points like DFC connectivity to Mundra, acquisition of Concor, etc. It will take too much time and effort to actually understand the growth factors with so many acquisitions and future growth triggers (make in india, pli, china +1, new logistics policy, etc.)

My current take on the business and situation:

APSEZ was in my watchlist since last 3-4 yrs but had anticipated that one day there would be sell off in group companies due to extremely high valuations and it would have a spill over effect on Ports as well. Now with all this imbroglio I think it was apt time to enter Adani Ports.

Being from project finance background, I am more comfortable with high debt levels than average investor but will not get into that. Port business probably the best cash cow for Adani group but never understood the market irony of giving it less valuation than other businesses.

Even with this downturn in group companies, APSEZ has corrected less than others and as per recent news mutual funds are accumulating in last couple of days. Even Moody’s and others have maintained their grades while downgrading other group cos.

Disc: Not a registered analyst. Information for education and not recommendation. Invested and biased.

| Subscribe To Our Free Newsletter |