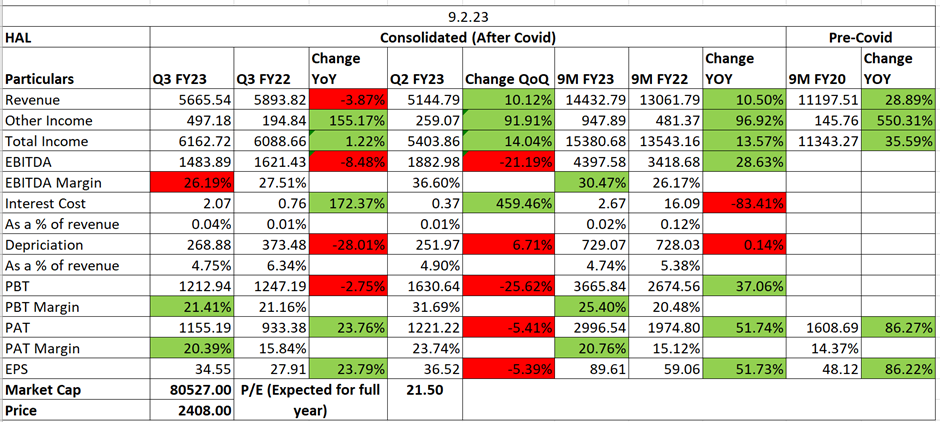

| – | EBITDA Margins reduced due to higher provisions. The guidance was of 25-26%. |

|---|---|

| – | PAT saw a growth due to tax refunds. |

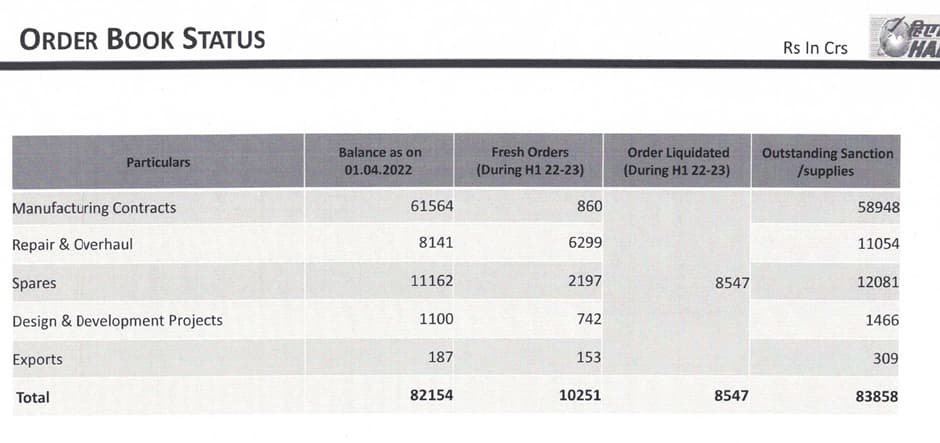

| – | Healthy order book position (84000 crore) led by large scale orders in manufacturing aircraft/helicopters (LCA, LCH, ALH). Implied order inflow was 16278 crore in 9M FY23. The order book is same as last quarter. |

| – | Continuous order inflows in maintenance, repair & overhaul. |

| – | Revenue was a little low due to muted execution in manufacturing contracts. |

| – | Gross margins improved due to lower RM cost. |

| – | In Q2 FY23, they said that they expect 8% revenue growth in this year. Revenue growth of 10.5% has already been achieved in 9MFY23. |

| Subscribe To Our Free Newsletter |