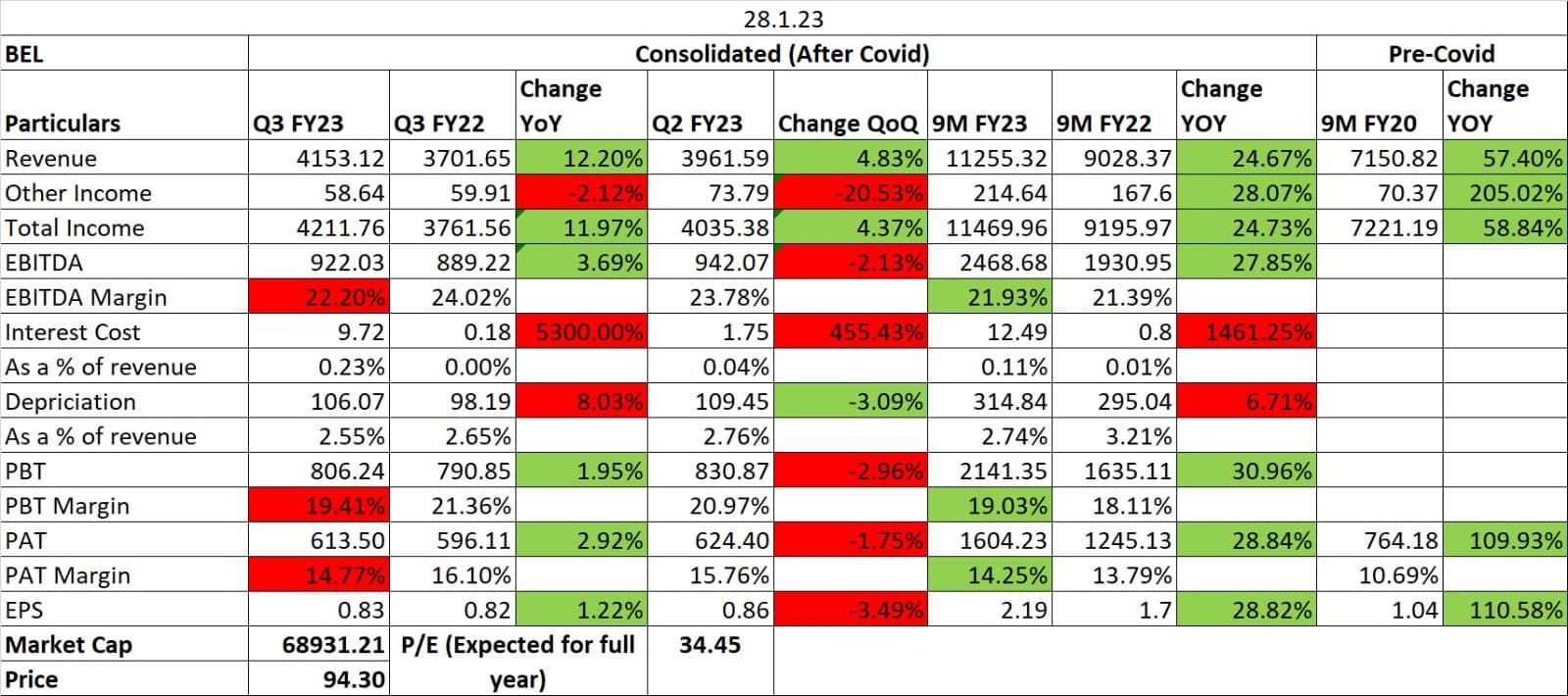

- Higher RM cost has impacted margins.

- Revenue increased due to better execution.

- Order book of 50116 crore as of Dec, 2022. Order inflows were 1452 crore in Q3 FY23 & 3736 crore in 9MFY23. Order pipeline is strong in FY23-24. Order book likely to expand in the coming quarters as a lot of them are in the pipeline. Order book accretion of 15500 crores is expected in Q4 FY23. Order expected are Himshakti programme of Rs33bn, Atulya medium-power radar of Rs20bn-30bn, Rs100bn expected from naval shipyards for radars and SONAR.

- Strategy to diversify into non-defence areas.

- Employee costs and other costs have increased.

- Revenue growth guided at 15% for FY23 and Gross Margins expected at similar levels of 42% for FY23.

- Capex of 6-8 billion expected in FY24.

- 15-20% growth in revenue expected in FY24.

- Investing in new facilities at Nagpur, Ibrahimpatnam, Anantapur, Hyderabad & Nimmaluru.

- Unwinding of receivables is expected in by March, 2023 end as government payments are coming in smoothly.

| Subscribe To Our Free Newsletter |