Just an update on my post written above more than 1.25 years ago.

The main question the current post tries to answer is whether anti-dumping duty (levied on imported toners) benefitted the company or not. IMHO, the answer is clearly yes:

1) Import Data

The anti-dumping order is in effect from August 2020.

If you observe the chart (SOURCE: Screener.in), you will observe that the Import Rate has steadily increased from 300-350 levels to 450+ levels. Admittedly, import data is noisy and also does not give accurate rates unless the HSN code is EXACT. However the general trend, shown in the red line, is unmissable

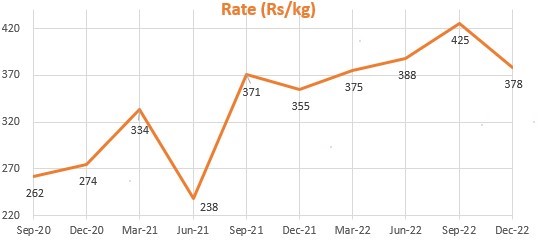

2) Improved Rates & Margins

The company had a capacity of 3600 MT which has increased to 4200 MT from September 2022. (SOURCE: Minutes of AGM held in August 2022). Using this we can calculate the Rate.

Again we don’t have utilization levels and hence the rates will be biased lower, but even here the trend is clearly visible. The company was getting Rs 262/kg in Sep-20 quarter and is now getting Rs 375/kg

Secondly the EBITDA margins have improved from 14% in Mar-20 to around 20% now

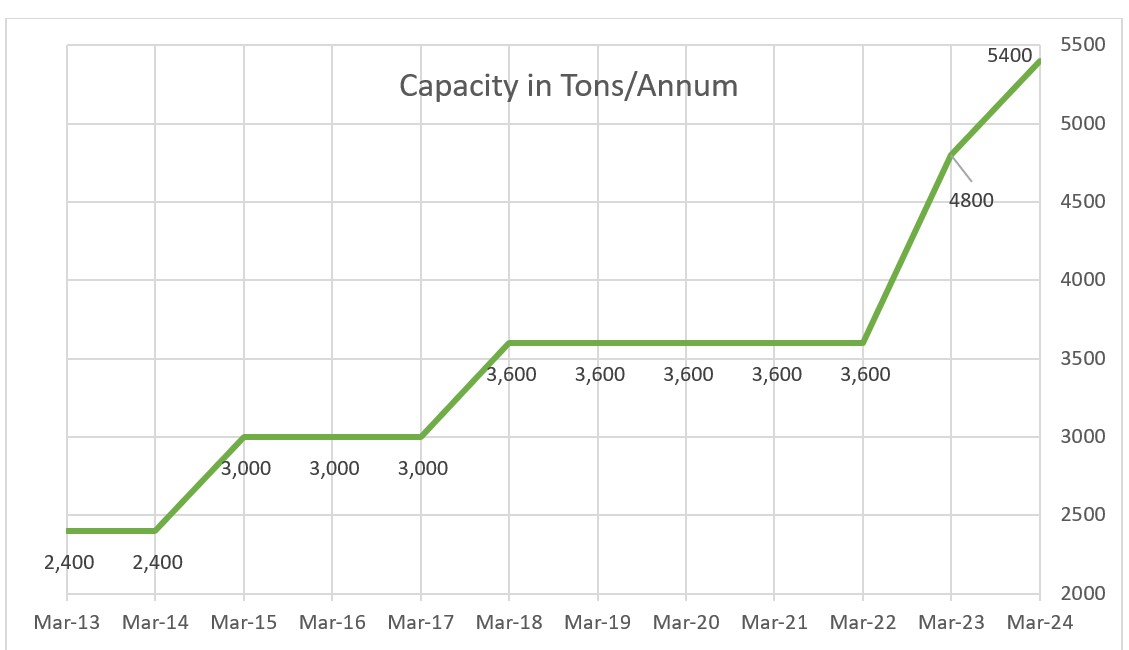

3) Higher Capex planned

The company has increased its capacity from 3600 Tons/annum to 4800 Tons/annum in January 2023 and has further announced its intention to increase to 5400 Tons/annum.

See Milestone section of their website. This clearly shows the confidence of the management in its business.

The current market cap is Rs 210 crores (Rs 195/share) and the company has Rs 85 crores cash (as per September 2022 Balance Sheet). At this price the market is effectively saying that after the elapsing of the Anti-Dumping Order (in August 2025), the company will not grow anymore, will not earn more than 12% Op EBIT margin and also will not have ROC>COC. These assumptions are EXTREMELY pessimistic and not consistent with past.

Even if you think in terms of the relative valuation, it is priced low. The business is being priced at Rs 125 crores (Rs 210 crores market cap- Rs 85 crores cash). If we assume capacity of 5400 tons/annum (in FY24) with an average rate of Rs 380/kg, it leads to revenue of Rs 205 crores. The average Op EBIT margin of the past 17 years is 16% and thus, after tax, we see a Net Profit of around Rs 25 crores. This yields a PE multiple of only 5 (Rs 125 crores/25 crores). One way to justify the cheap valuation is to assume that the margins will go back down to the levels it reached during the ‘dumping’ years of FY20/21 even in the long term. However, this assumption seems pessimistic (to me) and inconsistent with past data.

My views maybe biased as I hold the stock. Furthermore, my views are (and SHOULD BE!) subject to change in price and information.

| Subscribe To Our Free Newsletter |