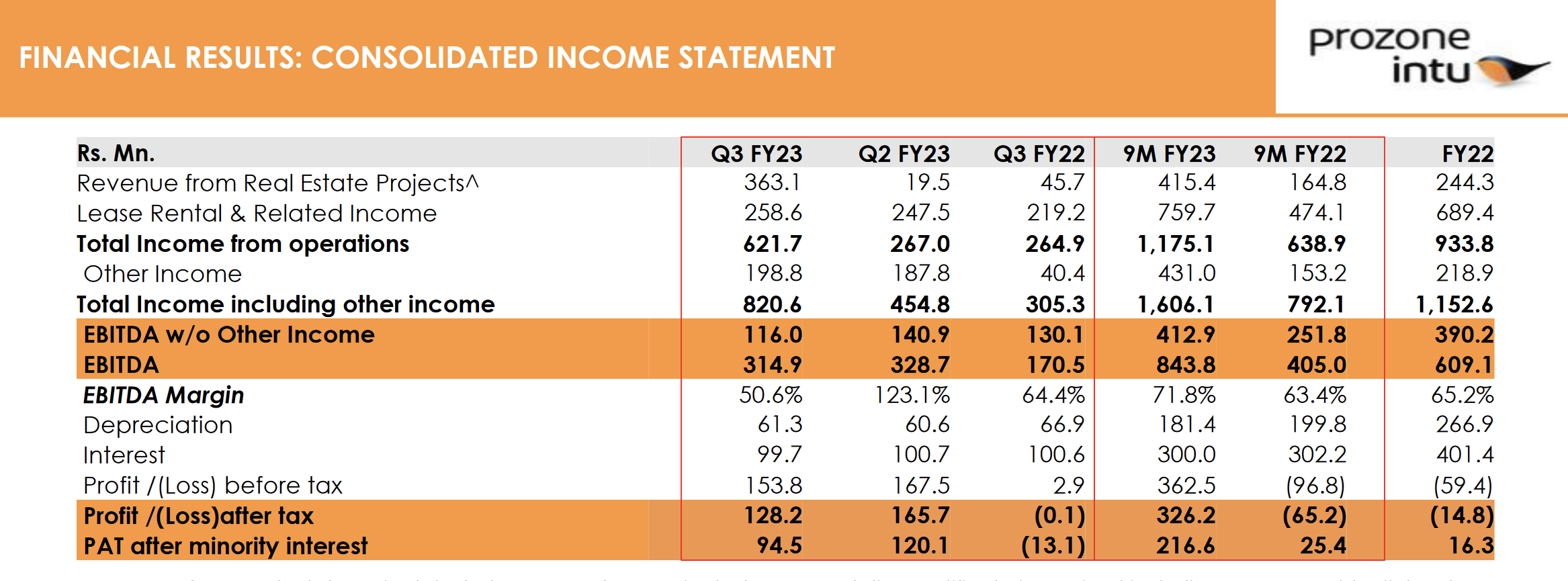

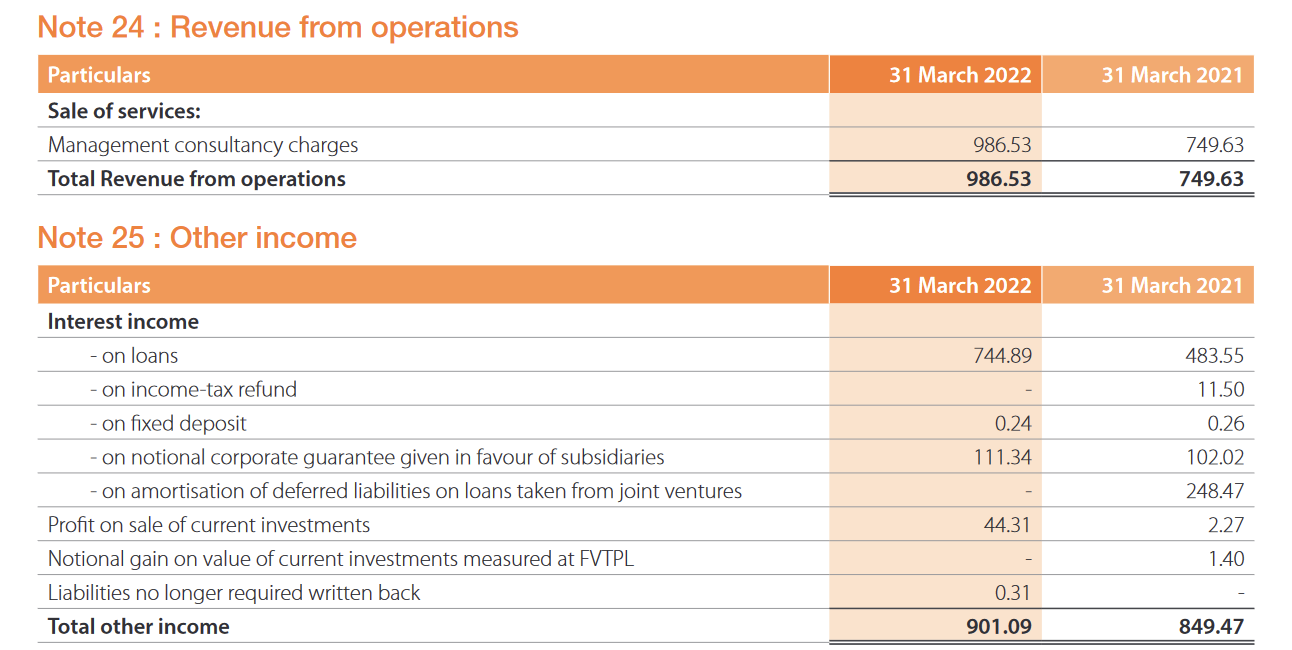

Once again other income is high and this time EBITDA has dropped. Dec 2022 quarter had a jump in expenses. Below is a shot from the Notes to financial statements in their annual report 2022 (link – https://www.bseindia.com/bseplus/AnnualReport/534675/77279534675.pdf | pdf page 128 of 221)

Here the other income includes

- Profit on sale of current investments

- Notional gain on value of current investments measured at FVTPL

I am not very clear on whether the other income is recurring but they have chosen to categorize it as other income and by that metric I presume that it will not be recurring. Also they have been able to sell some units in Nagpur and Coimbatore in the last couple quarters so I believe that is one aspect for the jump in other income.

I am not from an accounting background so I don’t know how to feel about the ‘Notional gain on FVTPL’ part here. It is not comforting as an investor but I suppose in a real estate business such as this, it is necessary to report.

Just a few points that I wish to note in this discussion

- Intu UK went bankrupt in 2020 thereby entering administration in the UK and KPMG took over to administer their properties. They have been selling off the UK malls to other real estate management businesses to recover money for their debtors as far as I know.

- Previously mentioned Chaturvedi family group trusts and some other assortment of trusts and companies are classified as the Indian promoters with 26.7% holding in the company down from 30.4% holding pre-covid.

- The investor presentation/ website etc. still uses the Intu UK logo / branding but I am not clear on the holding structure.

- Intu India sold off some portion of their shares in Prozone Intu so now they have dropped from holding 3.5% in Dec 2021 to 2.5% as of Sep 2022.

- Nailsfield limited holds 28.8% of the company. It is registered in Mauritius and was and probably still is a subsidiary of Intu Properties PLC (Source – https://bsmedia.business-standard.com/_media/bs/data/announcements/bse/22052018/F0B942C8_72F6_461B_A4F6_CCDDCA3718B2_182812.pdf )

PDF uploaded here in case the source goes down

F0B942C8_72F6_461B_A4F6_CCDDCA3718B2_182812.pdf (164.9 KB)

As an aside, this is probably why the business is using Intu branding and in case KPMG continues administering the business, they may sell off the holdings to recover the locked value. - Nailsfield Limited also held a stake in Provogue before that was delisted, (I presume due to the business failing) and as mentioned here the Chaturvedi family had a role in that business too.

- What I find interesting is that Nailsfield also had a holding in Pantaloons at one point (see – https://www.moneylife.in/article/pantaloon-promoters-to-infuse-rs-400-crore/6548.html). It might have been an Intu PLC strategy to get into retail businesses and have positions but not everything has gone all that well for them, as it appears.

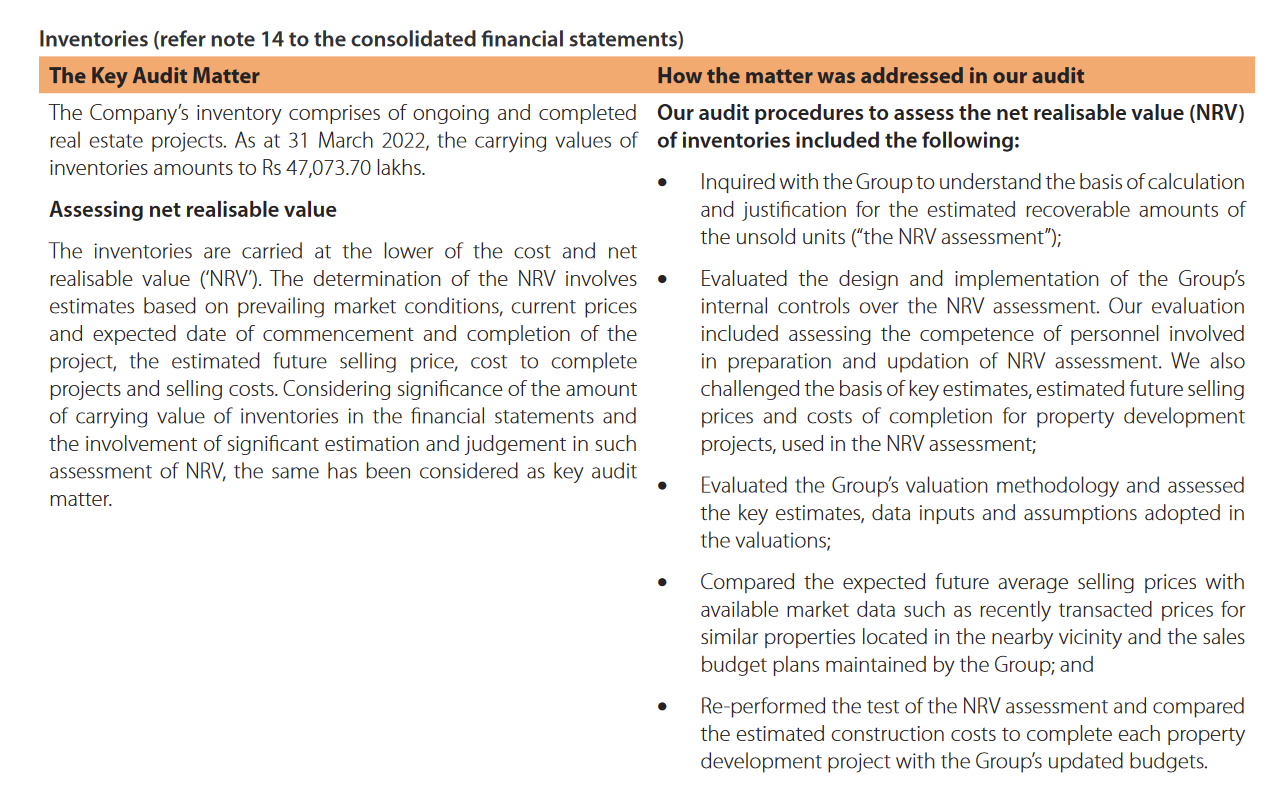

Disclosure here before continuing – The stock is an older holding in family PF, position size is small relative to PF. Considering increasing the position. No transactions in the last 30 days. Reason for holding and adding is that the business model is differentiated and current land bank plus unsold property etc. that is in their inventories gives them a book value above 30 Rs. while stock has been trading below that level (not without reason, as seen above). As for this consideration of inventories, it is prudent to read an audit note from the same AR 2022 (pdf page 153 of 221)

The previous page about revenue recognition is also worth going through before taking any investment decisions.

Below I am listing some points from the latest Investor Presentation (Q3FY23 IP – https://www.bseindia.com/xml-data/corpfiling/AttachLive/bea33a5e-69aa-45cf-9718-507851571907.pdf )

-

Two malls built – One in Aurangabad, which is 78% leased out and the other one in Coimbatore is 92% leased out so 80% – 85% of the leasing revenue is now being reflected in the income statements. I am assuming that any post-covid impact is minimal at this point. They are reporting increasing footfall.

-

Aurangabad Prozone Trade Center (PTC) is a commercial office space that is a part of the Aurangabad mall as far as I know. I couldn’t find details on the utilization of this office space. On the website it looks as if they are trying to lease it out.

-

Nagpur mall is under construction so that would be the next leg of leasing income growth. Debt has surged but there are reserves so it can be considered ‘net zero debt’ on paper.

-

170 / 540 residential units have been sold in Coimbatore as per latest IP so 69% of the space is yet to be sold. Construction is ongoing here, there are progress photos in the presentation.

-

272 / 336 residential units launched in Nagpur have bee sold so about 20% of the built space is to be sold out.

-

Collection of cash is not 100% for the sold residential units in both cases. This is normal with Real Estate projects of this nature and cash flow should reflect in the coming quarters. They seem to have enough expenses lined up for the cash anyway so debt may not go down soon.

-

43.5 acres residential with 5 acres commercial included is to be built in Indore. Many approvals have been received.

Overall, I feel that this is a risky pick. The presentation mentions that Jhunjhunwala holds some 2+%, Radhakishan Damani holds 0.9% etc. I usually am not a fan of these types of ‘selling the investment’ type of slides but many companies are doing it. There is a slim margin of safety here in my mind and further falls in price could increase that MoS. That said, it could all come crashing down but considering that they at least managed to hold on through the covid period I feel that they are at least resilient and the possible growth makes me think that this is worth a small allocation.

| Subscribe To Our Free Newsletter |