HBL has released their 1st Investor presentation on 13th Feb – sharing few key business updates below:

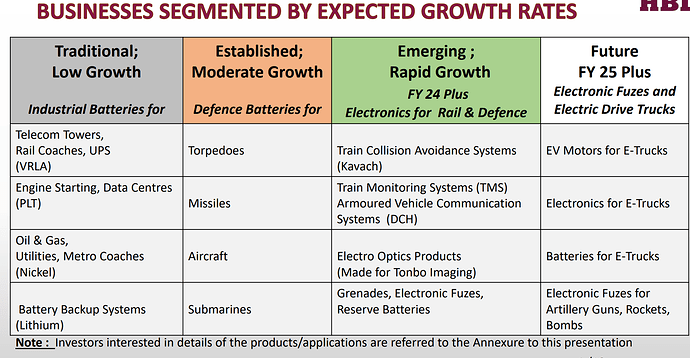

1. Slide 4 presents how managements segments business trajectory for various businesses based on their expected growth rates. Few things that stand out:

- PLT has been clubbed in Traditional low growth (despite massive tailwinds in data centres, and only 2 suppliers for PLT batteries)

- FY 24 onwards – Besides Kavach, also includes

- TMS,

- Electro optic products for Tonbo imaging (recent partnership announced by HBL) and

- Grenades/fuzes

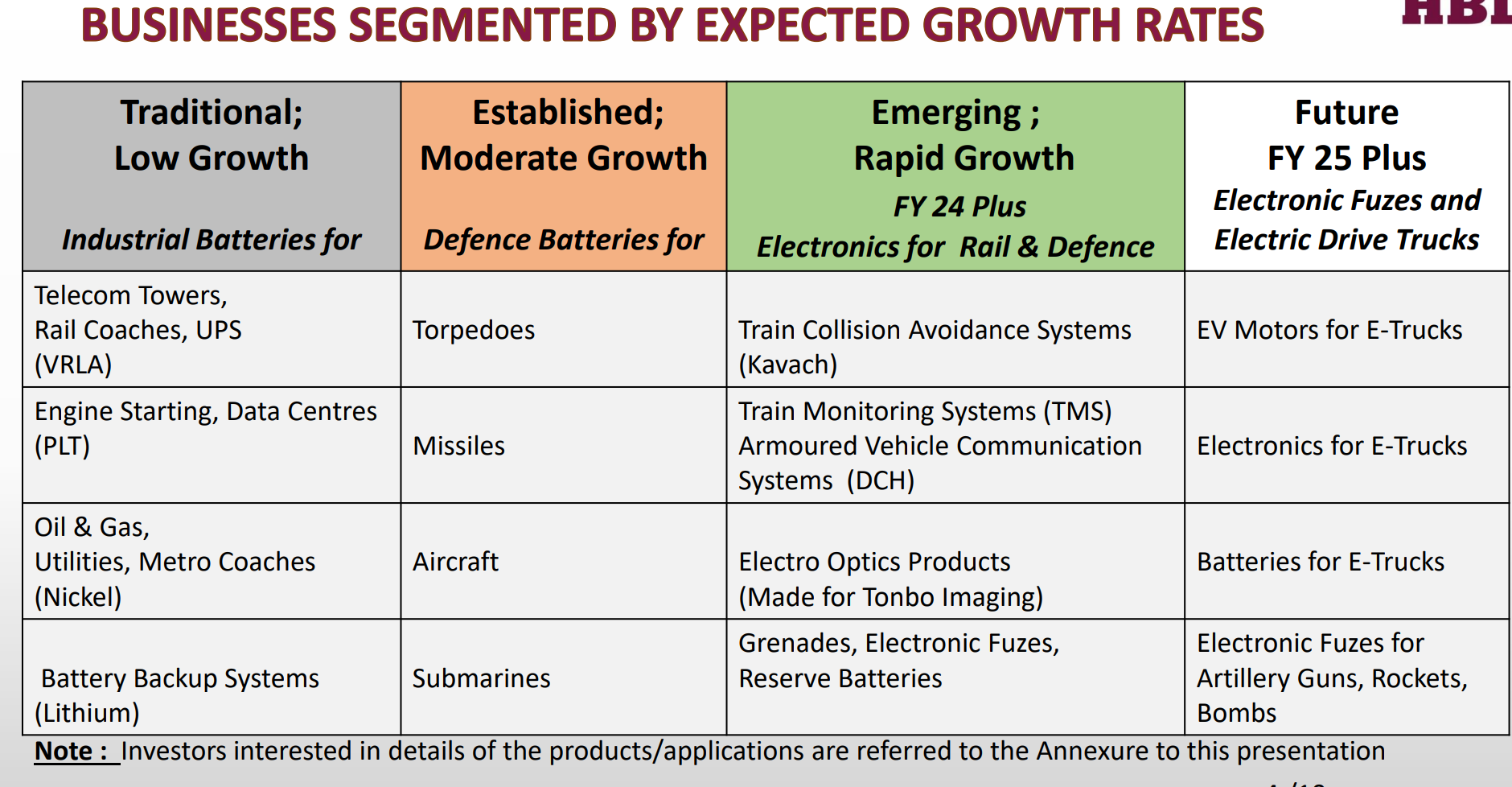

2. Slide 6 elucidates how the macro-economic environment has become supportive for HBL (unlike the previous 10 years) in all key business segments – railway electronics, defence, electric mobility

3. * On R&D costs –

- “Much of the cost of product development has been expensed. This is one reason why the profitability has been low in recent years, and why it will be higher in future.”

- “For the next few years, R&D expenditure would be lower and Working Capital would increase. The high capex of FY 24 will not be needed again in the next few years.”

4. On management aspiration – “HBL aspires to be a high value technology-based business, like the leading Mittelstand firms of Germany. We are on track to become one such company.”

Source: Wikipedia

5. TCAS/Kavach – Reiterates the limited competition in this space.

6. Torpedo batteries

One of the articles on battery chemicals mentions the advantages of aluminum silver oxide batteries. Extract below:

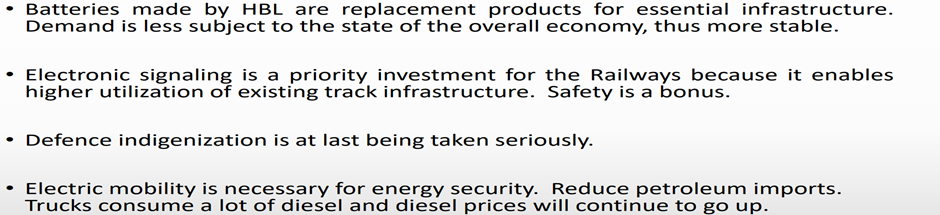

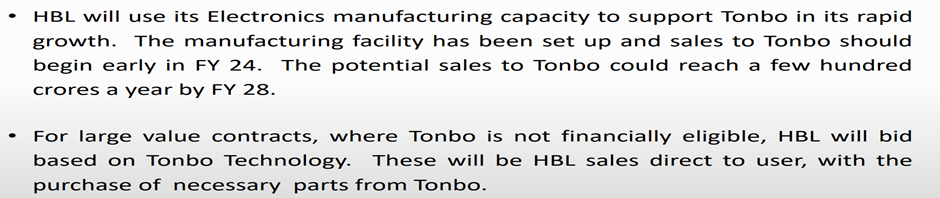

7. Tonbo tie up: Expected to start contributing to topline in FY 24 itself with potential to scale up to a few hundred crores by FY 28. The large value contracts, can probably be a higher margin opportunity for HBL.

8. Grenades with electronic fuzes – Approved by MHA and expected to begin by FY 24 and increase rapidly.

| Subscribe To Our Free Newsletter |