Seems that there is a decisive shift (after deliberation, diligence for 10+ years) in treatment approach towards fight against Tuberculosis/LatentTB. All the key global policy/decision makers are pushing for the new regime of treatment– preference of using Rifapentine (12/30 doses) as against current preferred treatment based on Rifampicin (90/120 Doses) formulation.

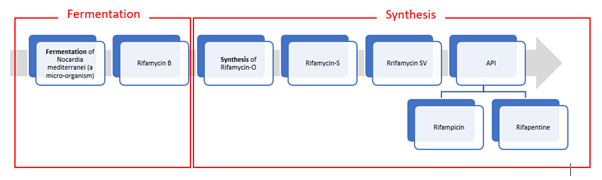

Worth exploring what are the implications of same on GTPL (manufactures Rifampicin API and its intermediate Rifa-S/O.)

Some facts to understand why the change in approach in the first place.

- As adopted in 2015, ending the TB epidemic by 2030 is among the health targets of the United Nations Sustainable Development Goals (SDGs).

- Milestones for 2020 was a 35% reduction in the number of TB deaths and a 20% reduction in the TB incidence rate.

- However, between 2015 and 2020 the cumulative reduction was 11% only as against the end TB Strategy milestone of 20%.

Two way constrain/challenge leading to sub-optimal performance on End-TB initiative:

-

Funding/Resource constrain (at implementation agencies level):

- US$ 13 billion are needed annually for TB prevention, diagnosis, treatment and care to achieve global targets agreed on at the UN high level-TB meeting. However, so far, global spend has been in the range of US$6B annual

- In fact, there was a decline in global spending on essential TB services from US$ 6.0 billion in 2019 to US$ 5.4 billion in 2021.

- For research and development, according to the Treatment Action Group, only US$ 0.9 billion were available in 2020 of the US$2 billion required per year to accelerate the development of new tools. At least an extra US$ 1.1 billion per year is needed to accelerate the development of new tools.

-

Treatment unaffordability/Discontinuation (at individual/household level):

- According to latest national TB patient cost survey data, globally, ~50% households reported treatment costs to be > 20% of their household income.

- Current regimen requires 90 days/120 days continued daily medication. In low per capita region and under developed countries, this longer regimen leads to discontinuation.

Considering the sheer scale, magnitude and context of Tuberclouses spread, fight has always been a calibrated global effort across different funding partners, implementation agencies, NGOs of global reach. Even in this case, global humanitarian agencies, implementation and monitoring agencies and eco-system members are working in tandem towards adoption and accelerated shift towards new medicine:

- US Centers for Disease Control and Prevention: Recommend 3HP (rifapentine) for treatment of LTBI in adults, persons with LTBI aged 2–17 years and persons with HIV infection. Link

- WHO: WHO encourages manufacturers to develop quality assured formulations of the game-changing drug rifapentine (Link).

- Big sponsors and funding partners striking volume guaranteed pricing deals with key drug manufacturers to address the affordability barrier:

- The Global Fund UNITAID and Sanofic (innovator) deal for 70% price reduction for volume committed agreement for Preftine (innovator drug). (Link)

- In August 2021, MedAccess, in partnership with CHAI and Unitaid executed a volume guarantee agreement with Macleods.

- Further In July 2022, they s negotiated a new agreement with Lupin to secure affordable prices for 1HP and 3HP. (link)

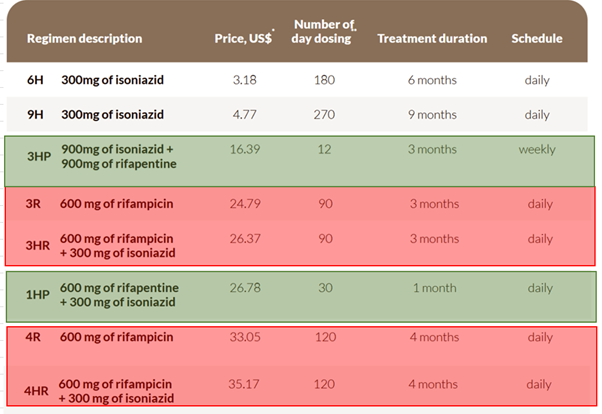

Prevailing treatment options:

P.S – On the above image, prices for 3HP and 1HP has come down significantly (in the range of $12-13) post Sanofi/Macleaod/Cipla deal with funding agencies.

Potential Impact to Gujarat Themis:

1: GTBL currently has approval for Rifampicin (API) and Rifa-S/ Rifa-O (intermediate). They are not manufacturing Rifapentine. Any decisive changes in treatment approach may impact Rifampicin volume offtake quickly.

2. Logically thinking, even GTBL can add capacity to manufacture Rifapentine since backward production value-chain is mostly identical. However there are few aspects to be thought through:

- Due approvals and Environment clearance may take its own bit of time. They already have sizable capex of ~200 Crs. underway for other formulation/R&D/AI.

- The API intake volume is going to drop substantially with the new medication norms – Rifampicin (600 mg * 90 days) to Rifapentine (900 mg*12 days) even if they start manufaturing Rifapentine.

- Part of the volume contraction may be offset by higher mg (900 mg) requirement and lower yield (~65% yield for Rifa-S to Rifapentine as against 85% yield for Rifa-S to Rifampicin). However, even with that net volume demand loss potential could be >80% for Rifa-S intermediate.

In general, both the big players Lupin (20 MT/year) and Mcleods has decent capacity of Rifapentine and have mostly been ahead of curve to the regulatory changes. Will be interesting to see how GTBL respond to evolving situation.

Disc: Invested

Tarun

| Subscribe To Our Free Newsletter |