24-02-2023 (analyst meet notes)

-

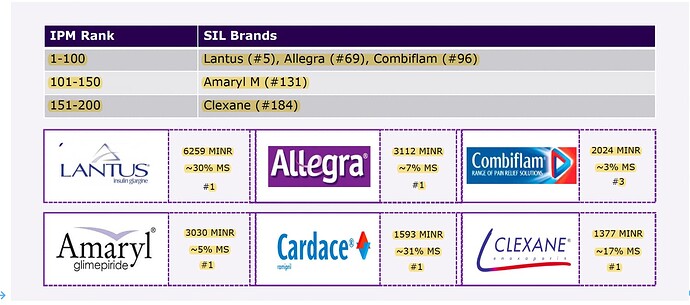

3 brands in top-100 of IPM and 5 in top-200. Targocid and Frisium are also leading in their categories. 70% sales from top 7 brands

-

Manufacturing facility in Goa along with 16 CMO, distributors: 3’000, pharmacies: 100’000

-

Like to like sales declined by 2% in Q4CY22 due to challenges in Targocid (faced supply chain issues)

-

Lantus: Draft notification will lead to 25% price erosion on the 3 SKUs. However, this price cut will be taken by the manufacturing arm (hence the parent) and the marketing arm (listed co) will not see any drop in margins

-

Lantus didn’t grow in CY22 because organization’s focus was on promoting Toujeo. Insulin glargine franchise (lantus + Toujeo) grew by 2%

-

NLEM portfolio: 15-16% which will go to 40% once Lantus comes under price control

-

Cardace and Frisium: Will see price reduction of ~14%

-

Clexane benefitted from covid demand and has shown sharp decline in CY22 (already under NLEM)

-

Growth drivers: Diabetes and consumer healthcare. Have reduced business units to 3 from 8 earlier. Transferred 200 MRs to the Diabetes division

-

Had 6.5 lakh prescription patients in 2020 which moved above 7 lakhs in 2021

-

D3 vitamin market size is 800 cr., growing at 3%. Sanofi’s market share is 5%

Disclosure: Not invested

| Subscribe To Our Free Newsletter |