His compensation last year – INR 10.7cr

His total investment in ITC – INR 11cr (at current valuation after doubling) – I think pretty much entirely through options over the years (by diluting shareholders) which I guarantee you he will keep selling.

He has been at ITC since 1986! – 37 years. (probably higher than the average age of a valuepickr participant)

Screener has insider trades since 2018 September – I have found 3 buys (amongst 100s of sells) by some employees/relatives buying insignificant qty of shares (two are of 100 shares by some relative and another is 2000 shares)

The purchaser of 2000 shares is this guy who runs a small part of the FMCG business

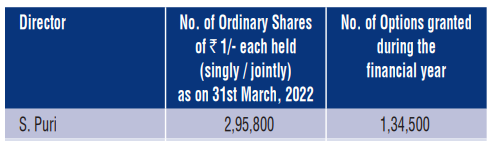

S Puri has only sold.

ITC effectively has no controlling shareholder, no parent, no promotor – no maa/baap.

There is no accountability – and the management doesn’t have enough skin in the game. They do not disclose how the bonus/performance element of compensation is determined.

Despite all the media/valuepickr/retail investor ferment about demerger – I will be very surprised if that happens – because the management has no incentive to do so – read empire building. They cannot justify paying high salaries otherwise.

“Yes we have discussed at board level blah blah blah blah”

Not that hotel demerger is going to create any significant value. Instead:

-

Demerge FMCG and Agri into one entity – aggressively grow, acquire, gain scale, increase availability then focus on margins.

-

Demerge Tobacco – maintain share, drive op lev, build RRP business (import tech from BAT and lobby govt to create policy), return 95% of cashflow to shareholders annually and lever up to 1-2x EBITDA and refinance with a big dividend or buyout a big shareholder (SUUTI maybe or buyout BAT’s stake in all non-tobacco assets)

-

Demerge Paper – stabilise margins and grow.

-

Maybe sell ITC Infotech – I don’t even know what this business does and I don’t think most shareholders do either (maybe ask on the concall ??? – doesn’t happen of course) and if you ask management they’ll do some word vomit about IT services etc.

Wouldn’t be surprised if the business is mostly internal to other ITC businesses. -

Maybe demerge hotels – create a pure-play luxury ITC hotel management company – sell more assets to a Brookfield/KKR fund (retain only flagship properties) and get into 10-20 year mgmt contracts.

A fairly asset-light business with long-term contracts (SaaS much?) and ownership of some flagship properties (already paid for) allow mgmt to effectively experiment and increase value prop (R&D) – these businesses are worth a lot folks.

That said all of that is wishful thinking because it won’t happen.

For one minute assume that my plan is a good one and it happens – tell me about the future of S Puri and where he sits and how he takes home 11cr a year (and growing)

Now if ITC is a large majority of S Puri’s net worth – suddenly he starts behaving like a responsible fiduciary rather than a hired hand.

I know my thread(s) may feel like a rant – but come on folks. We are here to discuss and be critical – not to defend the management. It is the management’s job to serve investors.

Sure price drives narrative (bhav bhagwan che) and re-rating has driven the performance. But tell me what has management done to drive re-rating?

Business performance was down, which has reverted to mean. The least the management could do is to run the businesses well.

Govt didn’t raise taxes (as much) – that helped sentiment and will help volumes.

And from a fairly poor sentiment (meme stock) to now – that’s basically sentiment mean reversion.

The one thing management has done is to stop hoarding cash (any more – there’s still a massive pile btw) and have a high payout policy and say they’re going to an asset-right strategy for hotels. (whatever that means and not that hotel is a value driver for this business – but surely investors pay attention to it so it is a sentiment driver)

And FWIW – I’ve had a 2x in ITC – but I don’t think I give credit to the management for that like they’ve been some wonderful stewards of capital.

P.S.

Why do companies like Alkyl Amines, Dmart, Berger Paints, TCS do con calls where the CEO shows up – promoters own > 70% of the company. Unless the promotor wants to do something – minority shareholders in theory have no say. Because they are good fiduciaries of minority shareholders’ capital.

| Subscribe To Our Free Newsletter |