Sure, but what’s highlighted in the picture is PAT Margin.

ITC FMCG PAT margin is currently like 4.5% (I would argue standalone economic margins would be lower)

6% EBIT Margin currently – assume no interest expense and a 25% tax gives you a 4.5% PAT margin.

They don’t have interest expense because the parent is funding with tobacco cashflow – so economic margins are lower because the growth is not self-funded (not so far anyway)

From your graphic,

In the 1992-2001 period – they grew sales at 22.5%

2.5x PAT margins and increased ROE from 30% to 54%

Assuming 7% inflation, ITC’s 18k crore (FMCG Revenue) is where HUL was in 1992-1993. HUL then did a 7% PAT Margin, 50% ROCE and 35% ROE.

I think he’ll be okay given he’s definitely getting a big raise this year.

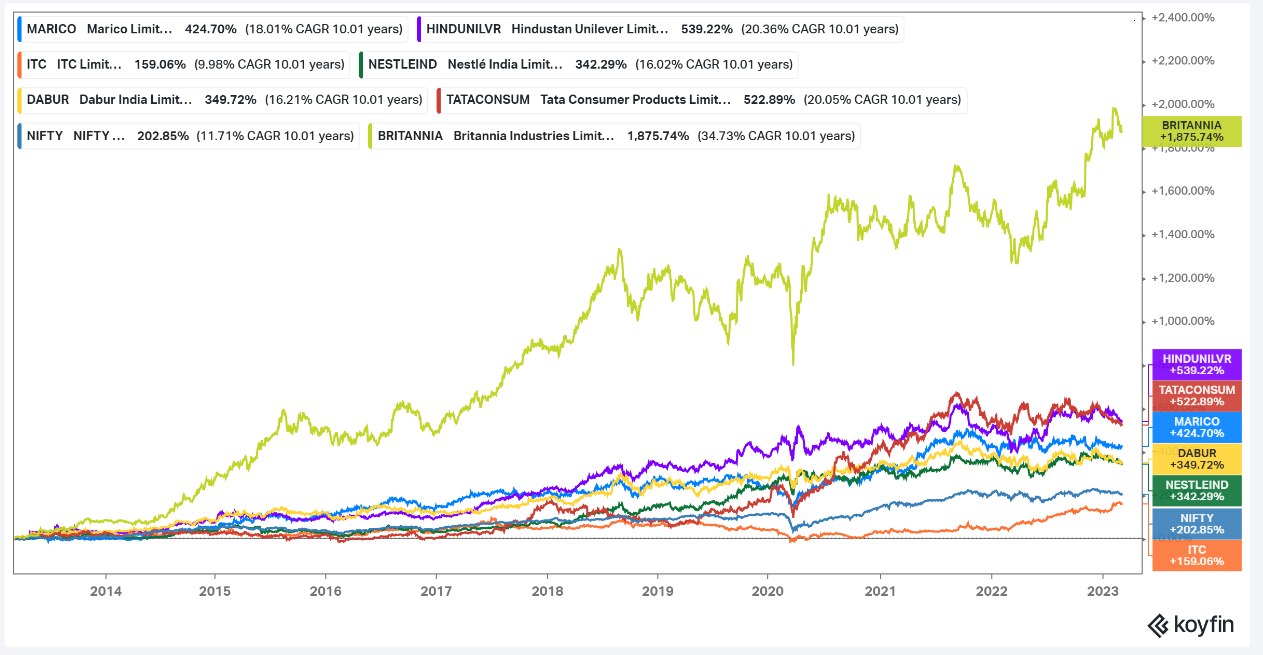

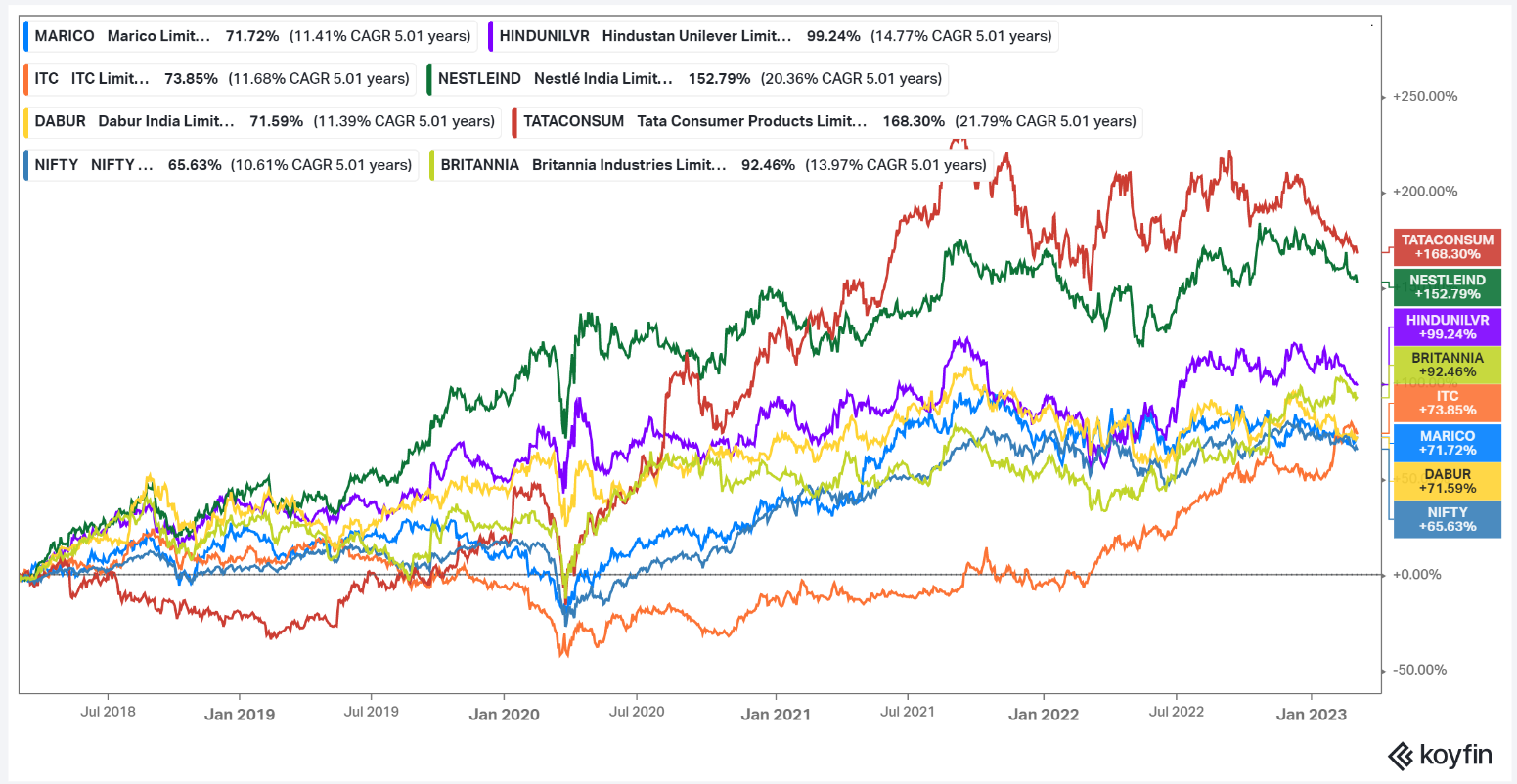

Sharing stock performance of all the stocks mentioned in the article for 5 and 10 years. Compensation should be commensurate with TSR.

| Subscribe To Our Free Newsletter |