Wanted to talk about this wonderful business Divi’s but never got the chance since the price it was trading was too high. Let’s go to Divi’s details:

- Divis is a pharmaceutical player involved in primarily 3 lines of businesses: Generic API manufacturing, Custom Synthesis and Nutraceutical

- As is a folklore, Dr Murli Divi started this company after working with Dr Reddy’s. In the first avatar, they were the consultants to the Pharma players and used to provide the consultancy for optimal production process

- Slowly they started putting up their own machinery. Since they had years of expertise in providing consultancy for cost optimisation, they started manufacturing naproxen at much lower cost vis a vis competitors

- Coming to the revenue mix, out of the revenues of 9000 cr, 630 cr attributes to nutraceutical. For the remaining, 41% gets attributed to generics (3431 cr) and 59% to custom synthesis (4938 cr)

- The company is having 2 units for manufacturing in Hyderabad and Vizag. The first manufacturing comprises of 2 units and the second manufacturing comprises of 4 units

- The company focusses on process chemistry and revisits the processes to produce API after fixed intervals. This process detailing leads to the lowest cost of API

- This is another reason that the company focusses on just a limited set of 30 API’s as compared to 100’s by competitors. Another 10 are in the pipeline

- These small set helps the firm to keep the focus on optimising production costs. Also, Naproxen & Dextromethorphan contributes to the significant amount of sales. Divis has 90% market share in naproxen and 70% in Dextromethorphan

- Newer generics like Pregabalin, Methylamine currently has 20-30% market share which can go to 60-70% market share

- So there is a trend in Divis playbook. Master the production process of the focussed API so that no other player is able to match its cost and thus dominate the market share

- Then there is another division of custom synthesis where Divis partner with big Pharma and manufactures API for innovator drugs and drugs under clinical trials

- This is the part which is having high margins since the big Pharma players are able to cough good money for the quality, no conflicts of interest. Innovator drugs API cost is 2% of final drug price

- Whereas generic API forms ~50% of final drug price. This shows the importance of cost optimisations in generics whereas ability to protect IP for big Pharma in case of custom synthesis

- As per the latest concall, generics and custom synthesis contribute 55% and 45% of the product mix respectively. The land at Kakinada for the third plant has been allotted to the company.

- In the latest quarter, the OPM was the lowest at 25% in the recent 7 years history. As per the management, the volumes for the generics are increasing and going to pre-covid levels

- Also raw material cost is easing. The pricing would improve in the coming quarter. But we have to wait and see the OPM in coming quarter

- Regarding the new technologies, the company is working on vapor-phased chemistry, continuous flow chemistry, photochemistry and Gadolinium compounds, which are the MRI contrast media agents

- The market size of MRI contrast agents stand at currently $6 Bn. With the focus on cost optimisation, there is a high probability that Divis would bee able to garner the significant market share

- The concall highlighted that the iodine recovery in contrast media is $75 per kg as opposed to $25 per kg giving it a significant competitive advantage. Once clearances are given, big Pharma can leverage these savings

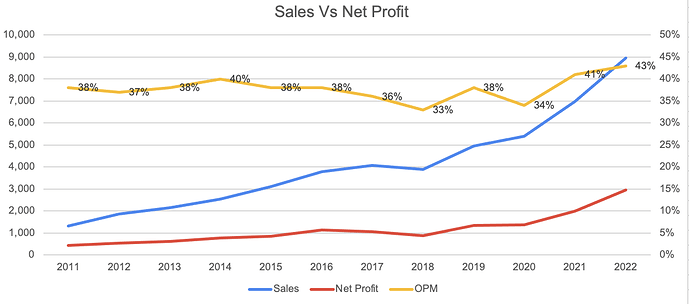

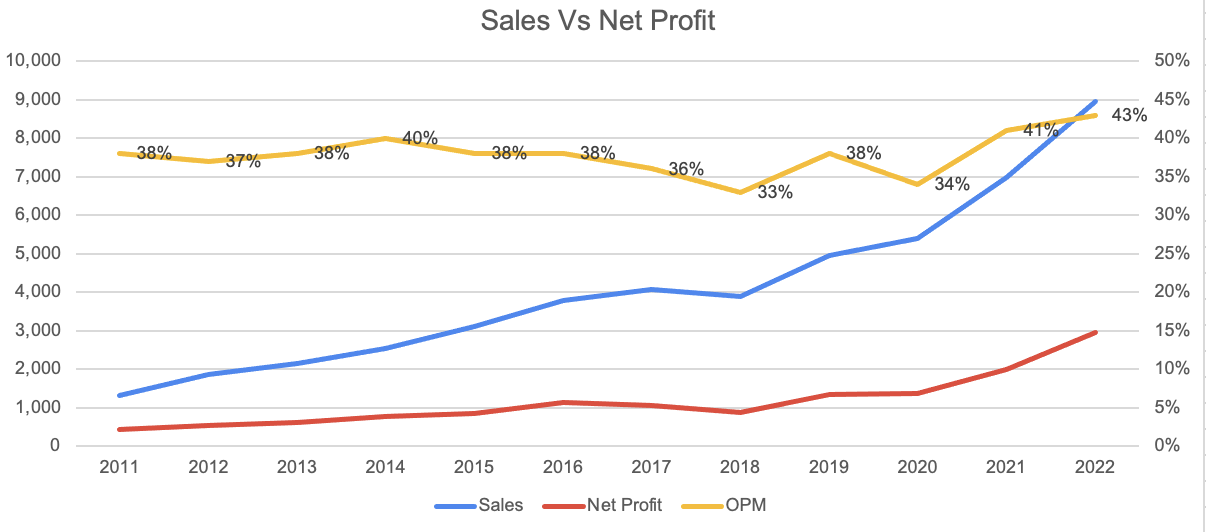

- Coming to Sales, this increased 7x from 2011 to 2022. Further the OPM is consistent at 35%. There was a recent jump in OPM due to capacity utilisation for covid drug API. But this seems to get normalised

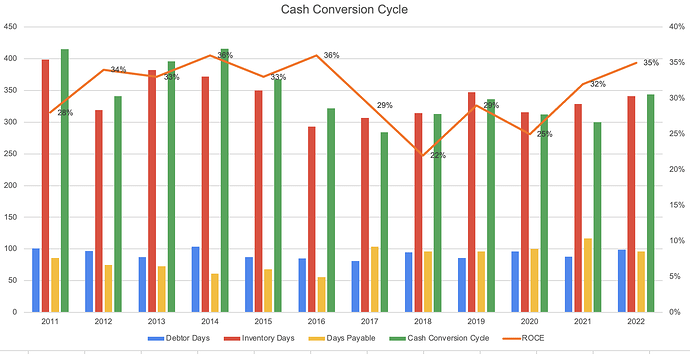

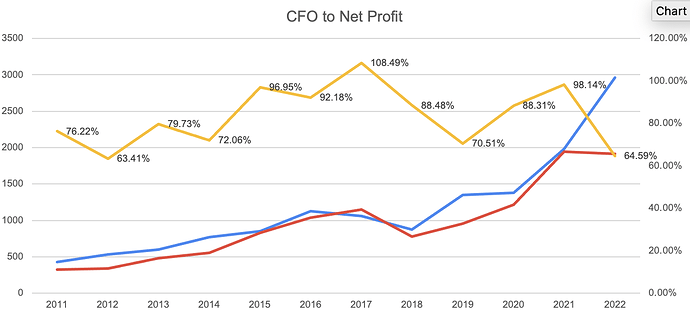

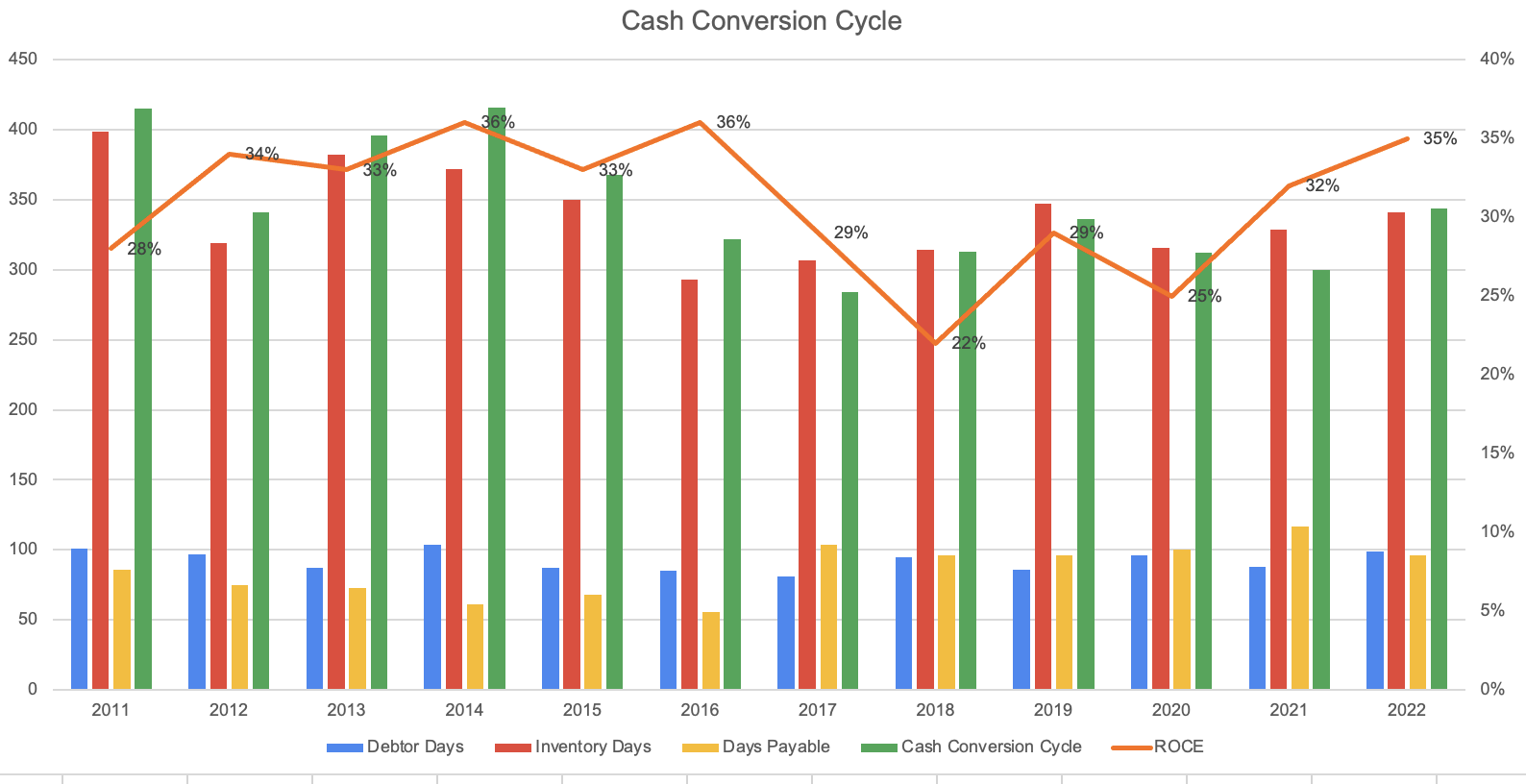

- The company is able to convert its profits to cash in timely manner. This is highlighted as shown in the following exhibit

- Coming to working capital cycle, the company’s cash conversion cycle is upwards of 300 days. The major reason is the inventory which the company has to stock.

- Manufacturing takes place in batches and not JIT. The manufactured API’s are stored in storage facility from where the demand comes and the API’s are shipped

- Regarding subsidiaries, the company operate two subsidiaries which are wholly owned: One in USA and other in Europe. They are engaged in customer development and marketing

- As shown in the screenshot of related party transaction, the company paid 8.7 cr as a rent to Divis properties which is controlled by KMP. Also Murali Divi took 110 cr as remuneration and short term benefit

- On the Sartans end, Divis is the only awkward integrated manufacturer. They make own Ortho Tolyl Benzonitrile using photochemistry and thus having the lowest cost in the world

- Competitive Advantages for the company includes its patented manufacturing processes which produces the lowest cost API’s, its focus on revisiting the chemistry and improving it to optimize costs

- Another advantage includes the economy of scales enjoyed in some key API’s which further keeps the pricing competitive.

- 100% IP compliance and focus on advanced reactions which cannot be built in house for big Pharma is another advantage

- Key risks include the dilution of R&D culture set buy Dr Divi once his children succeed. This is the biggest forte for Divis. Big Pharma moving their synthesis in-house is another key risk

- Competitors making the cost of API’s optimised by focussing on R&D is another key risk.

Twitter Thread:https://twitter.com/manujindal2803/status/1632921517846671365

| Subscribe To Our Free Newsletter |