A few critical observations from the Varun Beverages Annual Report for FY22 that caught my eye. Note that this is not the formal analysis of the AR, I am not commenting on the usual stuff like growth rate / margins / volume & segment information etc. which is readily available elsewhere – and all of which looks very good!

-

The company is a net foreign exchange consumer. Last year, forex consumed was Rs.956 crore and forex gained was Rs.230 crore. Rupee depreciation affects the company adversely.

-

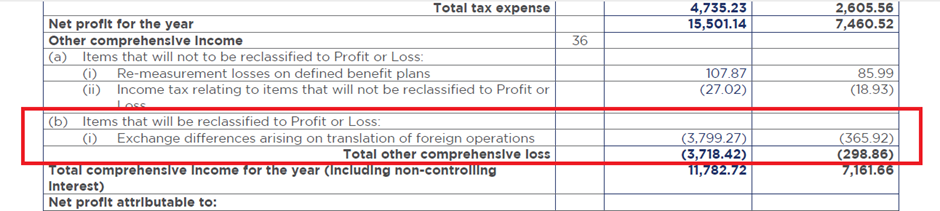

In FY22, there was a forex gain in India operations (Standalone P&L) of Rs. 46 crores but a forex loss of Rs.6 crore at consolidated level, implying forex loss in international operations. More importantly, a huge forex loss of Rs.380 crore is accounted under OCI. This is almost 25 % of the annual PAT.

My understanding is that unless the rates move back in the opposite direction, this loss will hit P&L in the coming year.

-

Franchisee Rights & Trademarks worth Rs.604 crore is capitalised as Intangible Assets. The current license agreement for India with PepsiCo India is till April 30, 2039. Company says this can be renewed at nominal cost and with no specific conditions attached, and therefore Franchisee Rights & Trademarks are no longer amortised. If these are amortized over a 20-year period, there will be a hit of Rs.3 crore per annum to the P&L.

-

Addition to Franchisee Rights was Nil during the year, despite company starting new operations in Morocco to distribute and sell Lays, Doritos and Cheetos. Not sure if this agreement is somehow different from other agreements elsewhere which created the Intangible Asset in the first place.

-

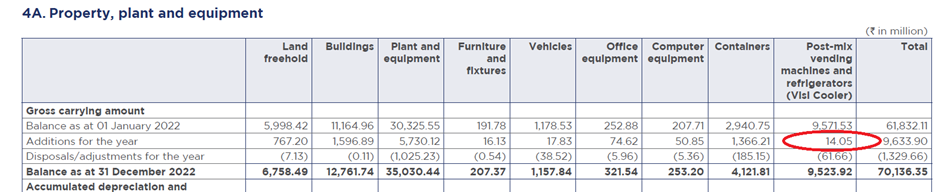

The large number of visi-coolers installed by the company at retail outlets is another fixed asset in the Balance Sheet. The number of visi-coolers installed have gone up from 840,000+ in FY21 to 925,000+ in FY22 i.e. 85,000 new visi-coolers installed during the year. At a cost of around Rs.15,000 per visi-cooler, there should have been an addition of Rs.125 crore to the asset base (gross block). However, addition to visi-coolers in Fixed Assets Schedule is just Rs.1.4 crore in Standalone.

Even if one assumes most of the new visi-coolers were installed outside India (unlikely), the addition in Consolidated is just Rs.43 crore. The numbers don’t match, not sure what I am missing here.

-

Rs. 185 crore of operating revenue is Government Grants under different industrial promotion tax exemption schemes. Outstanding government grants went up from Rs.185 crore in FY21 to Rs.301 crore in FY22. State governments are notorious for delaying on their obligations.

-

Company has operations in Zimbabwe, which is a hyperinflationary economy. Zimbabwe does not have a proper stable currency of its own, and hence conversion / translation of the transactions into INR are prone to inherent subjectivity.

-

A large part of the Annual Report is devoted to ESG, especially the company’s efforts at water conservation and management. Clearly, the company understands that cost and availability of water is the main risk to the long-term viability of the business. And for that, they are dependent on agreements with local municipal authorities. I went back to more than 5 years of analyst concalls but there is not a single question on this. What is the cost of water in the overall cost structure is not clear, and can the authorities deny committed quantities of water in a drought year? Interestingly, even the DRHP is silent on what I think is the most crucial aspect of this business (or maybe I am being unnecessarily paranoid).

-

Mr. Ravi Jaipuria made a Rs.56 lac settlement with SEBI with respect to a case during the year.

Just nit-picking, perhaps!

(Disc.: Invested)

| Subscribe To Our Free Newsletter |