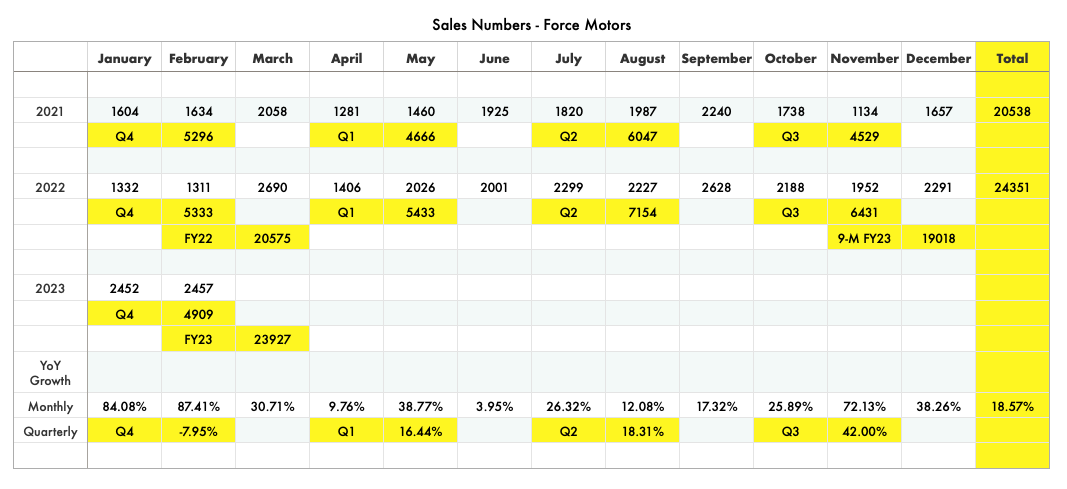

If we look at the monthly numbers of Force Motors – They are improving MoM since Nov-22 (post Diwali peak)

With new product launches such as Urbania, Gurkha 5-door variant – these numbers should sustain and improve.

With 1 month to go (which is a festival month – sales should grow MoM) – Force has already crossed FY22 sales by 17% and only 424 units short of Q4 FY22 sales number.

With demand of luxury car manufacturers (BMW, Mercedes) rising – Force is also showing improvement in its ancillary (engine) business (though separate data is not available – topline increased QoQ in Q3 inspite of fall in sales data by 10% QoQ).

JV with MTU (subsidiary of Rolls Royce Group) has also started operations from FY-21 and capacity utilisation is increasing as well – This JV should cross sales of at least 300-400 Cr in FY24 with peak sales potential of 1000 Cr (Force has 51% stake in JV) – With increased localisation of RM content, EBITDA margins should be north of 14-15% in this business in a couple of years (Source – Credit rating of Force MTU Power Systems).

The stock is trading at less than 0.95x P/BV (which is very cheap considering the capabilities they have).

Even if we look at EV/EBITDA then TTM is 10.6x (this is after they posted EBITDA loss in March-22 quarter) – If we extrapolate last 2 quarters avg ebitda then EV/EBITDA comes at 8x which is very cheap for an OEM which is fully integrated and have JVs with companies such as BMW, Merc, Rolls Royce.

Price/Sales of 0.38x (TTM) – No comments but this is extremely cheap (for an OEM + Ancillary company, P/S of 1x is justifiable)

Now if we look at the financial performance :

Depreciation has increased by ~ 90 Cr since FY19 (primarily due to capex on newer platforms and BS-VI variants)

TTM Sales are already at an all time high and EBITDA margins have started improving too.

With interest cost going down (as company has started debt repayment) – we should see company turning profitable on a consistent basis.

Disclosure – Invested and biased – Please share your views (would love to discuss)

| Subscribe To Our Free Newsletter |