Im quite glad someone (@ankit_george bhai) decided to create a thread on MTAR. This is one company that IMO as VP we need to do a good job of nailing down because its the rare category of companies that come for an IPO.

Lets start off by talking about the two most prominent risks i see in the investment thesis & then work around that.

Risk 1: How will you fund the growth

Each business has its characteristic in terms of being:

(i) Capital light

(ii) Capital Intensive : Fixed asset heavy

(iii) Capital Intensive : Working Capital heavy

MTAR falls in a mixture of second & third category. We know that because the WC as of Sep-22 balance sheet is : 322 cr compared to Quarterly revenue runrate of 160 cr or so in Q3. And compared to fixed asset base of 238 cr.

The net worth of the company is 562 cr. If we assume Q3 runrate of Profits & that profit gets added to Net worth, the 1 year forward ROE would be 18.5%. If we assume that they can grow the guided 50% & reach 900-1000 cr topline in FY24 with same margins as right now, we end up with 24-26% ROE.

How is this ROE expansion happening despite stable margins?

This is primarily due to better capacity utilization. We know from from MTAR’s brochures from 2021 that they have 370+ machines in aggregate.

What would be nice to understand in subsequent management interactions (like concalls) is the time wise asset utilization here. Given that MTAR performs a wide variety of activities (from mechanical, to incrementally more in sheet metals, electronics, ceramics) it would be hard to calculate a blanket capacity utilization but we can definitely calculate a time wise asset utilization (what % of time that we can run an asset productively are we running the asset productively averaged over all assets).

Given that they have guided for a roughly 66% growth in profits compared to Q3 runrate in FY24 my sense is that there might be significant headroom to increase asset turns & thus ROE.

Having said that, even in the best case scenario wherein they can reach 26-36% ROE in next 1-2 years & not dilute equity, at some point they would have to dilute equity given that their growth rates are higher than their ROE (Guide of 50% growth in FY24 over FY23, 5x revenue in 5 years & bloom growth guide of 30% cagr over a decade)

This is a key event to look out for. Typically cos that raise equity in market end up underperforming at least for a few years (though there can always be exceptions to the rule).

Risk 2: Where are the cashflows

When one analyzes this business at first glance it would seem like a poor quality business because of the lack of cashflows.

There are Two kind of capital for growth

- Working capital (inventory, receivables)

- Capital expenditure (plant, machinery)

#1 is accounted for in operating cash flow

#2 is accounted for in cashflow from investing activities

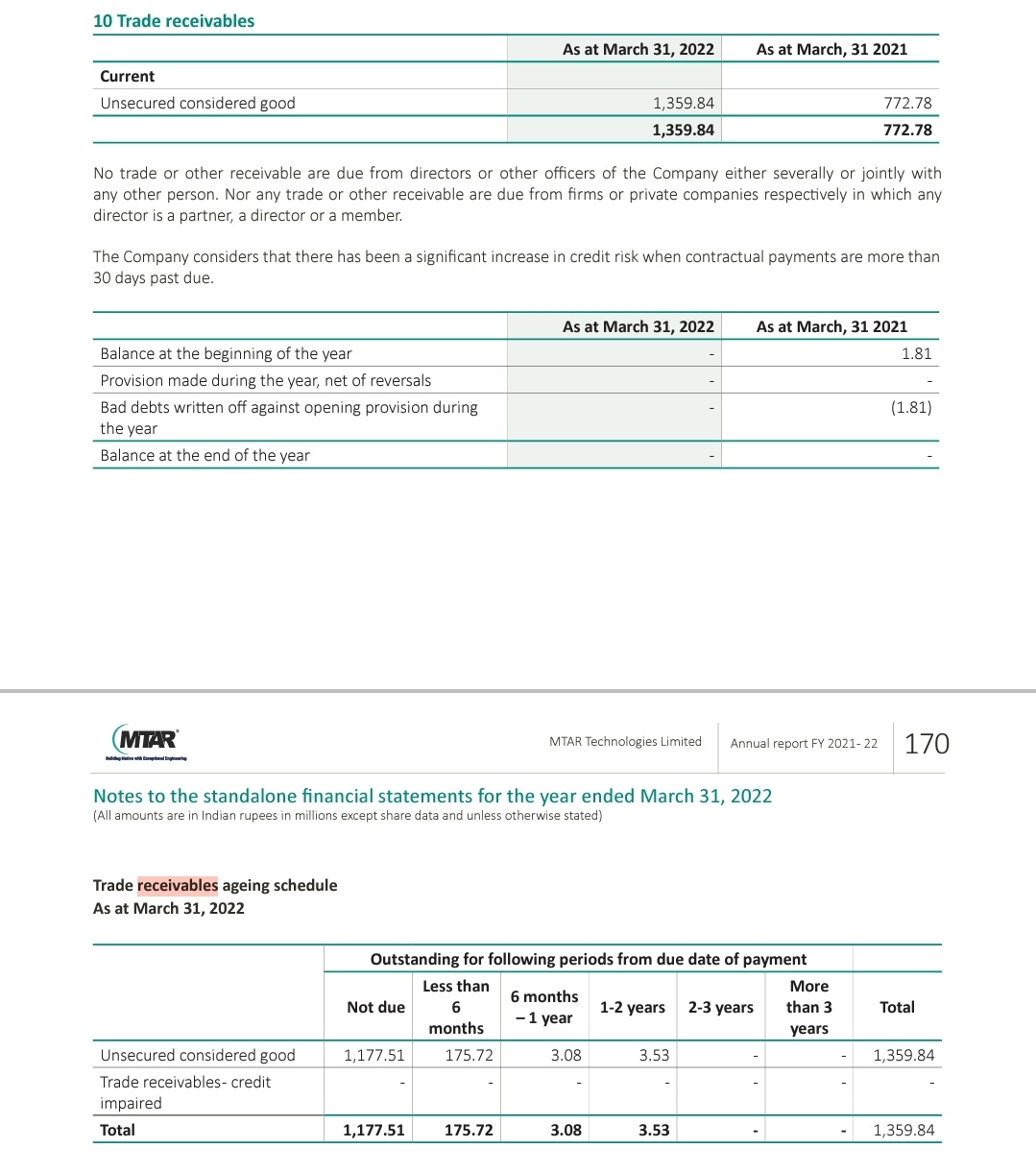

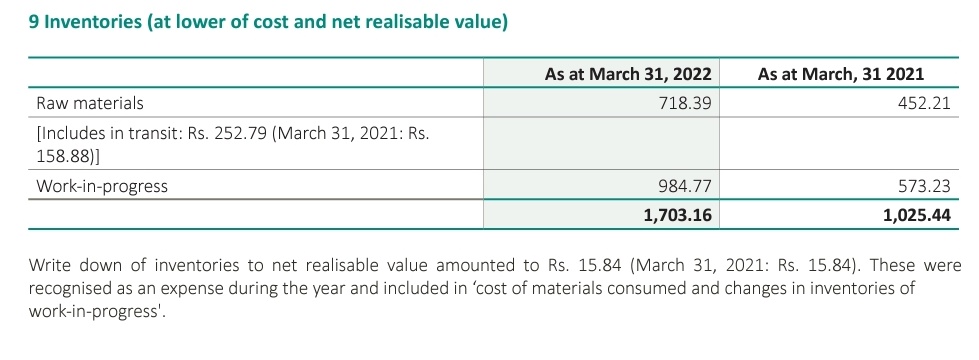

Have a look at the breakup of inventory & receivables for MTAR.

- 90% of receivables are not even due. They are essentially part of the payment terms

- 100% of inventory is raw material & cwip (higher rm for growth & higher cwip due to longer execution timelines)

- No finished goods inventory (except what is in transit to the clients)

- No credit impaired receivables over last 2 years

- Negligible inventory write down

We can Read the concall to understand why the inventory is high. It is due to the fast growth and the long execution cycle.

The high inventory is a characteristic of the biz. Serves as an entry barrier for any new entrant

In short, the cashflow will fund working capital & keep OCF depressed at least until we have high growth.

Risk 3: Valuations

THis is always a tricky & subjective discussion because its a fuzzy concept. We can know a very undervalued company. And a very overvalued company. Everything in middle is fuzzy. How should we think of MTAR?

Per the Q3FY23 guide, FY23 profits should be around 120 cr. Around 43x FY23 earnings. (FY23 will close in 20 days, so this is not really forward looking).

Per the Q3FY23 guide, FY23 profits should be around 180-200 cr. 26-29x FY24 earnings.

Keep in mind that company grew 80% in FY23, guide for 50% growth in FY24, & 37-40% Growth in next 5 years (historically have underpromised & overdelivered).

Definitely not egregiously undervalued. Maybe fairly valued perhaps a bit overvalued. Definitely no margin of safety. This kind of valuation will only sustain until they can keep delivering this kind of asset turnover increasing, ROE expanding growth.

Investment thesis

Despite these risks, why did i chose to invest & how to tackle these risks? I like to think of each company in terms of its unique differentiated value proposition to society. MTAR sort of stands out here.

The best way to understand MTAR is from the eyes of their clients.

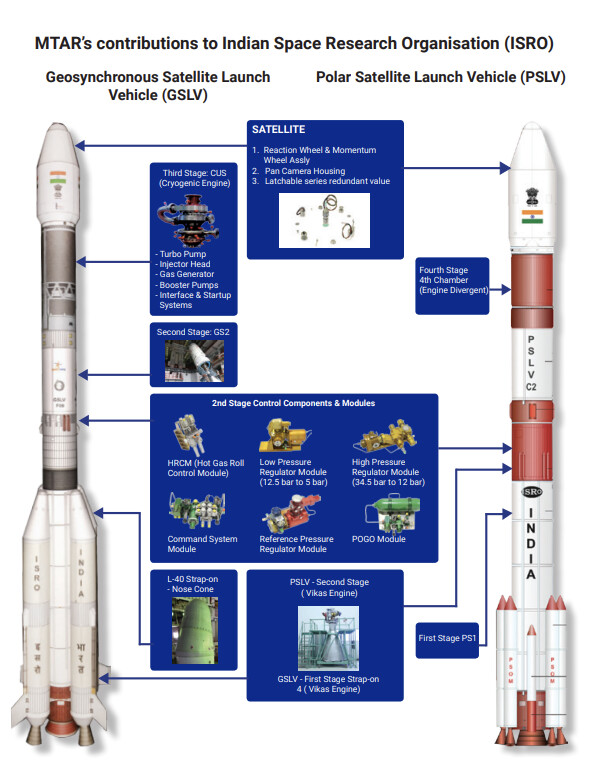

MTAR has significant value addition in ISRO GSLV & PSLV rockets. The vikas engine which is used in 1st stage of GSLV & 2nd stage of PSLV is co-developed with ISRO & manufactured by MTAR. the L-40 Strap-on Nose Cone, Command System Module, Reference Pressure POGO Module, Regulator Module, Low Pressure Regulator Module (12.5 bar to 5 bar), HRCM (Hot Gas Roll Control Module), in the cryogenic engine, the Turbo Pump, Injector Head, Gas Generator, Booster Pumps Interface & Startup Systems are all manufactured by MTAR. The engine for PSLV-C25, which launched the Mars Orbiter Mission Spacecraft, as part of the Mangalyaan mission, was supplied to ISRO by MTAR. Further, the engine for the PSLV-C49, which recently injected the EOS-01, an earth observation

satellite, was also supplied to ISRO by us. Was also integral for the GSLV Mark III

engine for the Chandrayaan II mission.

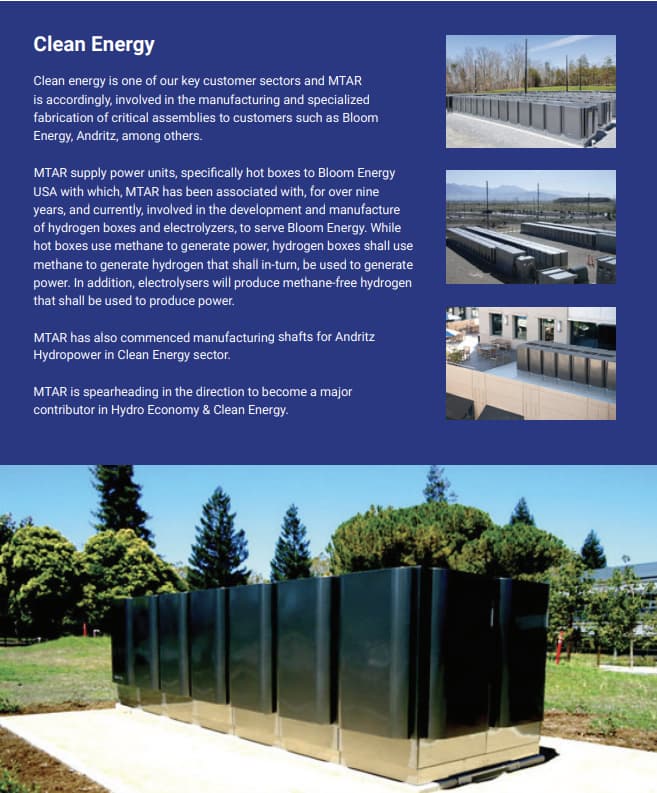

Right now the workhorse for the revenues of MTAR is bloom SOFC (solid oxide fuel cell) boxes. There are multiple growth levers which MTAR is yet to bank on in the future:

-

Ramp upf hydrogen boxes and electrolyzers for Bloom in about 1 year

-

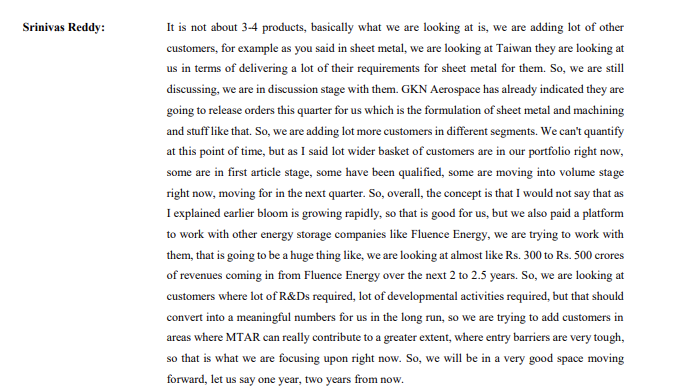

2 us based energy storage cos which can be as large as bloom in 2 years (so two 300-500 cr energy storage clients)

-

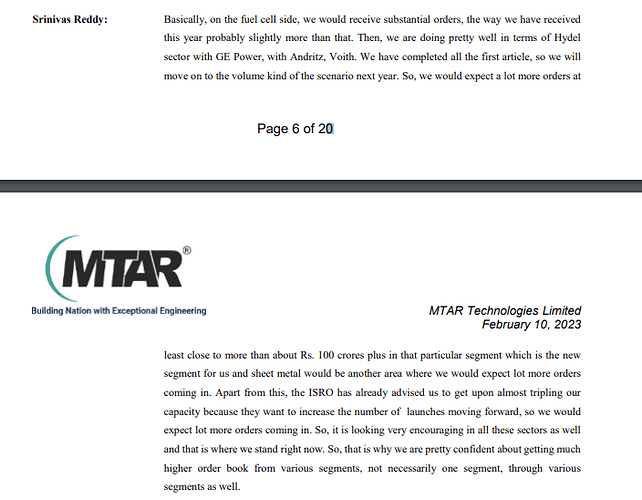

Isro asking mtar to triple capacity + MTAR is building their own own smallsat launch rocket in next 3-4 years (can easily become 400cr + given 1 smallsat launch costs around 7-8 cr (SpaceX slashes base price of smallsat rideshare program, adds “Plates”)

-

Sheet metal, hydel, ceramics can become ~100 cr segments individually leading to increased wallet share of bloom & other energy boxes (all boxes) for MTAR

-

Bloom has a revenue CAGR guidance of 30% for next decade.

Disc: Invested, biased. Position sizing is proportional to risks (specially valuation risks; might look to add more at lower valuations if thesis is in tact)

| Subscribe To Our Free Newsletter |