Owner of HINDUSTAN,LARGEST NEWSPAPER IN BIHAR, JHARKHAND. SECOND LARGEST IN UP. Hindustan ranks as the second largest-read daily in the country.

Hindustan has 4 editions and 113 sub editions across the Hindi belt. They are spread across Delhi, Bihar (Patna, Muzaffarpur and Bhagalpur), Jharkhand (Ranchi, Jamshedpur and Dhanbad), Uttar Pradesh (Lucknow, Varanasi, Meerut, Agra and Kanpur) and Chandigarh. Apart from these, the paper is also available in key towns like Aligarh, Mathura and Allahabad.

The stock is trading at PE, which is lower than its peers than Daini Bhasker and Jagran Prakashan. So in that sense this is a good value media pick because along with its synergies with HT Media it is able to sustain growth over a longer period of time

Fastest growing, in readership and profitability:

Hindustan, the Hindi daily of HMVL, is the second-largest daily in India (IRS-2014), growing by 25% through 2010-2014. HMVL’s EBITDA has grown 14.85% CAGR through FY11-FY15, significantly outperforming peers. HMVL has also registered significant gains in the UP market in IRS-2013, which provide for a strong long-term growth engine for the company. It can be note that UP market is the largest Hindi advertising market, and management expects that readership growth can enable growth of 2-3x in revenues from Uttar Pradesh.

UP & Uttarakhand (UK) to act as growth drivers for HMVL

HMVL’s readership in UP & UK grew at strong CAGR growth of 26% from 2.5 mn in 2009 to 8.1 mn in 2014 and entered into 2nd spot in UP following Dainik Jagran. With HMVL moving to 2nd spot in UP, which is the largest market for advertising industry with size of Rs.12 Bn, HMVL has started to increase the advertisement rates charged to companies LEADING TO EXPANSION IN MARGINS.

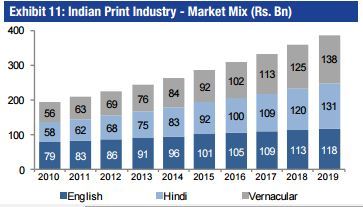

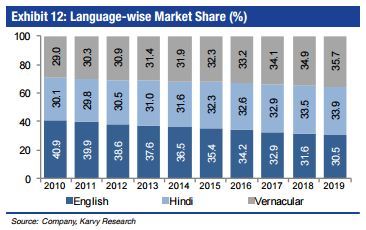

Hindi & Regional markets growing faster than the English markets

Literacy rate is one of the key factors behind the growth of Indian print industry. As literacy rate increases in Indian states, people tend to start reading newspapers as they get familiar with their regional language. Hindi and regional markets control 64% of Indian print Industry and likely to witness CAGR growth of 9.6% & 10.4% respectively. Print is the preferred mode for advertisers in India where companies spend 42% of total ad spends on print. Advertisers prefer print as it is better medium of reach to the non-metros, Tier-III and Tier-IV cities compared to digital & TV. Literacy rates in Hindi states are lower compared to national average which is expected to support growth. English market is likely to witness a slower CAGR of 5% compared to industry growth of 8%, on the back of shift towards digital media as the segment is catering mostly to big cities and metros where internet penetration and spending power is high.

Newsprint costs on decline

Newsprint is the major input and forms 51% of the company’s total expenses. With newspaper circulation declining in advanced economies on the back of shift towards digital, the demand for newsprint is on decline leading to cooling of newsprint costs. Further, transportation costs also to come down on the back of declining fuel costs. Newsprint prices have been coming off in the

last couple of years from $640 per ton in 2012 to $540 per ton in Q1FY15 according to karvy reasearch , As a result, raw material expenses as % of sales started to decline from 43% in FY12 to 41% in FY15.

Way to valuation convergence – growth, visibility, easy base to beat:

We believe HMVL shall register industry-beating revenue growth in the coming quartersenabled by strong growth in readership. Also, competitive intensity has begunto reduce in Jharkhand (strong growth in realization/ copy of DainikBhaskar). Lastly, on account of high employee expenses (Majithia Wage board) and promotional activity in Bihar (Patna launch of Dainik Bhaskar in 3QFY14), 3QFY14-2QFY15 have set up an easy to beat base. HMVL is set to register 35% growth in EBITDA in FY15-FY16 period, which will ensure earnings growth looks attractive in the coming quarters.

Near-term, earnings are likely to be well- supported by elections in key geographies further improving visibility:

HMVL will see elections in all of its key geographies in the next 24 months, starting with Bihar (3QFY16), and followed by Uttar Pradesh. The company’s earnings growth visibility, as well as industry – outperformance, is bolstered by these events.

PROS:

1.CONSTANTLY INCREASING OPM FROM 17.07 IN FY10 TO 20.33 IN FY15

-

NET PROFIT MARGINS INCREASE FROM 10.31 TO 17.20.

-

ROE INCREASE FROM 14% TO 19.19% and consistent free cash flow geneation.

-

MARKET CAP OF RS.1650 CR AND NET CASH OF RS 576CR.

-

BIHAR ELECTIONS ON ANVIL.

-

INSPITE OF GENERAL ELECTION ADSPENDS IN Q1FY15,

IT SHOWED A REMARKABLE INCREASE IN Q1FY16.

PROFIT INCREASED BY 23%. -

DECREASING PRICE DIFFERENTIAL BETWEEN ADRATES OF ENGLISH AND HINDI NEWSPAPERS.

-

INREASING READERSHIP AND CIRCULATION REVENUE.

CONS:

1. NO SPECIFIC AGENDA FOR DEPLOYEMENT OF CASH HOARD.

- VERY LOW DIVIDEND INSPITE OF HEALTHY CASH FLOWS.

THIS STOCK DESERVES A DEEP LOOK AS IT IS AVAILABLE ON PE OF 10-12.

MANAGEMENT

Mr. Vivek Khanna

Chief Executive Officer

Vivek Joined HT Media in 2008 after working for more than 16 years, of which 11 were spent with Hindustan Lever Limited (HLL). He led strategic and marketing initiatives – segmentation, positioning, advertising & new product development at HLL. In his last assignment he was Director Marketing with Aviva responsible for the Company’s product & marketing strategy. At HT Media Mr. Vivek Khanna set up the Ad for Equity (AFE) business. He ran the AFE business and Mint business for the last 5 years, growing these from small insignificant numbers to a strong & significant size.

He is the architect of current good shape in which HMVL is.

SHOBHANA BHARTIA

The media CZARINA. Owner of HT Group and daughter of late Mr. KK BIRLA.

disclosure: I currently have no stock position in the stock.

| Subscribe To Our Free Newsletter |