Here I am posing a question with reference to two companies as to whether the stocks become worthwhile if the companies start receiving orders.

Here is the first. Patel Engineering. As per the website of the company, it is into, “all sectors of the Infrastructure industry from dams, tunnels, micro-runnels, hydroelectric projects, irrigation projects, highways, roads, bridges, railways, refineries to real estates and townships.”

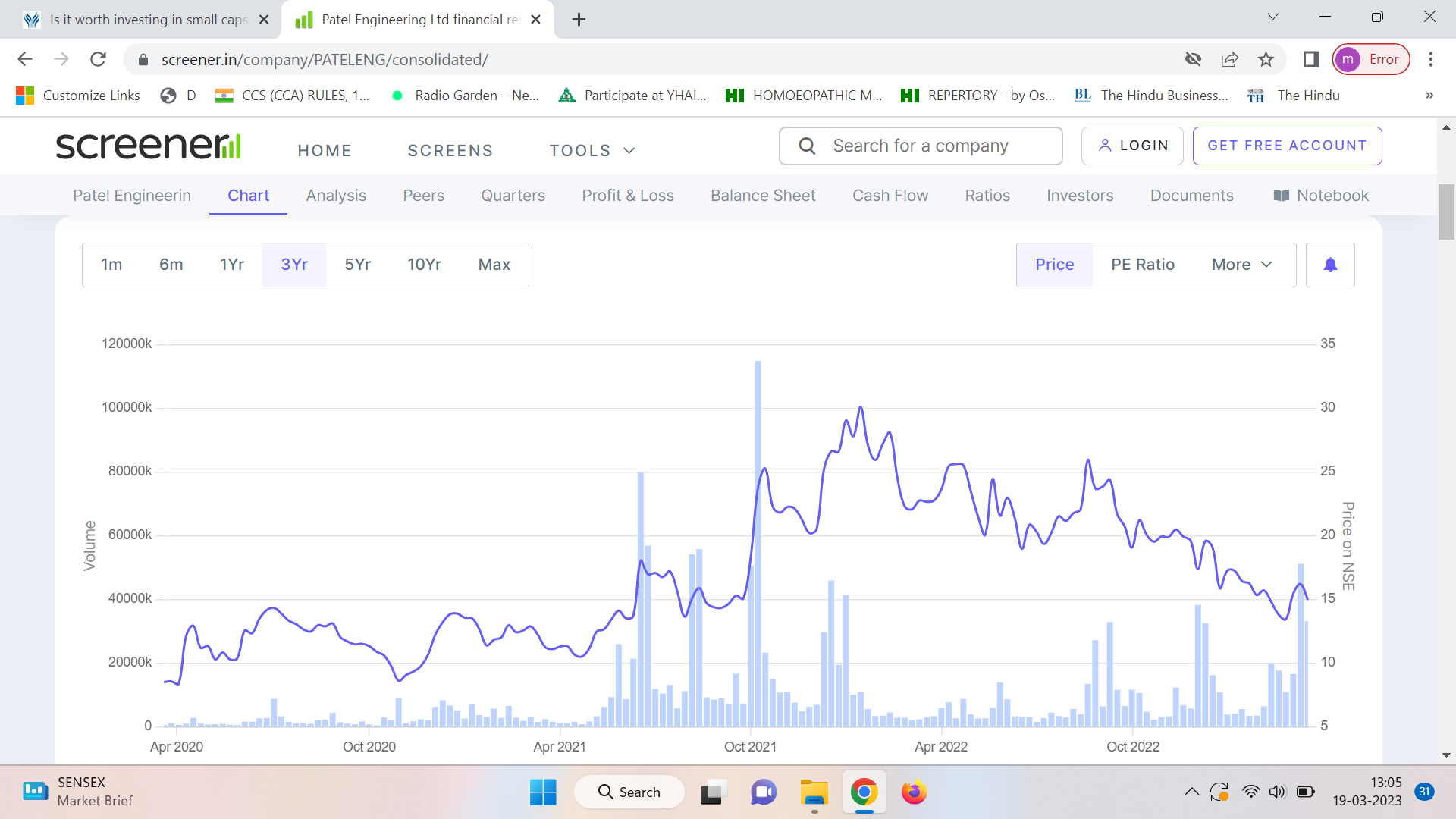

The price graph of the company does not makes for an appetising viewing.

Even the past financials are not exactly inspiring.

The PE is rather low. This is what, alongwith the spate of orders it has received, and the fact that it is really trading at a rock-bottom price arouses interest.

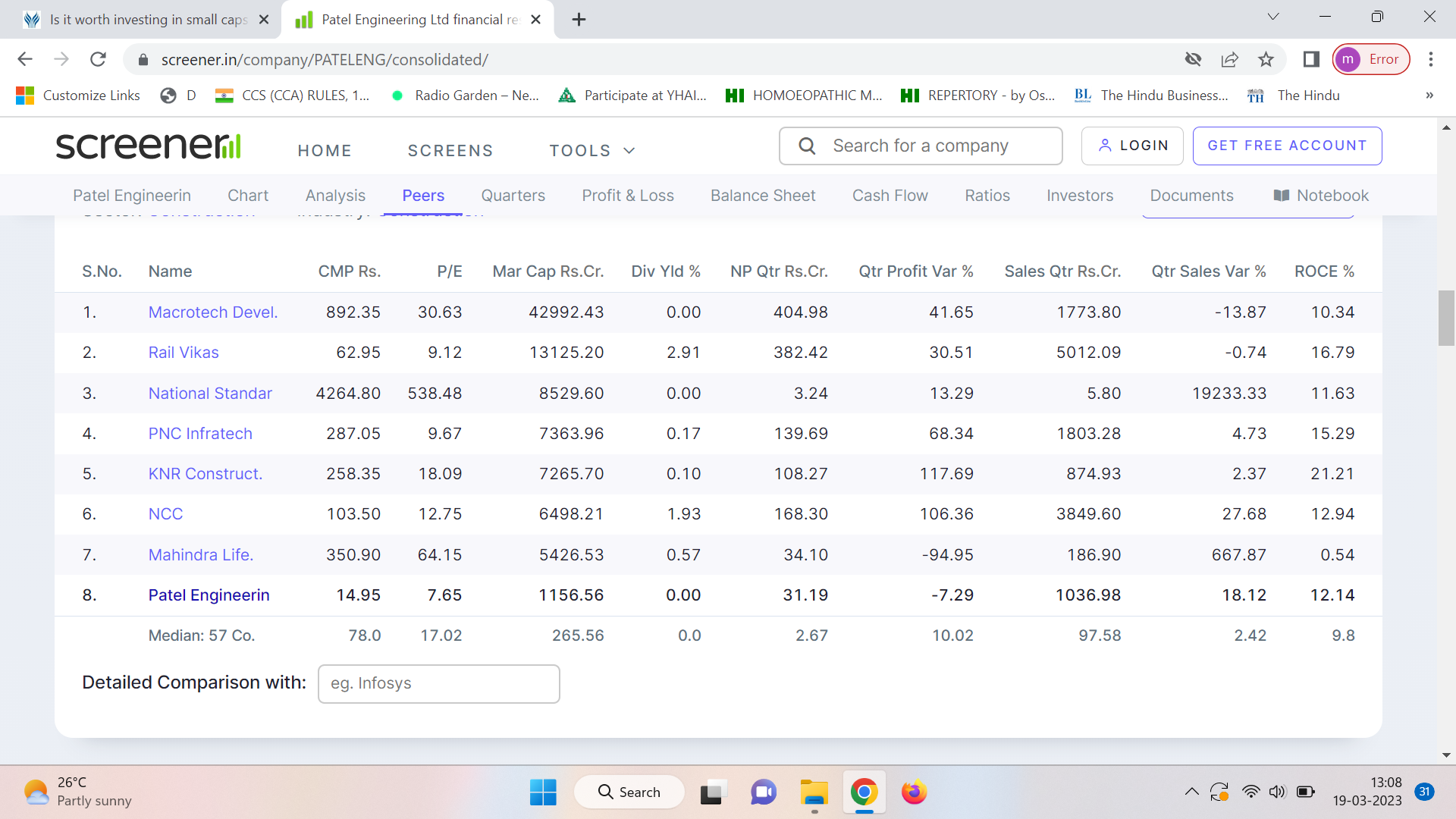

What is however not palatable is the fact that it has a debt of ₹ 2,221 Cr, which is more than its market cap of ₹ 1,157 Cr.

This makes it practically a basket case.

As for the orders I have mentioned earlier, in the recent times it has received multiple orders. ‘Rupen Patel, Chairman and Managing Director of Patel Engineering Limited says, “In the recent past, we have declared L1 for four other irrigation projects located in Maharashtra, Madhya Pradesh and Karnataka. Further, these two new projects will help strategically deploy and utilise resources more efficiently. With these two new L1 projects, our share of order wins including L1 in this financial year is around 5,900 crores.”’ (March 16, 2023)

See also

The interest outgo for ’22 was ₹420 cr, whereas the net profit was only ₹72 cr.

Book value of the stock is ₹32, which is more than double of its current price.

So, should we in the light of the recent orders ignore its debt?

The other company under consideration is Vintage Coffee and Beverages. Vintage Coffee is into the manufacturing of Instant Coffee. They are primarily supplying to domestic markets and majorly exporting to various countries.

The Co. was acquired by Chin Corp Holding Pvt Ltd and its owners in June 2021. The acquirer bought around a 50% stake in the company at an offer price of Rs. 20 from the public shareholders. [2] Post acquisition, the name of the Co. was changed from Spaceage Products to Vintage Coffee and Beverages Ltd.

https://www.screener.in/company/538920/consolidated/

Over the last 4 years, Vintage coffee has established itself as a supplier to several companies in key markets such as Russia, Latvia, Turkmenistan in East Europe and Central Asia, Nouakchott, Mali, and Nigeria in West Africa, Myanmar, Malaysia, and China in S.E. Asia and Australia in the far east, UK and Spain in Europe and now getting ready to enter markets in India.

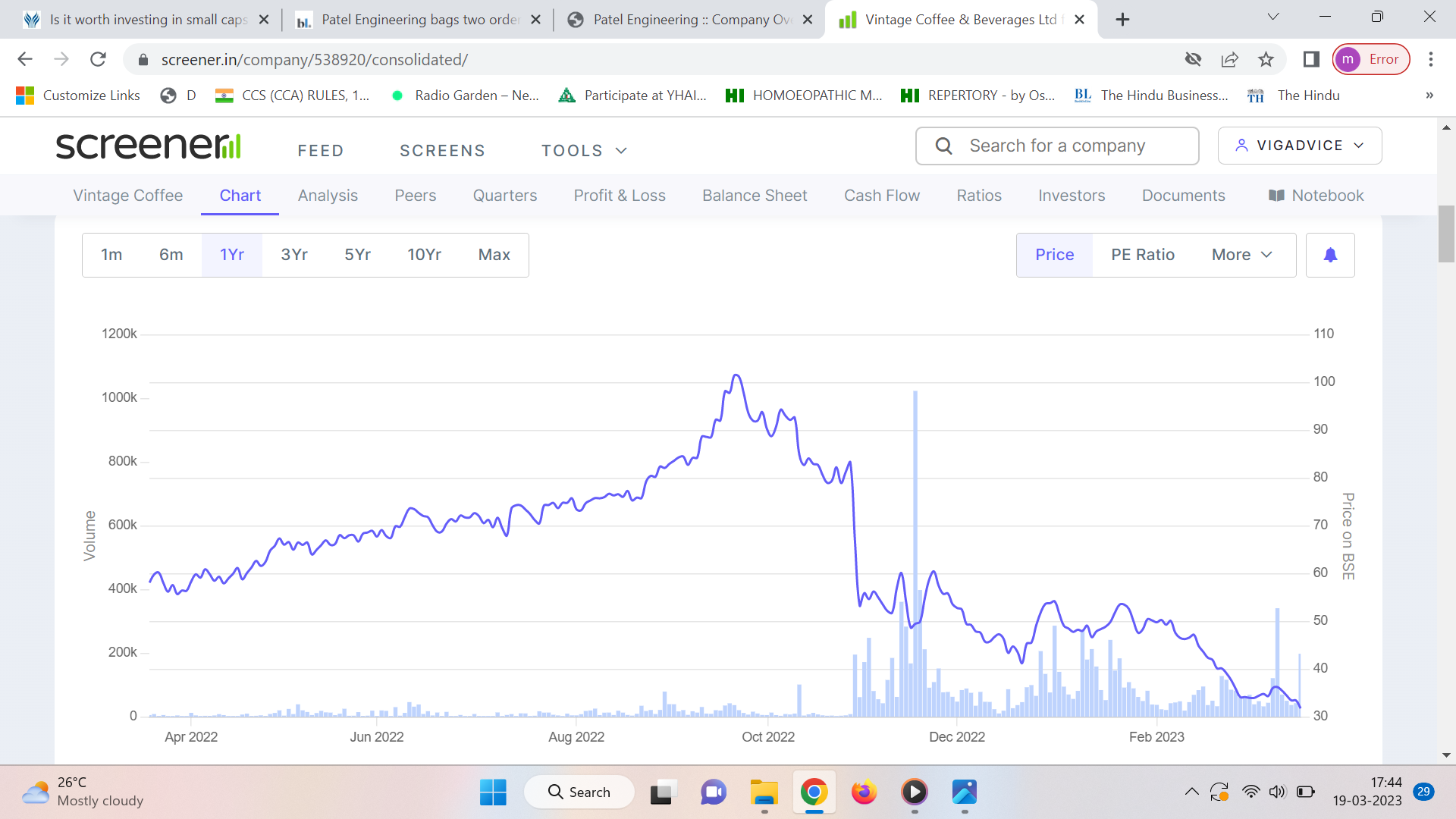

Again, the price of the share is at rock bottom. The trend looks like waterfall.

The book value in this case is half the current price of the stock ₹15.2 to ₹ 31.8.

The screen does not give any of the ratios, PE, ROCE or ROE. It made a net profit of ₹1.28 cr in the previous quarter. Last year its net profit was -12.27 cr.

Here, three things are of interest. The rock bottom price (Ben Graham would have recommended it?) and the orders it is receiving now.

Also, please see Vintage Coffee And Beverages Ltd bags order from South East Asia | EquityBulls

So, despite the low, almost negligible profits, are these two stocks worth a look?

Disclaimer: I have invested in them recently.

| Subscribe To Our Free Newsletter |