I have multiple subscriptions to various sources of market intelligence, and track the prices of chemicals this way.

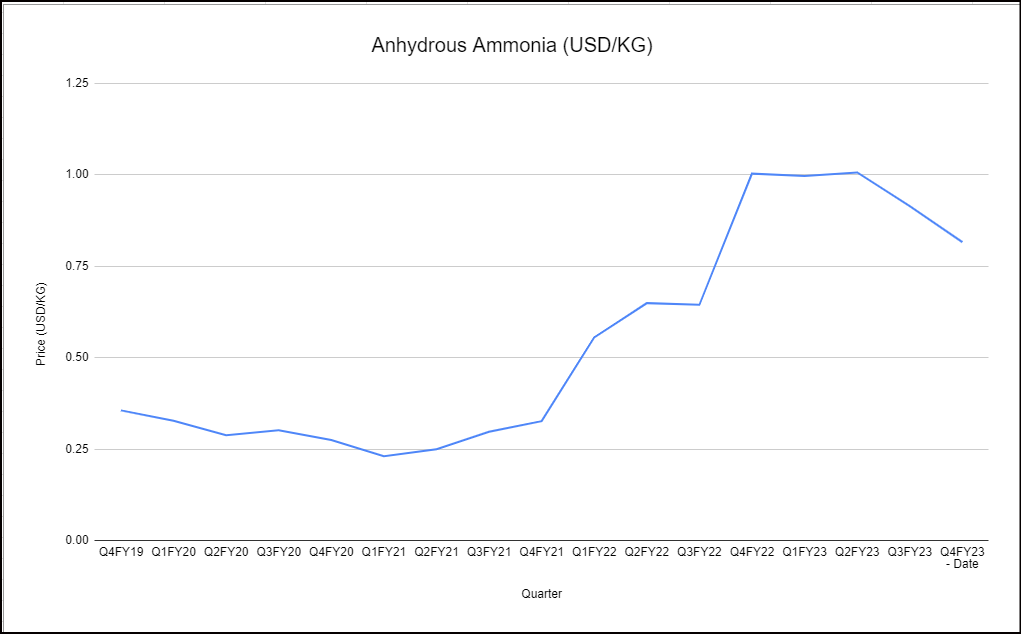

The price I’ve shown in the chart is the international price for ammonium nitrate. If you’d like to see the prices of ammonia, one can see the chart below. This is specifically the price Deepak Fert has paid for anhydrous ammonia over the last few years.

I think ultimately both depend on natural gas prices.

Natural gas → Ammonia → Ammonium Nitrate

The price of natural gas was the driver for the cycle seen in 2022. Then, Russian TAN supply was off the markets and had a knock on effect to the price of TAN. Now things have ultimately cooled in natural gas, and I think both ammonia and TAN will ultimately revert back to long term averages.

Hard to say. I think before the ammonia plant comes online, maybe 20-25% margins in TAN compared to the 35-45% margins seen in the peak of 2022. It’s hard to say because Smartchem has an NPK division inside it alongside TAN so the margins are not transparent. Similarly, the chemical division also includes nitric acid, which isn’t as high margin as TAN.

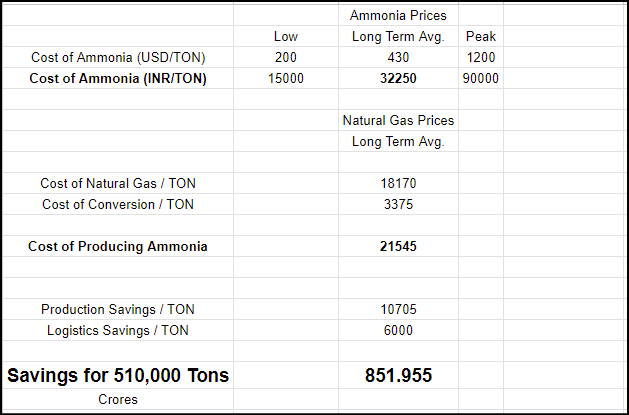

This calculation will of course change once the ammonia plant comes onstream. Management long ago explained the unit economics for cost savings and one can update it to include current prices:

As far as the fertiliser side of things is concerned, I wrote a post here:

https://twitter.com/Chins1729/status/1548322470637146115

To summarise, I have seen investors burn their hands in companies that have capex come onstream just after a powerful cycle. Here, the difference is that the capex is for in-house consumption. The plan however is to have a larger margin of safety before investing again.

With the demerger of their different entities, the hope is that the TAN vertical’s unit economics become transparent.

Hope this helps!

| Subscribe To Our Free Newsletter |