I re-read the transcript to understand their innovative CDMO business, Capex, better. Most of the Capex they are doing is going towards expanding existing high-margin businesses or targeting new innovative businesses, or expanding capacities where current capacities are running at full capabilities (Turbhe, Riverview, Sellsville).

In Q3, PPL went live with $42 million of Capex. This is mainly in Peptides, ADC, and in-vitro (within the glass) research facilities ((PDS Ahmedabad).

It is a high-margin business (although management said it is a high growth, it had revenue of less than 100cr, so I wonder if it will make a significant dent).

PPL is undergoing major capex at various sites across the work.

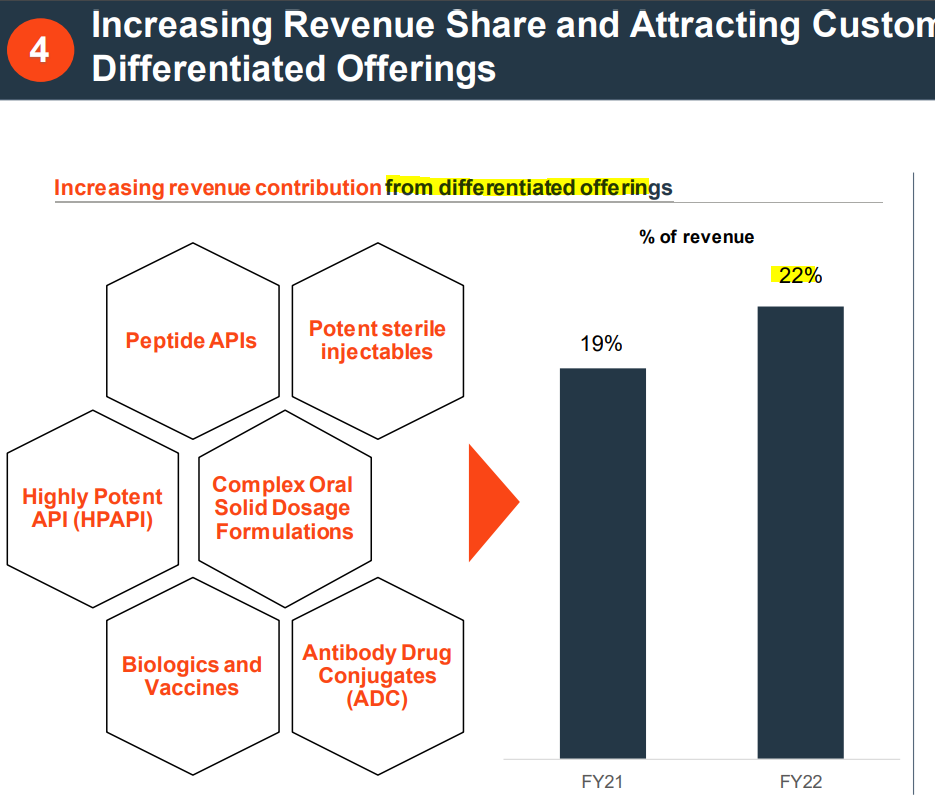

Another thing to track is how their differentiated offering is progressing. Although only some things here are patented, like peptides/ADC, these products have less competition and high margins even if they are generics.

As per management, most of the capex is to serve onshore clients for their innovative molecule. So once the capex goes live (whenever ), the portion of innovative molecules will increase rapidly. In FY22, $56 million (450 cr out of 3960 cr CDMO) was Innovative business, which is 11.38% of CDMO business. I think it could increase significantly in the next few years if one believes what they are saying.

Note- Invested

| Subscribe To Our Free Newsletter |