I agree on this point – initial return on capital will be low but as they ramp up & depreciation is also fully charged – incremental RoC should improve (this being a long term phenomenon – if they don’t any major capex in next couple of years)

My estimates are that Force (at consol level) can at least cross the last peak PAT (of 180 Cr in FY17) by FY25 (base case) – still return ratios (RoCE to be specific) at very optimistic case can cross double digit levels.

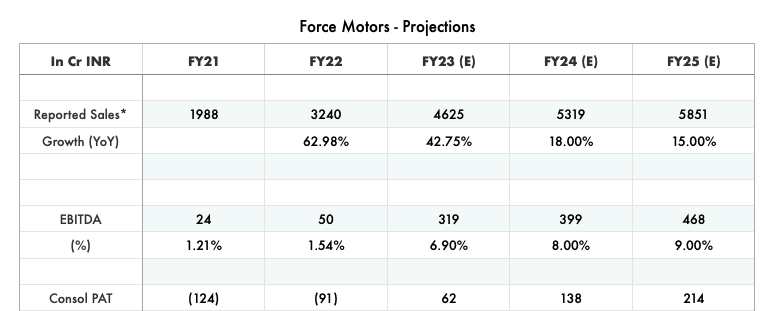

FY23 EBITDA can very well be the highest ever in the history for the company and sequential improvement should be there in FY24.

I am still not able to figure out incremental return ratios (as further capex plans are not known) and revenue potential of new launches such as Urbania, Gurkha & Citiline is anyone’s guess. I feel this is where the risk is and if they can sweat the assets efficiently – rewards can be big (as compared to the risk we are taking at current valuations).

Margin expansion is needed to achieve that and with Urbania targeting export markets & company has already been consulting with KPMG & E&Y for cost controlling measures since last 2-3 years – overall margins should improve (but can’t say whether they will improve to double digit or not).

In past, the peak RoCE which the company did was of 18% in FY-16 but later on it dipped as CV cycle also reversed and the company kept on doing capex. Hopefully they will be able to cross this as JV becomes profitable and they scale their operations.

All being said – the company seriously need to review its marketing strategies. They have superior products but lack in marketing – hopefully they will work on it.

As far as return ratios are concerned – I feel most of the OEMs (in CVs and some in PVs) have seen contraction and last peak in most of them was during 2016-18 period.

D – Invested & definitely watching closely and aware of these risks – margin of safety is very high at current valuations.

| Subscribe To Our Free Newsletter |