- Almost 3GW of back log was there so out of this for 400MW we have signed PSA.

Odisha’s GRIDCO to Procure 400 MW Wind Power from SECI

MAIN POINTS

a) The wind tariff will range from ₹2.96/kWh to ₹3.01/kWh. ( Good price)

b) 390MW is of tranche XII rest is of tranche XI

c) Tranche XII winners are NTPC 200MW ,EDF 300MW , JSW 300MW, Torrent Power 300MW

So this 390MW has to be assigned to some developer in short we have 390MW with signed PSA ready to come in market.

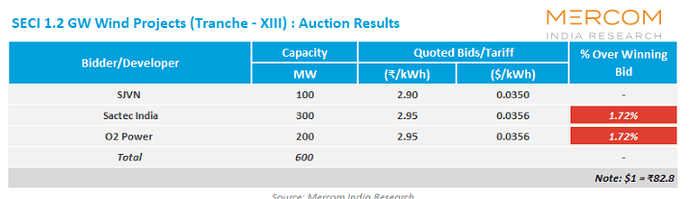

- Tranche XIII status below

SJVN and other are yet to award those tenders to the developers

Under Tranche XIII we have close to 600MW.

- What I understand is only the Tranche XII backlog has a possibility to be executed in future rest all backlog have very low tariff( 9,10,11). So under Tranche XII we have 1.2GW of contract out of which 390MW has a signed PSA so balance 810MW still has a possibility to workout in future.

4.SECI Invites Bids for 1.2 GW of ISTS-Connected Wind Projects

MAIN POINTS

a) SECI has invited bids for 1.2GW under Tranche XIV

b) CUF should be above 22% ( very important point)

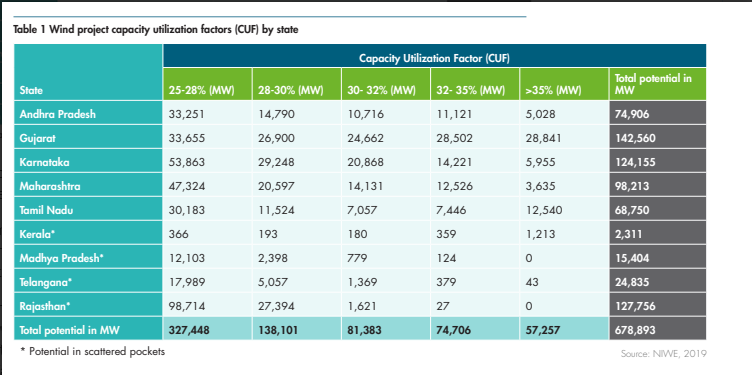

This is the land availability in india. I think as per national institute of wind energy.

MY TAKE

-

This Year First half might be a dull period for SUZLON. I expect volumes to pick up from H2 FY24 and H1FY26 being the peak.

-

Suzlon has a decent order book of 780MW ( this can last for 4 quarters)

-

We have total 3GW of orders to come in market ( Tranche XII,XIII,XIV)

-

Suzlon TTM finance cost 500cr and Suzlon expected finance cost FY24 200cr. ( clearly with same execution they save 300cr. After 2nd part of rights issue of 600cr their NET DEBT will come down to 1700cr hence 200cr interest cost )

-

Their OEM business will grow form FY24 which was flat from last 2yrs. FY24 will have low single digit growth but from FY25 we should see good growth.( will quantify later)

NOTE : Suzlon is a highly risky bet as good as calculated GAMBLING because there are too many moving parts in this kind of business. I see this as a medium term opportunity ( 2yrs to 3yrs to make 2x or 3x but highly risky. I have my own exit criteria and I would exit once I don’t see some decent progress in the industry.

GWIC has released their FY23 global wind report. I am yet to go through it which would further increase my understanding.

KEY RISK

RISK.docx (215.3 KB)

I am still understanding this industry and now I am slowly understanding that the ROOT cause of problem is not land but price. Once I develop decent understanding here I would share with you.

Disclosure – Invested

| Subscribe To Our Free Newsletter |