We did a detailed analysis of Titagarh Wagons and we believe this company is expected to see some “ache din” going forward.

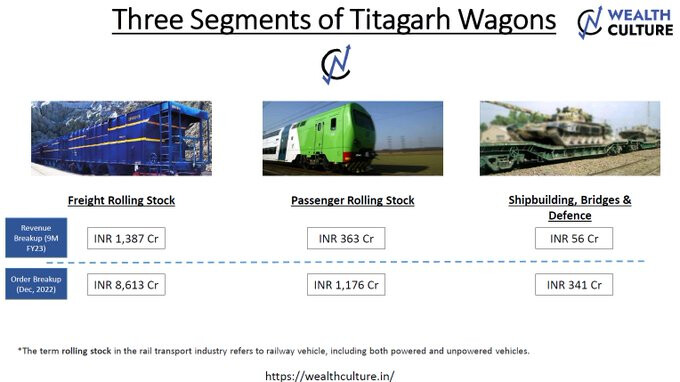

The company operates in 3 segments. Revenue and order breakup as follows:

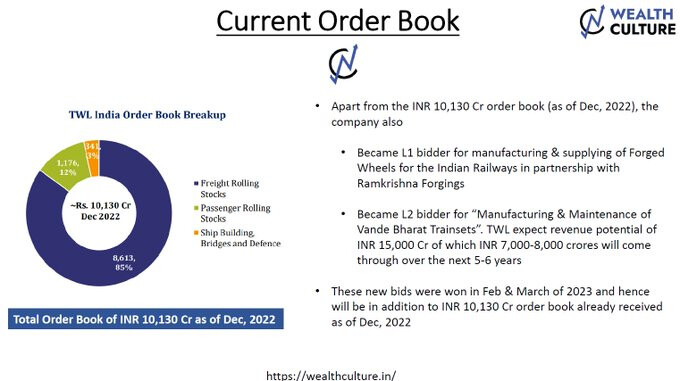

TWL has more than 10k crores in order book. Additionally, it was declared L2 and L1 bidder in 2 new projects.

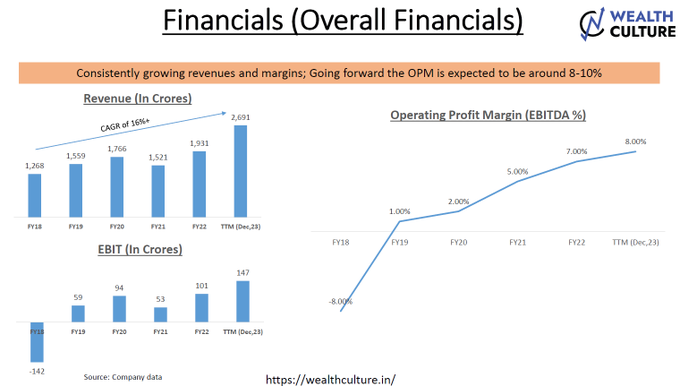

Financials have been improving consistently over the last few years and we expect this to continue in the future as well:

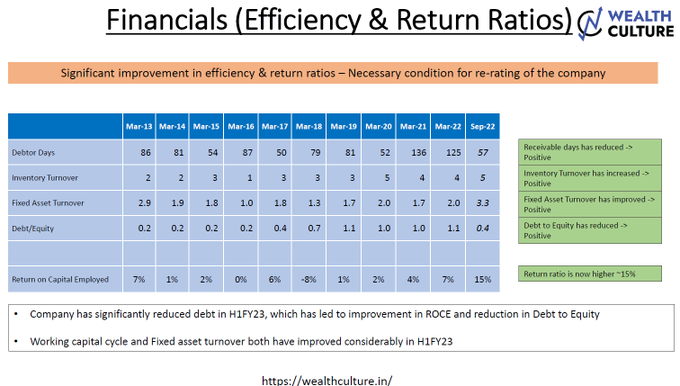

Similarly we can see an improvement in efficiency and return ratios as well.

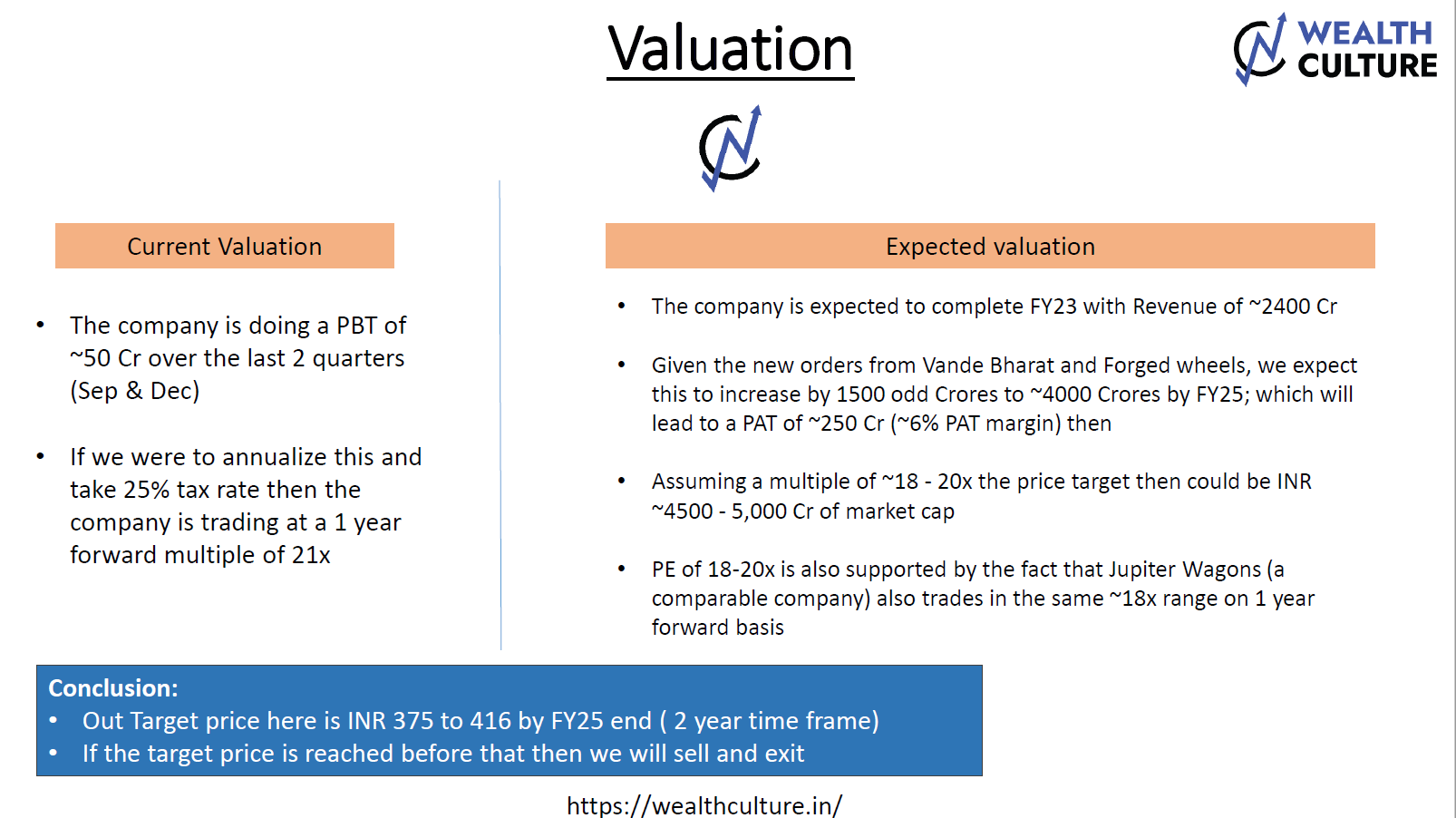

Our thought process on valuation as follows:

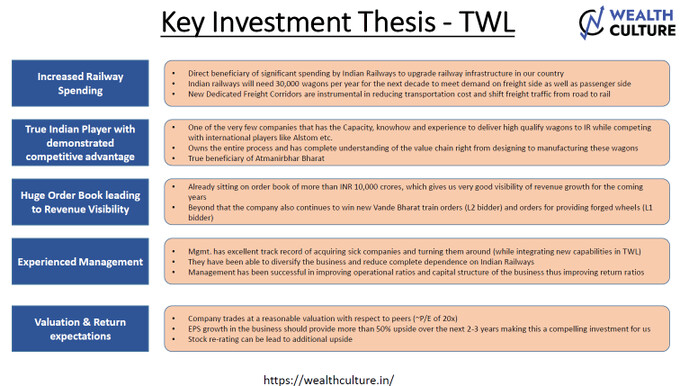

To summarise our investment thesis is as follows.

Technically speaking the Stock (TWL) has given an ATH breakout. This ATH was first seen in 2008, so it is a very old ATH. The volumes are also reasonably good. I hope to see the stock in trend now.

disc: we are already invested in this company along with our clients and hence we maybe biased.

This is not a buy/sell recommendation. Please consult your advisor before investing.

Ujjawal Kumar

Founder & CIO – WealthCulture

| Subscribe To Our Free Newsletter |