This intrigued me a bit as well. Briefly checked last year’s AR for Vijaya and Krsnaa. Some things stand out base on my very crude assessment (no positive or negative opinion on these)

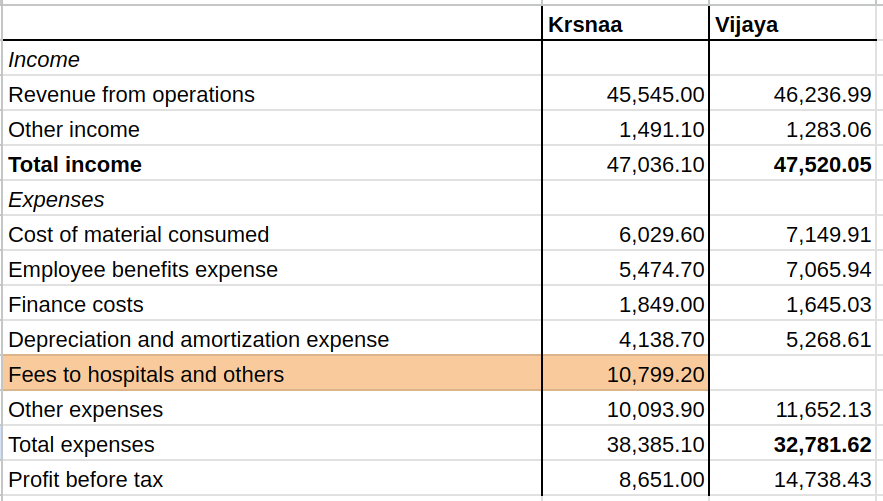

- Krsnaa is heavy on Radiology compared to Vijaya, which is heavy on Pathology. So, was expecting the depreciation cost to be more for Krsnaa. But, it turned out to be lower…

- One big expense for Krsnaa is the fee to hospitals. This is directly affecting their profit margins. But, this is also their business model which is different from Vijaya’s.

Below from respective AR for FY 22.

IMO, the major part is to track the quality of their tests. So far, they have a very good record. Otherwise, the management is pretty vocal that they are building their moat in terms of pricing (below from investor presentation).

It does appear too good to be true considering how much of a discount they have. But they do seem to generate decent cash flows and I am not able to locate any doubtful entries in their statements yet. Eager to see their upcoming annual report.

Apologies if I added more to confusion.

Disc: Invested

| Subscribe To Our Free Newsletter |