I was briefly invested in the company in 2021. I was also impressed by the business prospects. but exited in late 2021 as I was not convinced by some factors associated with the business.

- I believe there is huge competition from unorganised players and unlisted player.

- There is a lot of political involvement in awarding of contracts. There are issues or delay in payment when the political party in power at the municipality changes.

- Why has the EBITDA margins gone down since 2021? I think it has to do with provisions. These provisions started showing in P & L since Elliot capital made exit from the company in Sept’21. Was they painting a rosy picture to provide them a complete exit which they couldn’t do at the time of IPO?

- Qualified opinion from Auditors: I think the company proposed accountable reserve concept to combat the qualified opinion at least this FY. I think this is a good step in this direction. Wont this impact P & L?

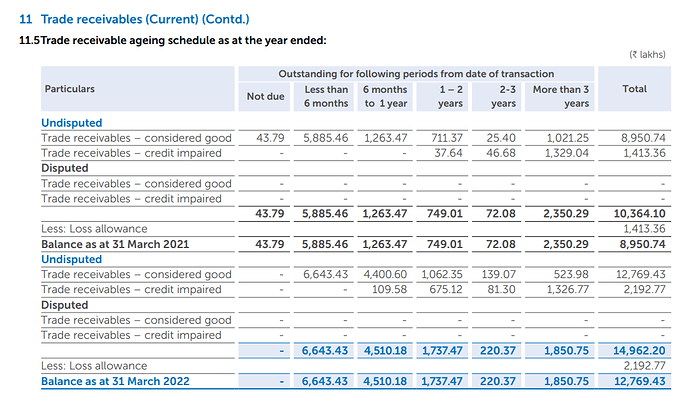

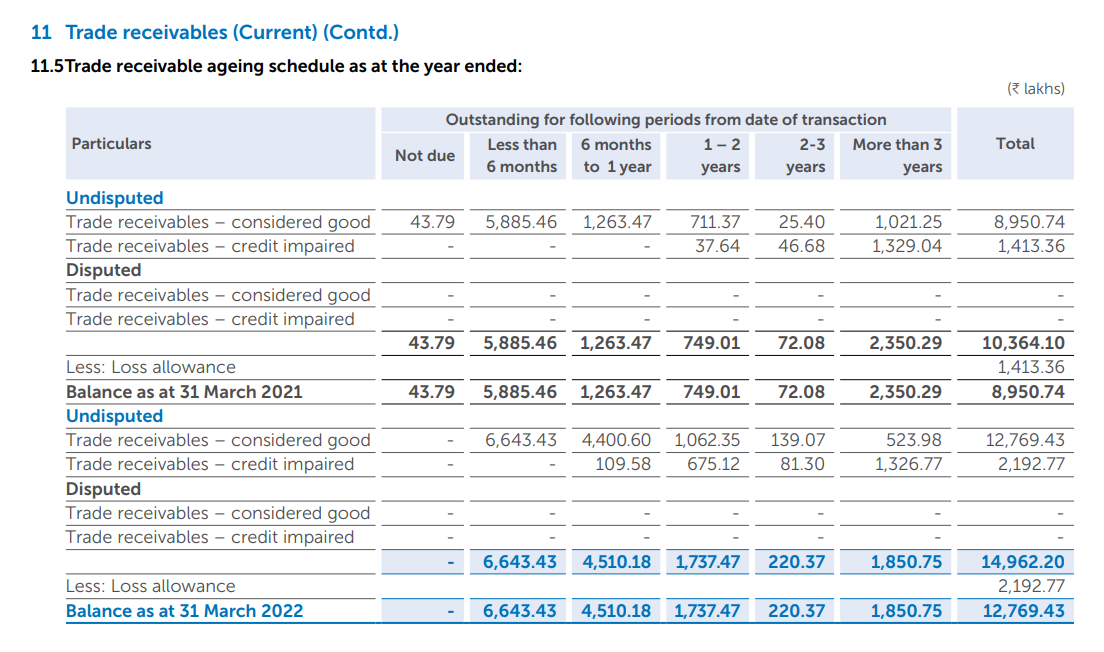

- Keeping retention money is a regular concept. I don’t think this could be a reason why auditors gave a qualified opinion. Retention money is a significant part of non current receivable. But there is current receivables in addition to this. Look at the age of current receivable and allowance for loss.

- CWIP as of Sept 22 is 50 crores. WTE project was initially envisaged at around 240 crores. So I think the bulk of investment is yet to take place.

Discl: Not invested. I have not gone fully through the AR. I may have some biases. I will try to update more on the trade receivable situation. Let me know if there is any mistakes above. I was spooked by the IT raid as well.

| Subscribe To Our Free Newsletter |