Hello Everyone , I have recently started studying this company . All due credits to @Worldlywiseinvestors .

I saw that no one in this space talked about the recent quarter concall which took place . So I have attached the link here : Apcotex Industries Limited Q3 FY23 Earnings Concall – YouTube

I had highlighted some notes by the management on the transcript itself , if you want you can simply go through the transcript i.e. attached below and side by side hear the con-call ( That’s what I do) as it was packed with info.

Q3Fy23 Apcotex Concall .pdf (983.4 KB)

Below I have attached some important snapshots which really helped me clear some doubts :

-

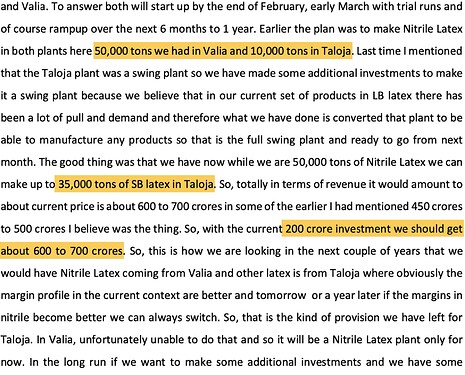

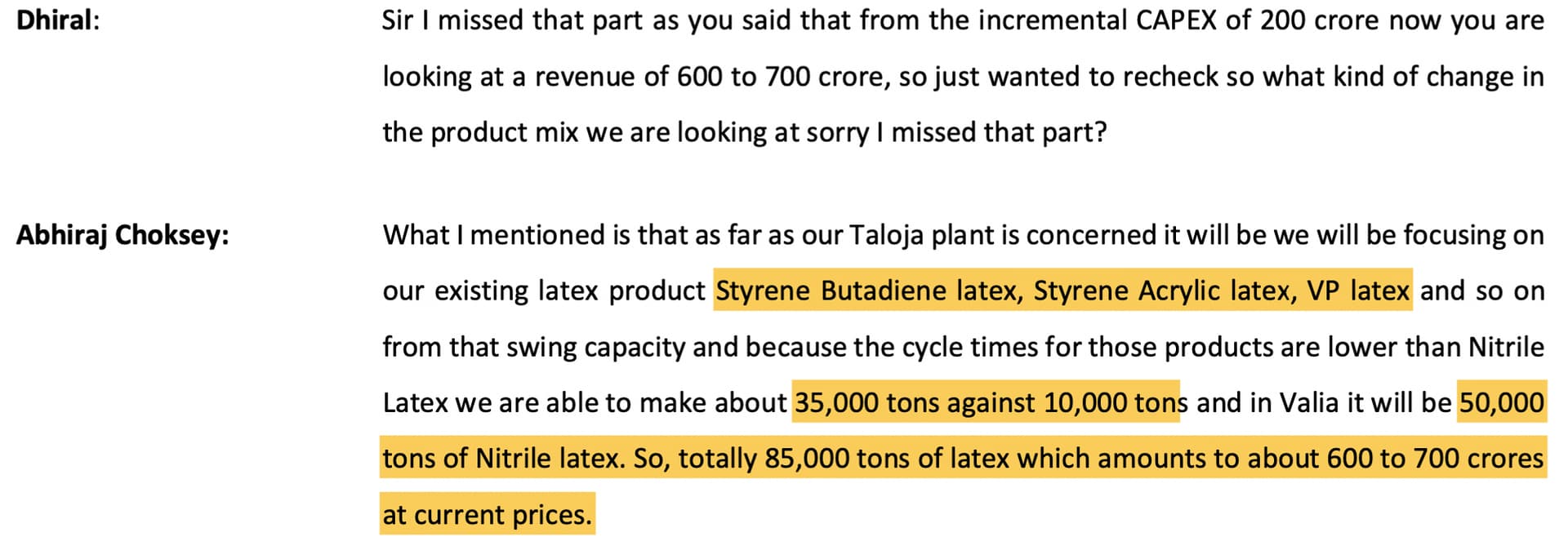

27th Jan Q3Fy23 concall , capex and it’s utilization and flow to topline by Abhiraj Choksey

-

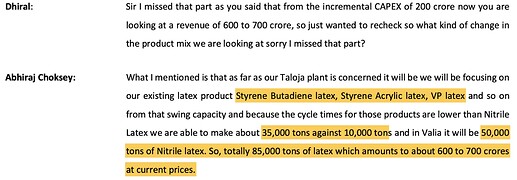

So total 85000 tpa latex , making a 600-700Cr . ( quarterly 150-175Cr in addition)

-

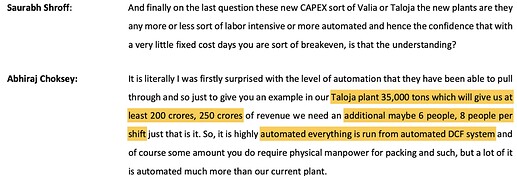

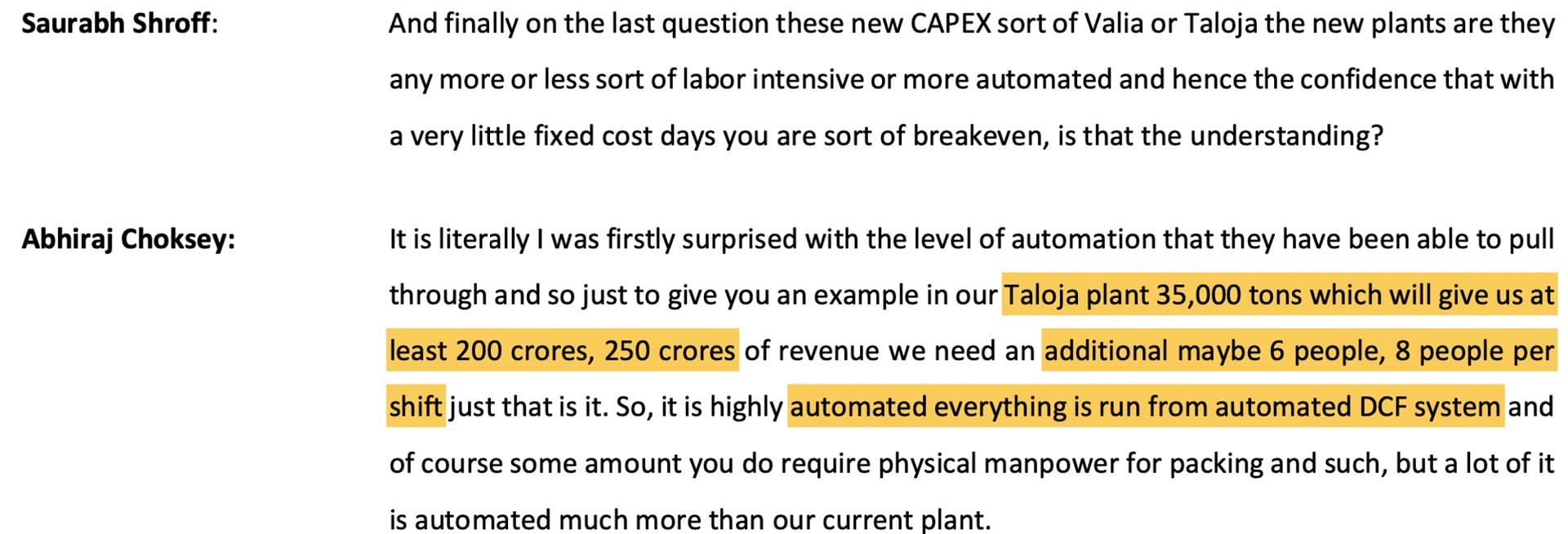

The plant’s would be highly automated , playing a part in operating leverage .

-

The Capex was funded by 60% debt(120cr) , and 40%(80cr) internal accruals

-

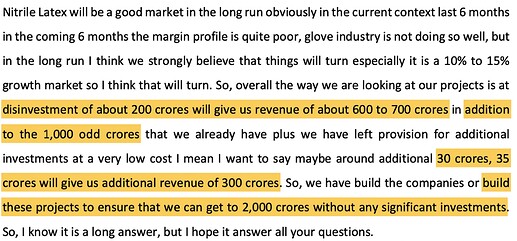

Abhiraj Choksey as to how to how the 200 Cr Capex in Taloja and Valia plant can change the final topline of the company .

Some pointers from above :

- To reach total topline of 2000 Cr would be in 4-5 years timeframe with all the things in place.

- Currently the sales is around 900-1100 Cr

- ROCE of 20-25% would be possible

-

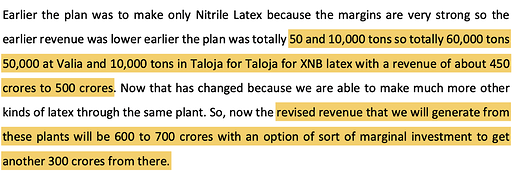

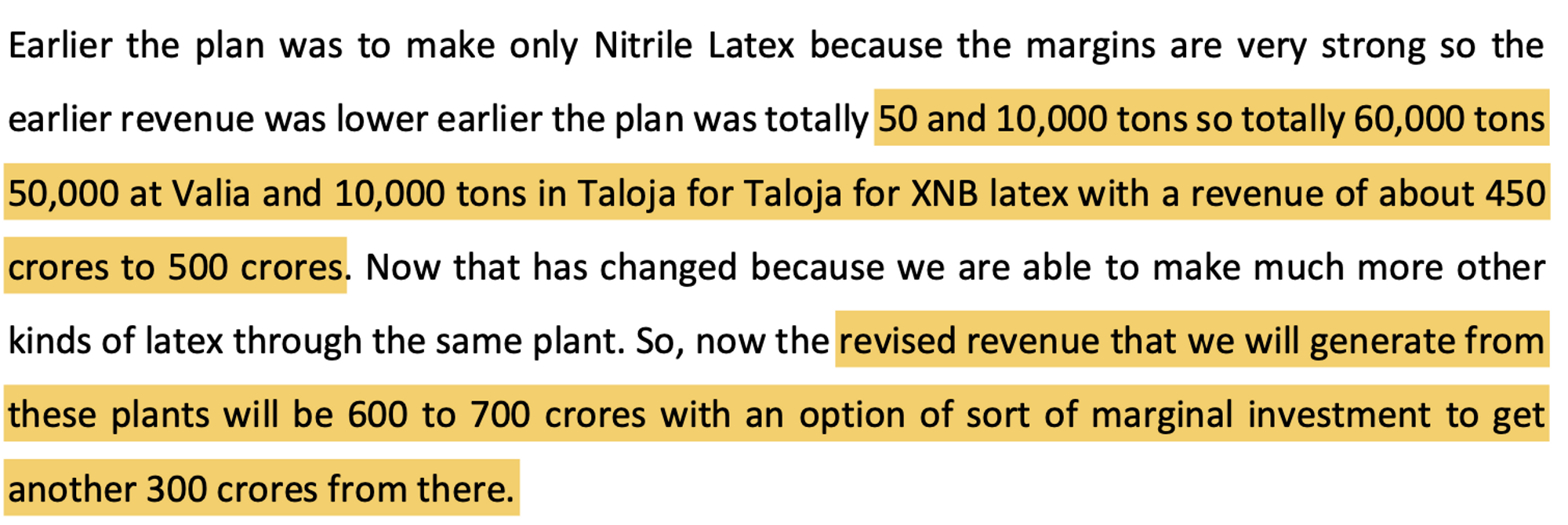

More clarification by Mr. Chokey as to why moving fromt the original plan .

-

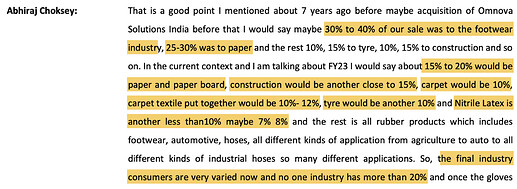

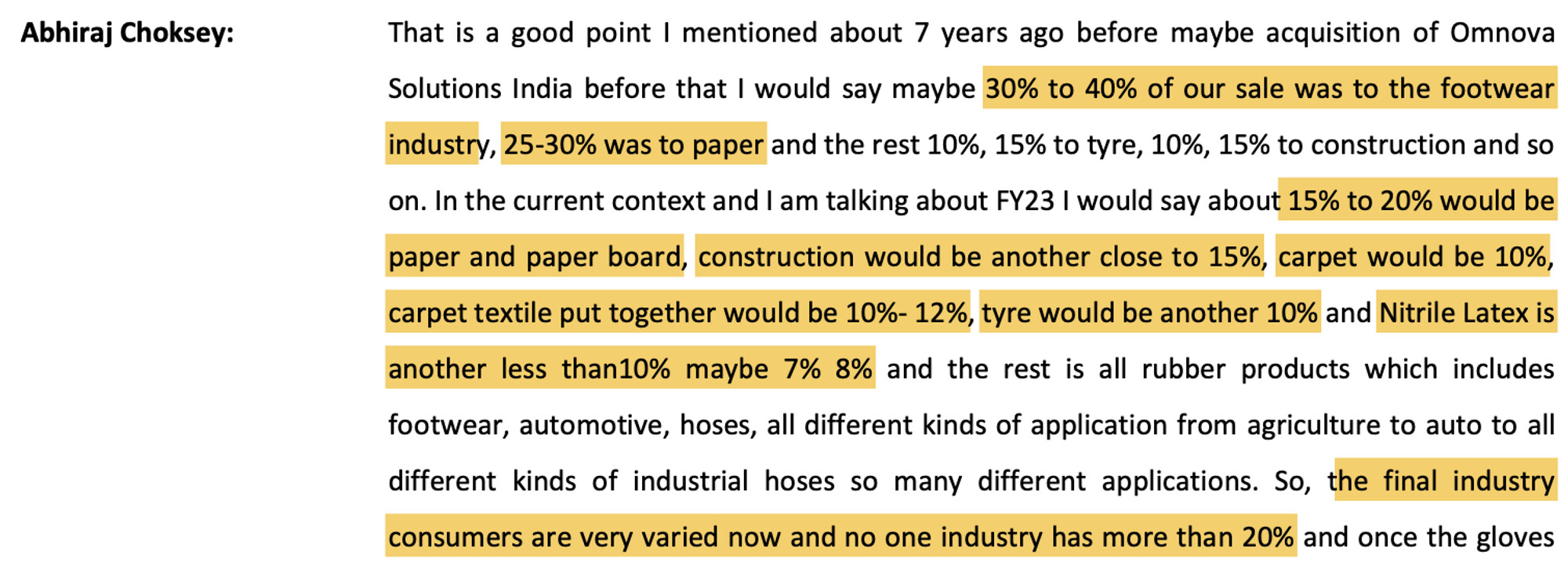

The change in revenue mix over the years.

-

Export – 20% , roughly 180-220 Cr , Domestic – 80% , roughly 780-820 Cr

-

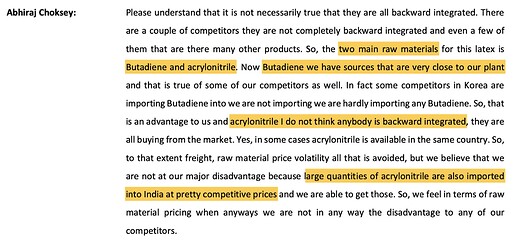

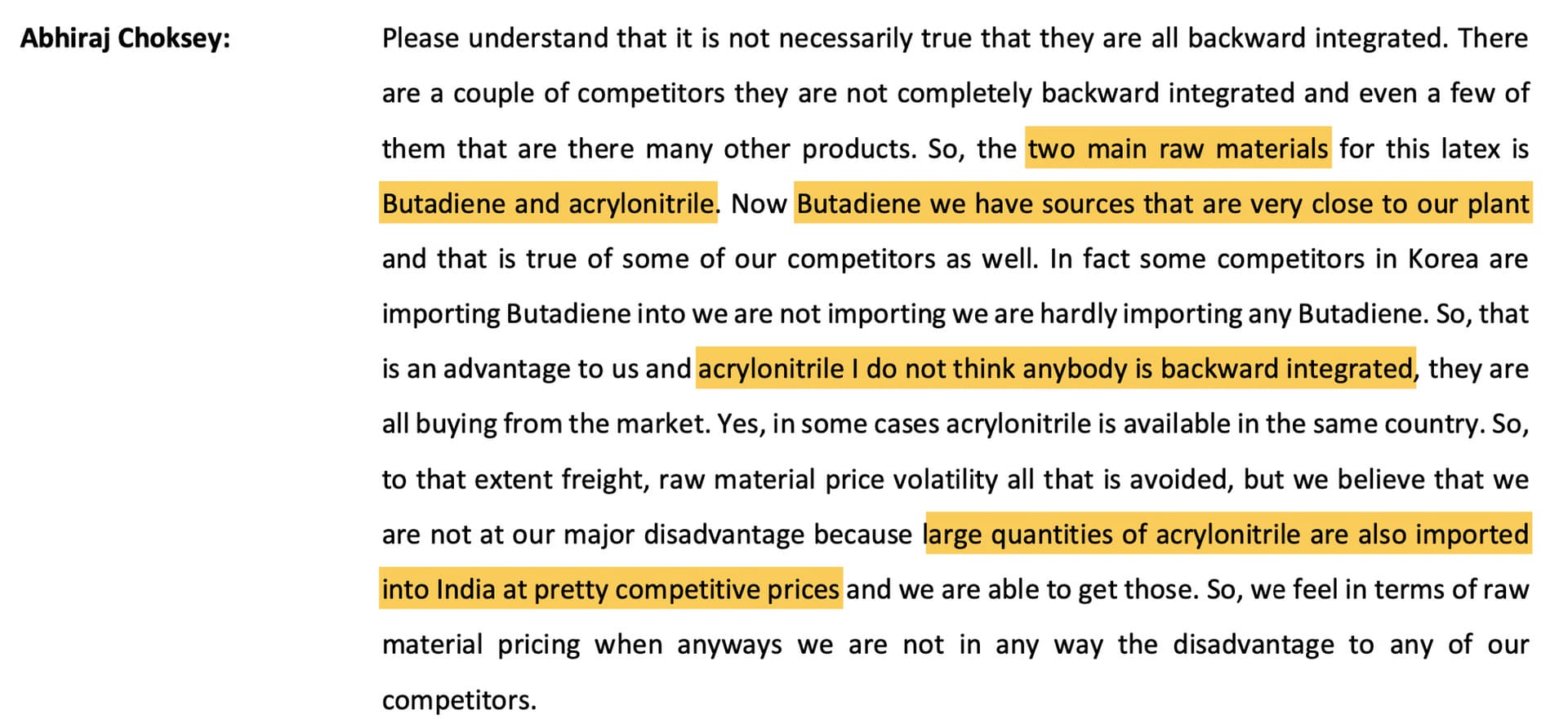

When asked about the competition and about there competitive advantage in the market.

Hope reading all of these would have cleared some of your doubts , as it really helped me a lot ![]()

Happy Weekend , cheers ![]()

| Subscribe To Our Free Newsletter |