So the question is – what could be the possible reasons for Ideal Cures’ so much higher Gross Margins?

Given the general lack of information on both these companies, it is hard to say for sure. But few of the possible hypotheses could be:

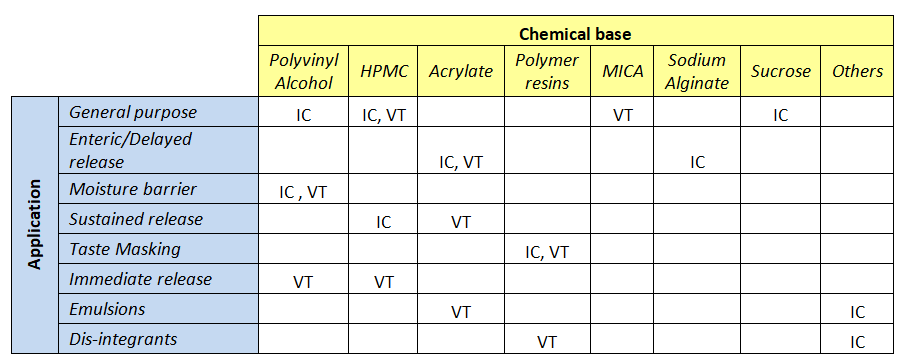

(i) Chemical base used in key products

Basis my understanding from the respective product brochures, have put together a table on chemical base and applications these two companies work on.

As can be seen from above, both have products across applications. However one difference is VT’s concentration on Acrylate polymer based products.

Basis product listings an estimate is that around 50% of VT’s listed products are based on Acrylate (as a % of all listed products). While the corresponding number for IC is around 20%.

This high dependence on Acrylate could be the reason why VT’s margins fluctuate widely based on crude oil (raw material source) prices while that of IC are relatively stable.

(ii) Ideal Cures is more R&D focused than Vikram Thermo (complex products, possible backward integration etc.)

Data on R&D spends is a bit patchy (inconsistently reported for IC). However for the years it is available, it does show that IC’s spend on R&D has been higher than that of VT.

While not conclusive, it could possibly indicate that IC’s products are better (in complexity and/or quality) and a somewhat higher degree of backward integration than VT.

| R&D spends as % of revenue | 2022 | 2021 | 2020 | 2019 | 2018 |

|---|---|---|---|---|---|

| Ideal Cures | NA | 2% | 2% | 3% | NA |

| Vikram Thermo | 0.1% | 0.1% | 0.2% | 0.9% | 0.1% |

(iii) VT’s sales mix (Pharma & Non-pharma split)

Till 2016, VT had about 30% of sales coming from DPO (perfumery stabilizer, HTF) which is relatively low margin vs their pharma products. They have stopped sharing the break-up of drug coatings vs DPO post 2016. However there are indications that DPO’s share in total revenues has been declining. Hence this in itself should not be a big reason for VT’s lower margins as compared to IC.

Above are just some of the hypotheses on why IC’s margins have been relatively better. If VP seniors can kindly share their views on possible reasons for above, it will really help newer equity market investors like myself ![]()

| Subscribe To Our Free Newsletter |