I would like to point out a few things

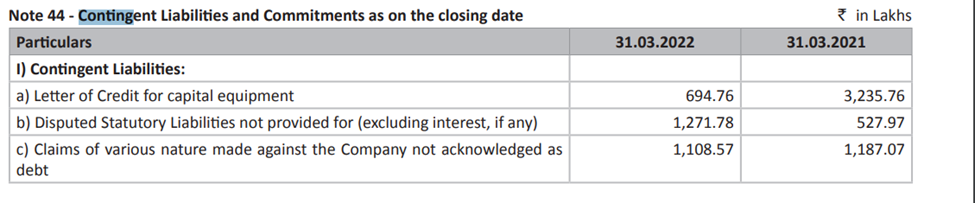

Contingent Liability

Its 5 % of net worth and close to 7 crores is letter of credit.

Debt

Debt of 534 crores is huge if we look at it separately. The company however has cash and cash equivalents of 235 crores as of Sept’22. At the last quarterly run rate the company could be net debt free by the end of next FY. Interest payment is currently huge but can considerably reduce if the company uses cash to pay down debt.

Valuation

The company is available at a trailing EV/EBITDA of 9.18 which I consider cheap for a non cyclical business. Also P/E is 21, is much lesser than other listed hospitals.

Dividend payout is very low and I don’t think its a major issue. It’s true that its a regional player, but I am not worried about that as long as there is steady cash flows. Going forward, I am interested/ concerned to know how the company is going to utilize the cash its generating.

| Subscribe To Our Free Newsletter |