Hi Pratik,

I went through your notes and model , I just had one doubt that the Apcobuild as a part of it’s revenue constitutes less than 4-5% of it’s revenue from what I am aware . If you could help with any source .

Secondly regarding the model –

- The management had mentioned that it can expect a opm% of 17 , so we can work with 15% .

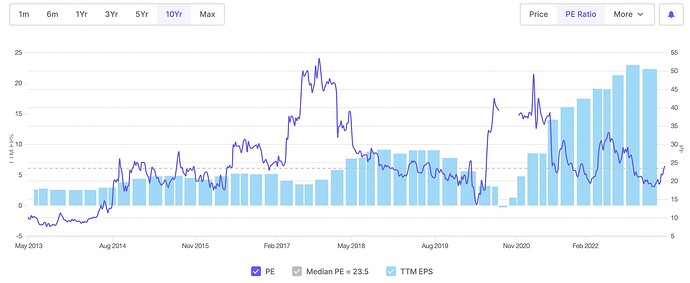

- The Average PE for 10years has been 23.5 .

Considering these the Share price for FY25E could be = 23.5(pe)* 27(eps) = 634

( I do agree that somewhat the growth has been factored in post the commission of the new plant ) The stock from 400 has gone to 540 . Mr. Market is supreme after all ![]()

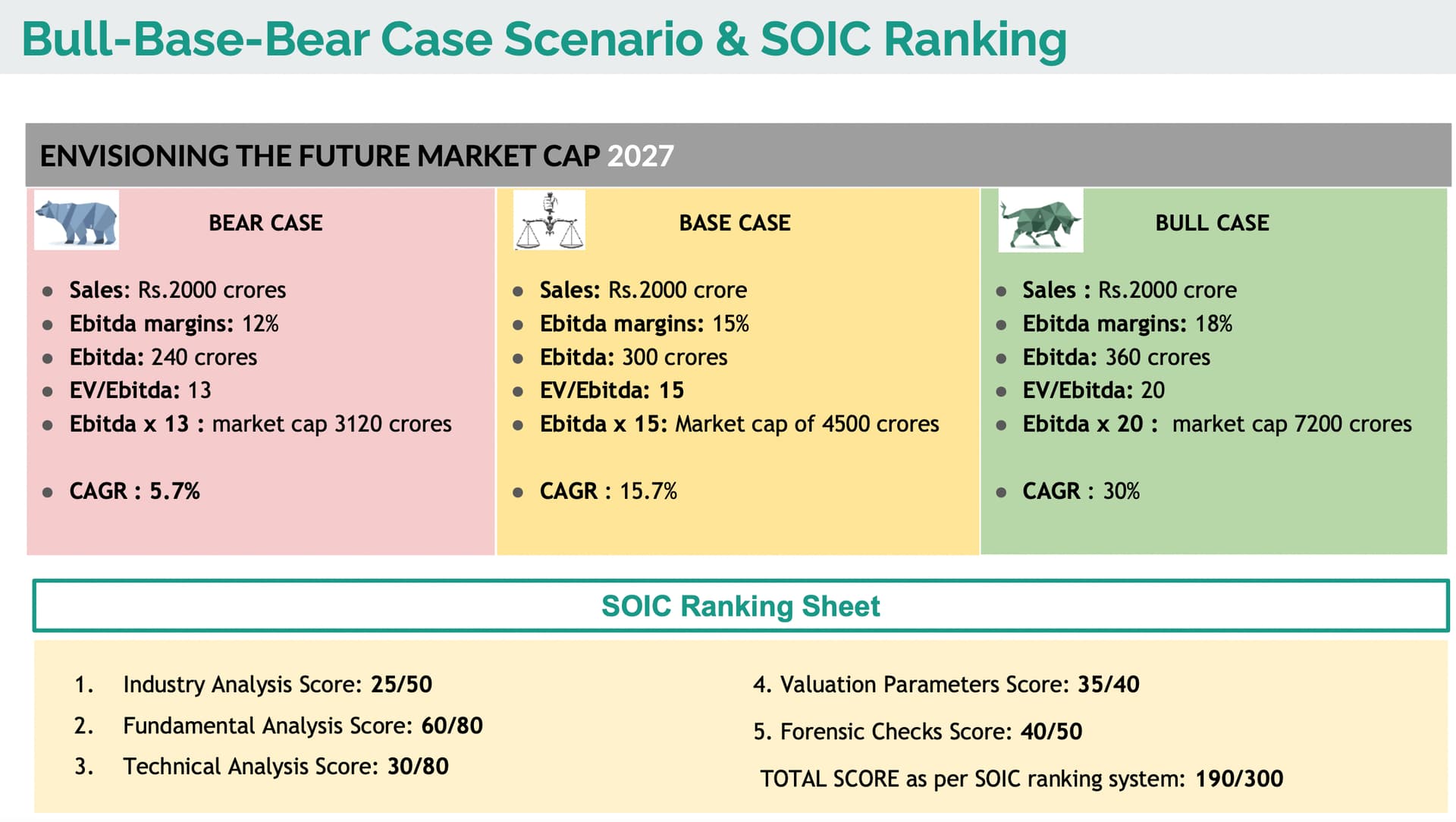

I had worked with the other members of the soic team including @Mgkreddy and came up with the below model using ev/ebitda .

Assumptions taken were :

- Management on the latest call had mentioned 200 Cr capex +35Cr of debottlenecking capex if taken place would lead to 1000Cr increase in topline . That’s why the fixed 2000Cr in sales for 2027.

Disc : Interested but not invested ![]()

| Subscribe To Our Free Newsletter |