In the last 3 to 4months I have realized how important Cost to income is so let me just share you what I have noticed. Please Ignore if you already know

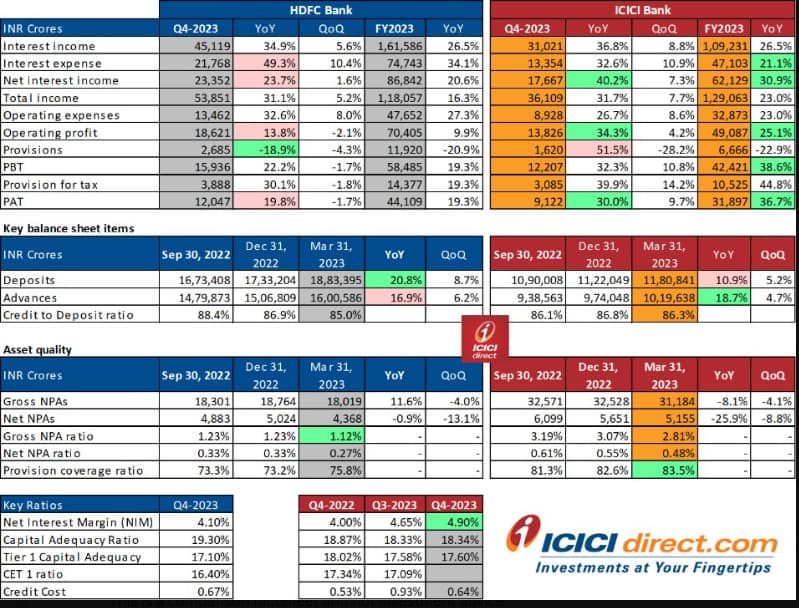

This is the result of HDFC and ICICI if you notice HDFC NII is 86000cr ( up 20% YoY) and operating expense is 47000cr ( up 27% YoY) despite this in absolute terms they have added incremental revenue when I just compare NII and operating expense. Same can be seen in ICICI case.

In IDFC case NII is 9000cr (up 28% YoY) and operating expense is 8700cr (up 25% YoY) now the incremental revenue IDFC has added is absolutely low.

In simple terms if NII is 100 and operating cost is 50 and both increase by 30% my revenue grows by 15%

But if NII is 100 and operating cost is 90 and both grow by 30% I grow by 3%. Now I cannot increase the gap between my NII and operating cost in 1year it will take 2 to 3yrs atlest.

IDFC NII is 100 and operating cost is 96 so now we can do X growing at 20% Y growing at 15% or whatever and see when can it come to NII 100 and operating cost at 60 for operating leverage for comparison HDFC operating cost is 55 and ICICI 53.

But despite this problem the only way to still grow is other income which can be game changer so in IDFC case we have to analyze 1. What are the operating cost, How much is business volume related, When will leverage kick in. 2. How much can other income grow.

Another important point is we have to see this year how much of my profit came from lower provisioning and how much came from higher operating profit or PPOP and next year will I be able to get more profit from lower provisioning or not.

As rightly said by Nirvana Laha Sir that we have to focus on the % of promoter NET WORTH in a company. So if this 0.4% is lets say 90% of his NET WORTH then there is enough skin in the game

I think these are their sustainable NIM but in the very long term as you get bigger they to to come in line with larger banks. EXAMPLE – Bandhan bank had a NIM of 8% but then they had asset quality issue and now they are moving to corporate lona from EEB loan ( Emerging Entrepreneurs Business) so they are saying that going forward their NIM will fall.

Now it is not going to fall by 100bps in 1 year it is going to be very slow because as a bank becomes bigger they want to give loan to the creamy layer which as on date is captured by HDFC,ICICI,KOTAK that is why they have the best asset quality and you can give loan to this creamy layer only when you have the ability to take CASA and 3.5% or 4%

A good way to see PB said one by Ayush Mittal sir was divide the ROE of a company by the 10yrs bond yield. So if ROE is 30% and bond yeild is 6% PB can be 5times. Now there are many more adjustment to be done and this not a hard and fast rule. A SCB bank can never generate 35% ROE what an NBFC can hence high PB.

SUMMARY.

1. We have to focus on ROE as it captures dilution but PAT does not so instead of PAT growth we should see ROE and EPS

2. We need to see other income and how long can it grow at current rate because for IDFC that is critical as for 2 to 3yrs operating leverage wont be significant.

3 We have to analyze operating expanse and see how much is volume related and try to roughly estimate when will leverage kick in

4. How much profit this year was form lower provisioning and next year what will be the drivers

5. At what rate can book value grow @Pradeep_Jadhav Sir most of your estimates are too high especially dilution at various PB and i think some where we have to consider cyclicality factor I feel especially small SCB cannot have linear growth. So that factor has to be considered

| Subscribe To Our Free Newsletter |