Relevant events from Q4FY23:

-

Raised 340 Cr. of equity. New investors are onboard for a tenure of 5-8 years.

-

Launched a much awaited product where they provide working capital loans for very short tenures, often charging interest for as little as a few days.

-

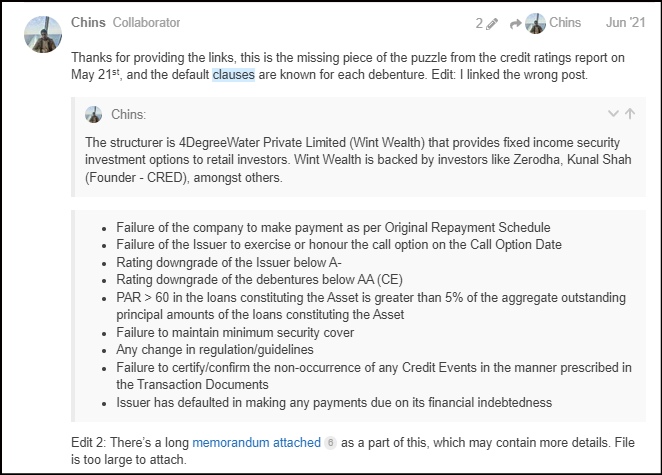

There was a lot of drama following the switch from Acuite to Crisil. Acuite promptly downgraded Ugro’s rating, leading to a clause breach in one of their MLDs. Incidentally, VP had discussed these clauses during the early days of the thread, two years ago:

-

They have scaled their off-book AUM from 475 Cr. at the end of FY22 to 2400 Cr. at the end of FY23.

-

There is currently an overhang in the stock, where DBZ Cyprus (one of the large investors) have been constantly selling. Shareholding has gone down from 20% last year to now below 1% in my estimate.

-

Q4FY23 results should see around 30 Cr. of PBT, but we expect a tax issue of around 7 Cr. (from the same issue in Q2) relating to old deferred tax. FY24 should be completely free of any abnormal tax, and they’re expecting around 200-220 Cr. of PBT in FY24.

| Subscribe To Our Free Newsletter |